24 Mar, 2021 US operator guidance points to modest increase in 2021 capital investments, according to GlobalData

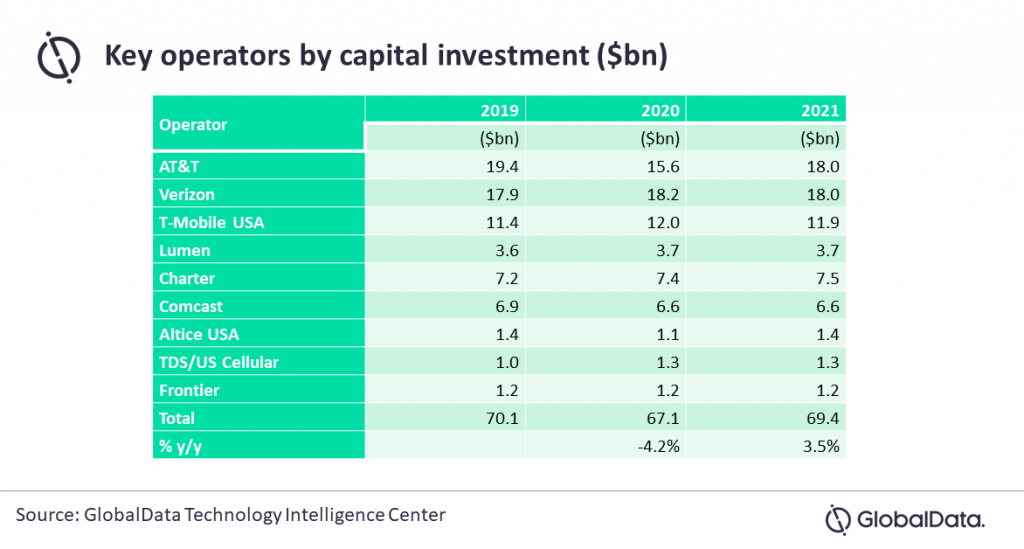

Posted in TechnologyWhile COVID-19 did slow capital investment in the US*, it could have been worse. Thanks to a flurry of activity toward the end of the year, the top nine publicly reported carriers studied by GlobalData, all of which spent in excess of $1bn in capex, accounted for just over $67bn in capital spending. That was down by approximately $3bn (4.2%) compared to 2019.

GlobalData estimates that the ‘big three’ – AT&T, Verizon, and T-Mobile USA, which collectively account for nearly 70% of total capex – spent roughly $46bn, down 6.1% from 2019. However, the bulk of the decline was attributable to AT&T.

John Byrne, Service Director, Telecom Technology & Software at GlobalData, comments: “Following the outbreak of COVID-19, many operators’ capital investment came to a standstill – both due to the disappearance of supporting staff, as employees were forced to retreat to their homes, and to supply chain issues, particularly regarding Chinese suppliers. However, those issues were resolved relatively quickly. As a result, it was relatively ‘business as usual’ for many operators for most of H2 2020.”

It was a similar story outside of the US as most operators reported modest year-to-year declines in capex spending. For example:

- Telefónica reported a significant year-to-year decline in 2020, reducing capital expenditures from €8.8bn to €5.9bn.

- América Móvil spent approximately 16% less in 2021 capex, at $6.7bn, down from $8bn. Orange capex declined only slightly from 2019 to 2020, from €7.3bn to €7.1 bn. However, Orange expects capex to grow to between €7.6bn and €7.7 bn in 2021.

- Deutsche Telekom and Orange both reported small year-to-year declines.

Bryne adds: “The good news – especially for supporting infrastructure vendors – is that capex looks likely to improve modestly in 2021. Factoring in available operator guidance, GlobalData estimates that next year’s spend among these US operators will be up by approximately 3.5%. That would return full-year investment to $69.4bn – just below the $70.1bn these operators spent on capex in pre-pandemic 2019. The story is the same for international operators surveyed, which appear likely to ramp up spending in a similar fashion.

“To network infrastructure vendors, year-end results show relatively good news on two fronts: the major and long-term slowdown from operators in the wake of COVID-19 was less severe and more short-lived than expected; and much of the slowdown now appears to be more related to deferrals into 2021 rather than cancellation of plans.”

* Based on GlobalData analysis of US operator financial results based on Q4 2020 earnings releases