24 Jan, 2022 Switching for cheaper motor insurance becomes harder for 77.8% of UK motorists as providers increase premiums, says GlobalData survey

Posted in AutomotiveThe vast majority of UK consumers who switch motor insurance policies do so for a cheaper price, with 77.8% of motor insurance customers switching at renewal because a different insurer offered a lower premium according to a GlobalData survey. However, that is now being restricted following the Financial Conduct Authority’s (FCA) regulatory reforms.

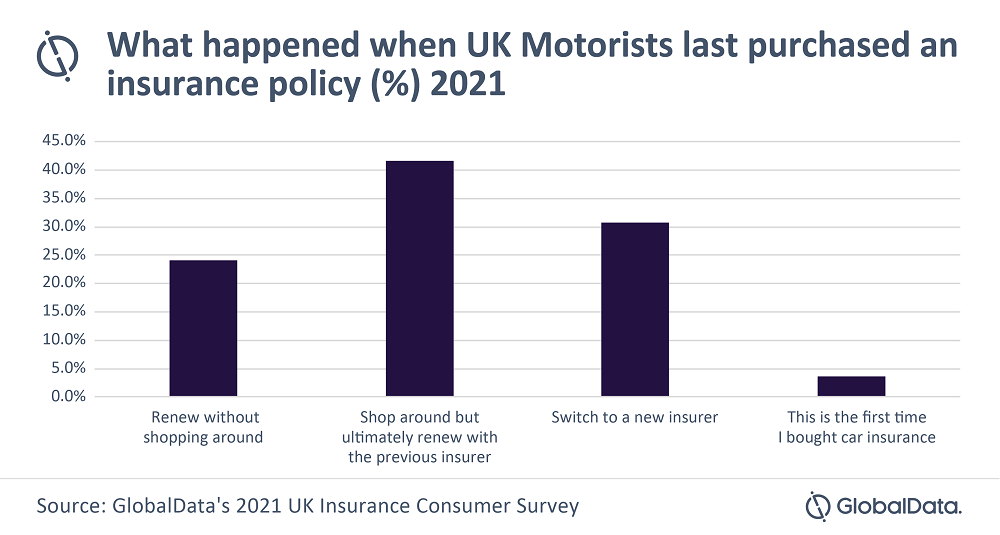

The leading data and analytics company’s 2021 UK Insurance Consumer Survey also found that 30.7% of all consumers switched to a new motor insurer in 2021. However, a further 41.6% shopped around but ended up staying with the same insurer. This highlights how many motor insurance consumers shop around for value in premiums every year.

Ben Carey-Evans, an insurance analyst at GlobalData commented: “As motor is a compulsory line, there is not a great deal that consumers can do, and insurers do not face the risk of people canceling policies, as in other lines. Rising prices will undoubtedly lead to more shopping around at renewal, but if no leading insurers are offering competitive premiums to new customers, then the amount of consumers switching will not necessarily rise.”

According to the Insurance Times, the cost of motor insurance has risen by £100 on average in 2022.* The new reforms prevent insurers from offering cheaper policies to new customers than existing ones. The lack of preferential rates will make it harder for consumers to shop around for cheaper rates. This will be worrying news for the FCA, which introduced these measures in order to protect consumers. Typically, existing customers had faced higher rates than prospective ones because of the loyalty penalty.

Carey-Evans went on to add: “The largest threat to insurers is likely to be from pay-per-mile motor insurers. These are generally startups, with companies such as Metromile and ByMiles leading the way. Their policies offer consumers a cheap basic rate for the year, and then they will pay a flexible rate based on how much they drive. This means they can control costs, and it may even be more fitting anyway, with fewer consumers commuting to work on a daily basis due to COVID-19.”

Overall, leading insurers and the FCA will need to work together to ensure premiums do not continue rising sharply throughout 2022. Consumers in the UK are facing low wage growth and an increased cost of living, so this would lead to many searching for alternative, cheaper forms of motor insurance, such as pay-per-mile.

*secondary data from the Insurance Times can be found here.