As emission regulations tighten and sustainability concerns grow, zero-emission vehicles like fuel cell electric vehicles (FCEVs) are gaining traction. They offer advantages over battery electric vehicles (BEVs), including longer range, faster refueling, and lower weight. Currently, the Asia-Pacific (APAC) region holds nearly 90% of the FCEVs market globally. Against this backdrop, the APAC fuel cell powertrains market is expected to record a compound annual growth rate (CAGR) of 46.7% over 2024-29, according to GlobalData, a leading data and analytics company.

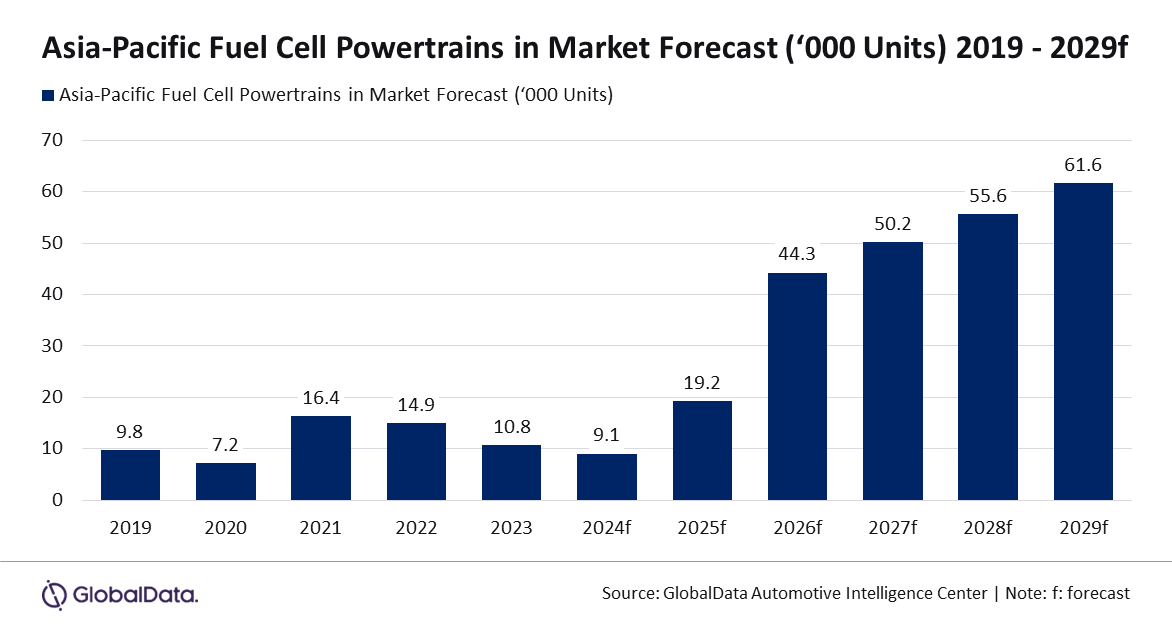

GlobalData’s latest report, “Global Sector Overview & Forecast: Fuel Cell Powertrains Q3 2024” reveals that the fuel cell powertrains market is estimated at 9.1 thousand units in 2024 and is forecast to reach 61.6 thousand units by 2029 in the APAC region.

Madhuchhanda Palit, Automotive Analyst at GlobalData, comments: “However, despite the benefits, there are several hurdles for FCEVs that need to be overcome to catch up with BEVs at their current adaptability stage. The cost of hydrogen is one of the hurdles that need to be addressed for the widespread adoption of FCEVs. Hydrogen is expensive to store and transport due to its volatility, but the key cost driver is the energy source used for production.

“Green hydrogen, produced through electrolysis using renewable energy like solar or wind, is environmentally friendly but costly compared to hydrogen produced using fossil fuels. This price disparity presents a significant barrier to the commercial viability of FCEVs. The water crisis is another major hurdle, as making hydrogen using the electrolysis method requires a significant amount of freshwater, which is a resource that is already under stress in many parts of Asia. Research is being undertaken to find alternatives to freshwater, and also different types of electrolysis methods are being explored to improve the feasibility and efficiency of the hydrogen production process.”

Hydrogen’s high energy density gives FCEVs a longer range, faster refueling, and fewer stops on long trips, making them particularly suitable for replacing diesel-powered trucks. Moreover, the battery required to power heavy cargo trucks for long hauls – a class 8 truck, for instance, generally having a 1-2MWh battery – is significantly heavier than a full tank of diesel or a fuel cell configuration, which typically only needs a small battery of 20-100kWh to accompany the hydrogen, making the fuel cell powertrain a more economically viable alternative to internal combustion engine (ICE) trucks.

As Asian countries focus on zero-emission vehicles, their approaches vary based on demographics and other factors. India, for example, aims to become a key hub for green hydrogen production and export through initiatives like the “National Green Hydrogen Mission.” This could boost FCEV adoption, as India’s lower lithium reserves and large population make the faster refueling times of FCEVs more appealing compared to BEV charging times.

Recognizing the potential, both the public and private sectors in the APAC region are making significant investments in FCEV technology. For example, Toyota has developed a portable hydrogen energy cartridge that is 16 inches long, 7 inches in diameter, and weighs just 5 kg. These swappable cartridges, designed for easy transport and quick replacement, simplify the refueling process and improve hydrogen accessibility as a clean energy source.

Palit concludes: “While fuel cell electric vehicles (FCEVs) offer a promising solution to air pollution and energy security challenges in Asia, their widespread adoption is contingent upon overcoming significant barriers. Public perception plays a crucial role, as many consumers remain unfamiliar with FCEVs and their benefits, highlighting the need for education and awareness campaigns. Additionally, government support, technological advancements, and infrastructure development are vital for growth in the FCEV market.”