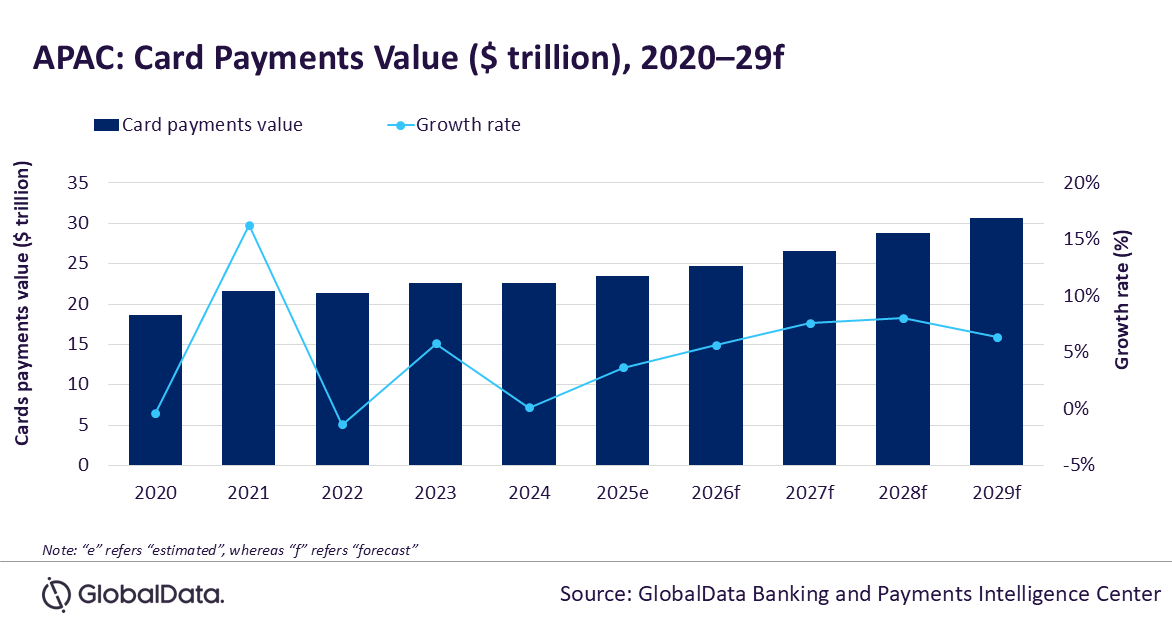

The Asia-Pacific (APAC) card payments market is forecast to grow at a compound annual growth rate (CAGR) by 6.9% between 2025 and 2029 to reach $30.6 trillion in 2029, supported by growing preference for electronic payments, according to GlobalData, a leading data and analytics company.

GlobalData’s Payment Cards Analytics reveals that that the card payment value in APAC registered a growth of 5.8% in 2023, driven by a rise in consumer spending. The value reached $22.6 trillion in 2024. However, the current global uncertainty resulting from the latest US tariffs may pose a challenge for the overall regional economic growth, resulting in slowdown in the overall card payments value, which is expected to grow by 3.6% in 2025.

Ravi Sharma, Lead Banking and Payments Analyst at GlobalData, comments: “China, South Korea, Japan, and Australia have a robust card payments market with a high card payments value. Other markets within the region are also catching up, supported by improving payment infrastructure, a rising middle-income population, growing financial awareness, and banks offering lucrative benefits in terms of reward programs and installment facilities.”

The APAC card payments market is dominated by China, which is expected to grow at a CAGR of 6.8% to reach $24.9 trillion in 2029. It will be distantly followed by Japan with an expected card payments value of $1.2 trillion, South Korea with $1.1 trillion, and Australia with $895.9 billion in 2029.

A well-developed payment infrastructure and the adoption of newer payment technologies contributed to growth in these markets. For instance, Australia’s contactless card market is highly developed, with strong penetration and awareness of contactless cards. This can be attributed to the widespread adoption of contactless payments in transportation further aiding adoption. In February 2025, Public Transport Victoria (PTV) announced plans to launch contactless payments on tap to go payments on the public transport of the State of Victoria.

However, card usage is comparatively low in countries such as Indonesia, India, Thailand, and Vietnam. This is mainly due to the limited financial awareness for card payments, inadequate POS infrastructure, and the growing popularity of QR-based mobile payments.

Governments in these markets are also taking a number of initiatives to strengthen payment infrastructure. For instance, the government in India offers businesses a subsidy for the installation of payment device such as POS terminal and QR code under the Payments Infrastructure Development Fund (PIDF) scheme. According to the Payments Council of India’s September 2024 report, both QR and physical POS terminals experienced substantial growth, demonstrating the PIDF’s positive impact on digital payment adoption.

Sharma continues: “However, the high costs involved in POS infrastructure for merchants and high preference for digital wallets among consumers remain challenges for faster growth in card payments in the region. Many consumers in the region have leapfrogged from cash to digital wallets skipping card payments. The availability of low-cost smartphones, rising Internet penetration, growing awareness of mobile payments and the proliferation of digital wallets have resulted in Asian countries shifting from cash transactions to mobile digital payments.”

Sharma concludes: “Looking ahead, the total card payments market in APAC is expected to continue its upward trajectory, driven by ongoing government initiatives, improving payment infrastructure and a consumer shift towards electronic payments. However, high preference for digital wallet payments remains a challenge for their faster adoption.”