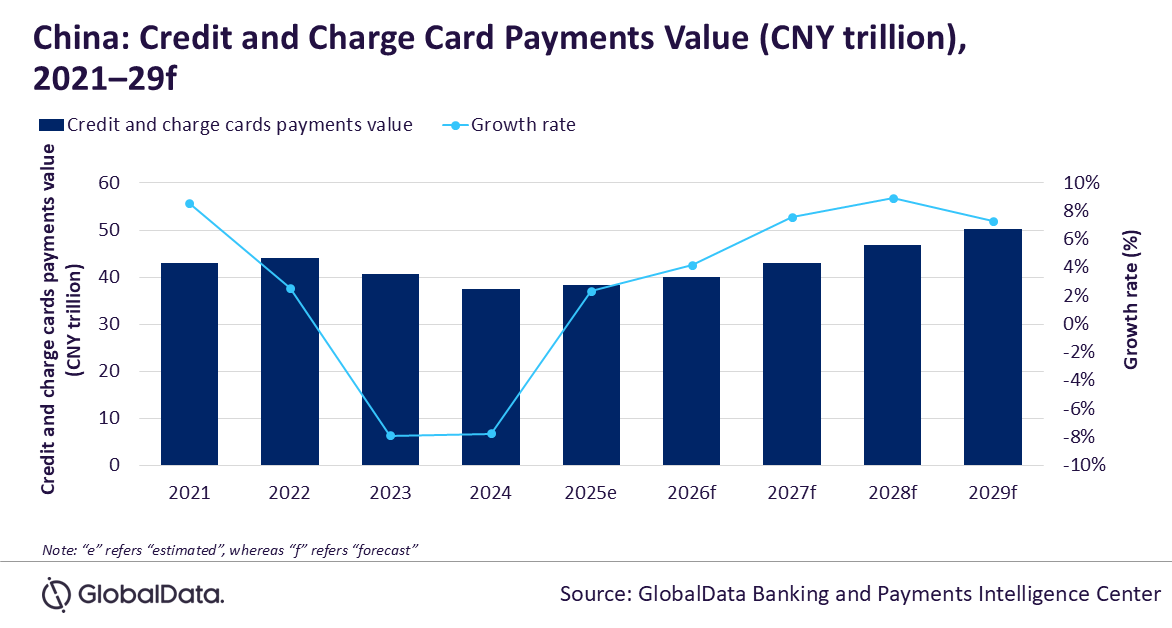

China’s credit and charge card payments market is expected to register a growth of 2.4% to reach CNY38.4 trillion ($5.3 trillion) in 2025, after a sluggish performance in the past two years. This growth will be driven by the rising consumer spending and increasing consumer preference for cashless transactions. Enhanced by value-added incentives such as cashback offers, flexible repayment options, and instalment facilities, the market is set to maintain an upward trajectory, despite the evolving global economic challenges, reveals GlobalData, a leading data and analytics company.

GlobalData’s Payment Card Analytics reveals that credit and charge card payments value in China registered a decline of 7.7% in 2024, due to challenges such as high inflation, geopolitical uncertainties, as well as the trade tariff dispute with the US.

Kartik Challa, Senior Banking and Payments Analyst at GlobalData, comments: “Despite lower penetration than debit cards, credit and charge cards are highly preferred for payments. Payment frequency for these cards stands at 55.3 times a year in 2025e—much higher than the equivalent figure for debit cards (33.6). Credit and charge card payment frequency is set to increase further to 79 transactions per card in 2029f. With the expansion of the middle-class workforce, increasing incomes, and heightened awareness of credit card benefits—fuelled by banks’ promotional campaigns—the adoption and utilization of credit cards are on the rise.”

Gradual improvement in payment infrastructure is also contributing to the rise of credit and charge cards in the country. The number of POS terminals per million inhabitants in China stood at 36,578 in 2024, which is higher compared to some of its peers such as Hong Kong (27,992), Japan (21,996), and India (9,005), though there is significant room for further expansion of POS infrastructure.

Despite the rising credit and charge card adoption, their usage is overshadowed by digital wallets. Chinese consumers prefer digital wallets for low-value daily transactions due to their convenience and wide merchant acceptance. Central bank PBOC and card issuers are taking steps to boost card payments. For instance, PBOC reduced its one-year loan prime rate (LPR), a benchmark for most loans such as credit cards, from 3.45% in June 2024 to 3% as of 21 July 2025. This is expected to have a positive impact on credit card spending in 2025 and beyond.

Likewise, the government is taking steps to control household debt in the country, such as requiring financial institutions to set defined maximum and minimum limits for installment payments, with repayment periods expanding from existing five years to seven years. These measures are designed to assist customers in managing their financial obligations more effectively.

Challa concludes: “China’s credit and charge card payments market is projected to maintain upward trajectory over the next five years. However, the country’s economy may encounter challenges due to the potential repercussions of the recent global trade disputes arising from US import tariffs. Also, high preference for digital wallet payments remains a challenge for their faster adoption. Overall, the credit and card payments market is forecasted to grow at a CAGR of 7.0% between 2025 and 2029 to reach CNY50.3 trillion ($7.0 trillion) in 2029.”