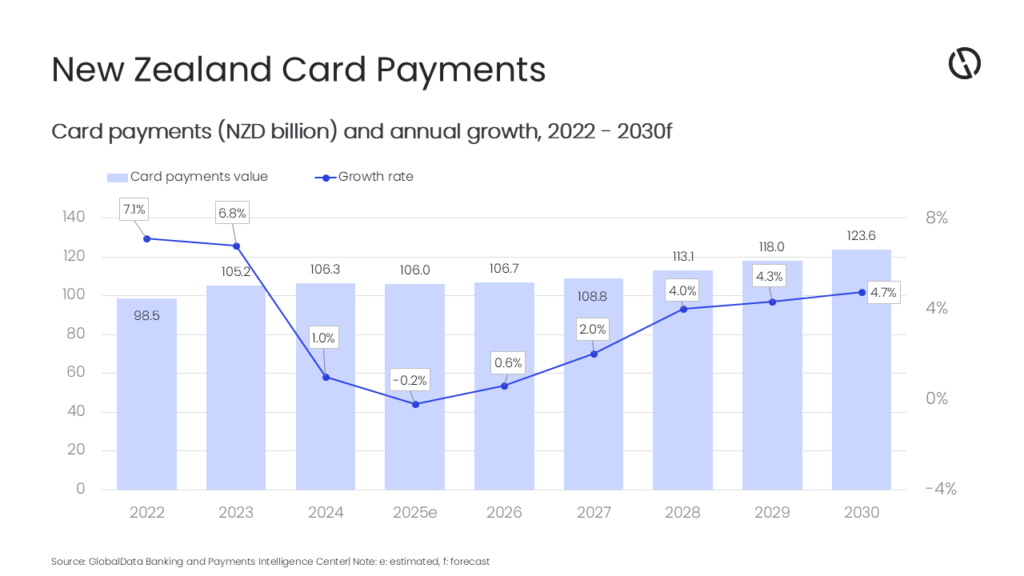

The New Zealand card payments market is forecast to reach NZD106.7 billion ($62.1 billion) in 2026, supported by strong consumer migration toward electronic payments, widespread adoption of contactless cards, and well-established digital infrastructure, according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Payment Cards Analytics reveals that the total card payment value in New Zealand registered an estimated compound annual growth rate (CAGR) of 3.6% over 2021-2025 to reach NZD106 billion ($61.7 billion) in 2025, reflecting continued traction in card-based spending driven by high financial awareness, consumer incentives from banks, and government initiatives favouring cashless transactions.

Poornima Chinta, Senior Banking and Payments Analyst at GlobalData, comments: “The New Zealand payment card market remains highly developed and competitive. Regulatory efforts to cap interchange fees, increasing awareness of electronic payments, and expanding merchant acceptance infrastructure, alongside the issue of contactless debit cards by all major banks, have reinforced consumer confidence in card payments. However, global risks—geopolitical conflicts, import tariffs, inflationary pressure—pose potential obstacles to growth.”

Debit card payments represented 48.9% of the total card payment value in New Zealand in 2025, driven by very high levels of bank account ownership and regulatory policies promoting low-cost bank accounts. The proliferation of fintechs and digital-only banks is further driving banking and card penetration. In October 2025, the fintech company Emerge launched personal banking services in New Zealand. Currently, the bank offers Mastercard physical and virtual cards to its customers.

Conversely, credit and charge cards accounted for 51.3% of total card payment value in 2025, slightly exceeding debit cards in value share. The segment has benefitted from consumers seeking value-added features—such as rewards, cashback, travel perks—and greater uptake of ecommerce, where credit cards are frequently preferred. However, increasing popularity of buy now, pay later (BNPL) solutions may place competitive pressure on credit card spending, particularly among younger consumers.

Other important factors driving card payments include the rapid spread of contactless payment technology. All major banks in New Zealand now issue contactless debit cards, and many merchants have upgraded POS infrastructure to support contactless transactions.

Regulatory measures are further reinforcing card adoption. In July 2025, the New Zealand Commerce Commission capped interchange fees for both domestic and international card transactions. For domestic cards, debit fees remain at 0.2% for contactless and 0.6% for online use, with no fee for swiped or inserted transactions. Credit card fees have been cut to 0.3% in person and 0.7% online, down from 0.8%, effective December 2025.

For international cards, the caps are 0.6% for foreign debit in person and 1.4% online, and 0.7% in person and 1.5% online for credit; these take effect in May 2026. These changes reduce costs for merchants and promote fairness, boosting debit and electronic payment growth.

Chinta concludes: “Looking ahead, a continued growth in the total card payments is expected in New Zealand over the next five years driven by the sustained preference for electronic and contactless methods, ecommerce expansion, fintech innovation, and policies promoting financial inclusion and low fees. Nevertheless, geopolitical uncertainty and evolving competitive threats such as BNPL could moderate growth and reshape market dynamics. Total card payment value is forecast to grow at 4.7% in 2030 reach NZD123.6 billion ($71.9 billion).”