South Korea’s card payments market is projected to continue its strong growth over the next few years, driven by near-universal banking access for adults, an advanced payments infrastructure, and a lasting migration toward electronic transactions. Credit cards remain the dominant force driving the nation’s cashless economy, according to GlobalData, a leading intelligence and productivity platform.

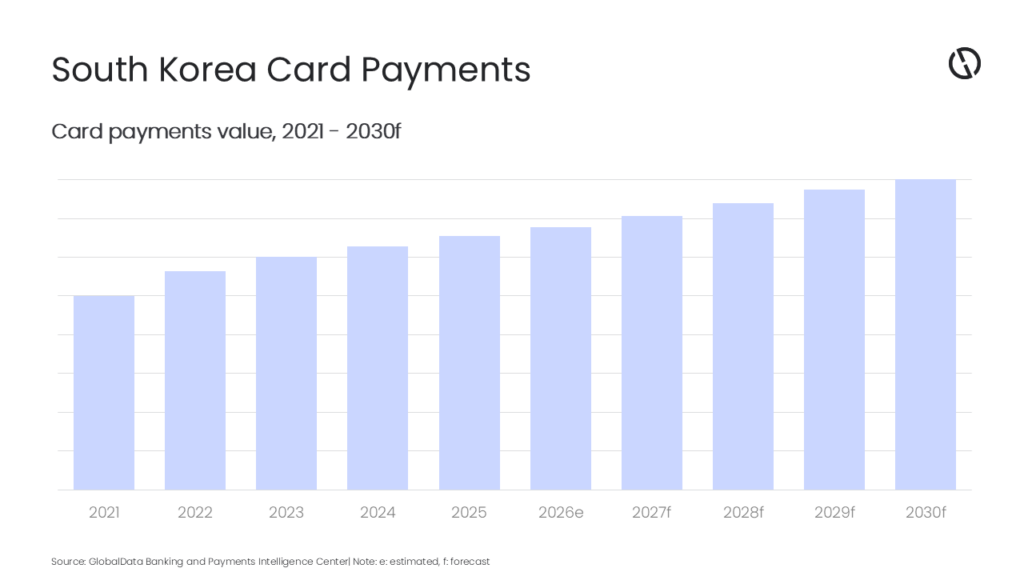

GlobalData’s Payment Cards Analytics reveals that the total card payment value in South Korea registered a robust growth in last five years, reflecting a shift from adoption-led expansion to steadier growth, even as enabling factors—such as increasing POS penetration, rising ecommerce demand, and digital-only bank competition—continue to underpin card usage.

Ravi Sharma, Lead Banking and Payments Analyst at GlobalData, comments: “South Korea’s card payments outlook is firmly positive. Between its highly banked population, widespread POS and network acceptance, and a public increasingly comfortable with electronic payments across all purchase types, the fundamentals are strong. Although external geopolitical and economic headwinds may introduce near-term volatility, the core structural shift away from cash remains intact.”

Debit issuance is thriving thanks to the affordable and user-friendly financial services, especially from digital-only banks like KakaoBank, Kbank, and Toss Bank. For instance, Kbank—serving some 16 million customers—bundles debit cards with basic bank accounts, making them pervasive for everyday spend.

When measured by transaction volume and value, credit and charge cards remain dominant. Their strength lies in consumer preference for rewards, cashback programs, instalment plans, flexible repayment, and broad merchant acceptance. These benefits make them the preferred instrument for discretionary and larger-ticket purchases.

Furthermore, contactless payments are increasingly accepted, especially in retail, transit, and dining sectors, helping to drive adoption, speed of transaction, and hygiene perceptions post-pandemic.

The rollout of modern POS devices and upgrades in merchant acceptance (SMEs included) are enhancing convenience and reliability. Meanwhile, authentication improvements—such as biometric verification, tokenization, and two-factor or risk-based checks—are reinforcing consumer trust and regulatory compliance.

Younger consumers are showing greater willingness to use digital payments over cash, influenced by social media, e-commerce, and peer norms. Also, urbanization and higher income levels reinforce demand for convenience and value-added services, while older population segments are also being pulled along via inclusive services and outreach.

Sharma concludes: “GlobalData expects sustained expansion in South Korea’s card payments market, anchored by deeply rooted consumer preference for digital payments, continuous innovation in both card-linked services and acceptance methods, and the resilience offered by strong payment infrastructure. Short-term pressures—such as energy price fluctuations or international trade disruptions—may influence variability in consumer spending, but the overall trajectory appears firmly upward.”