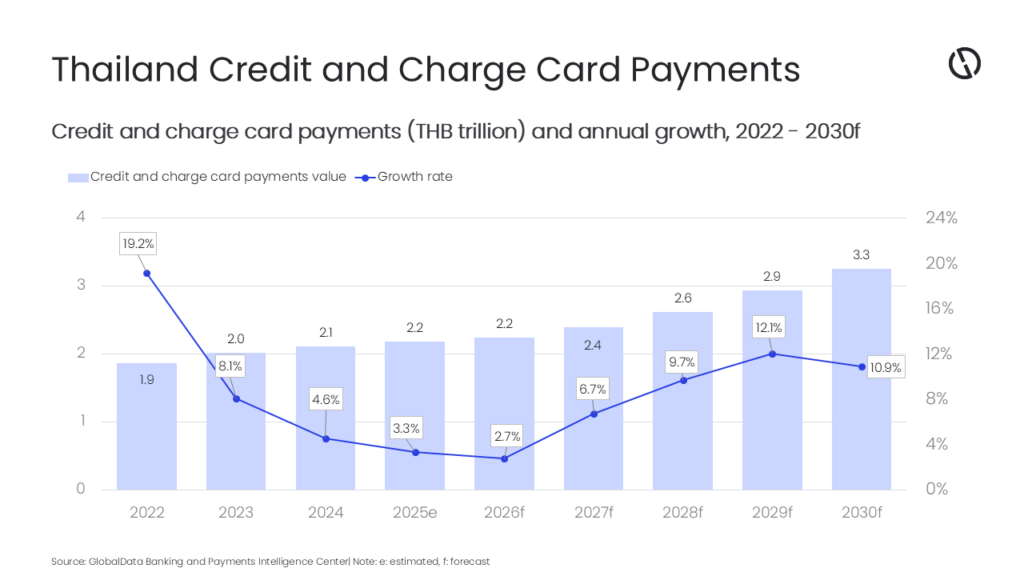

The Thailand credit and charge card payments market is projected to increase by 2.7% in 2026 to reach THB2.2 trillion ($68.1 billion), supported by a gradual increase in payment card usage, expanding payment infrastructure, and ongoing government initiatives, according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Payment Cards Analytics reveals that credit and charge card payment value in Thailand registered an estimated compound annual growth rate (CAGR) of 8.6% over 2021-2025 to reach THB2.2 trillion ($66.3 billion) in 2025, reflecting rising consumer spending and accelerating adoption of cashless and digital payments in the country.

Shivani Gupta, Lead Banking and Payments Analyst at GlobalData, comments: “Though credit and charge card penetration remains relatively low at 0.4 cards per 100 people in 2025, they remain the dominant form of payment cards in Thailand. This is largely supported by bank incentives such as cashback, rewards, discounts, and instalment plans, alongside rising adoption among the growing middle class and younger working population.”

Thai consumers are increasingly using credit and charge cards for payments, with the frequency of payments per card standing at 38.6 times in 2025, much higher compared to just three times for debit cards. This is driven by banks offering flexible repayment options and value-added benefits such as cashback, reward points, discounts, and installment facilities. For instance, card issuer Krungthai Card, in partnership with travel company Traveloka, offers its credit cardholders three-or six-month installment payment options on travel bookings above THB3,000 ($87.02).

To provide relief to indebted households, the Central Bank has extended the policy requiring minimum credit card installment payment rate of 8% till 31 December 2026, extending it beyond the original 31 December 2025 deadline. By maintaining a lower minimum payment rate, the Central Bank aims to support households in maintaining their financial stability and avoiding further indebtedness. Further, debtors who make at least the minimum payment are eligible for a 0.25% interest reduction on their outstanding balances.

Additionally, to drive credit card adoption in Thailand, Visa introduced “Scan to Pay with Visa QR Credit” service in May 2025. The solution enables Visa credit card holders to scan a QR code at checkout and pay directly from their Visa credit card, without needing a physical card. Users can access this payment method through their issuer’s mobile banking app. Such innovations are expected to sustain momentum in credit card usage and encourage consumers to use credit cards for regular, everyday purchases.

Gupta concludes: “Looking ahead, the Thai credit and charge card market is poised for sustained growth over the next five years, driven by the expanding digital payment infrastructure, incentives from banks and card issuers, supportive regulatory policies, and the shifting preferences of younger and more affluent consumers toward cashless transactions. The market is projected to register a CAGR of 9.8% between 2026 and 2030, to reach THB3.3 trillion ($99 billion) in 2030.”