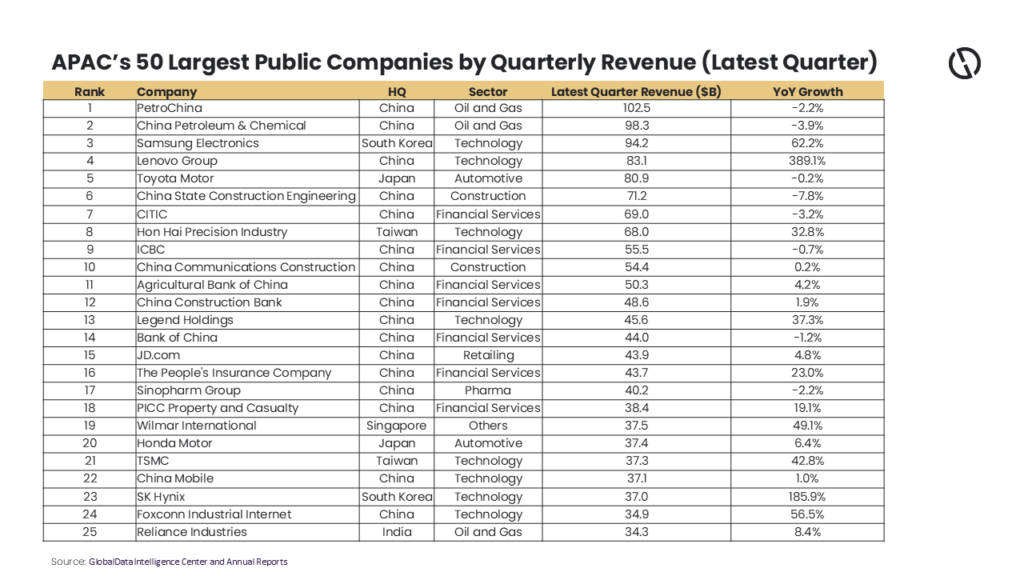

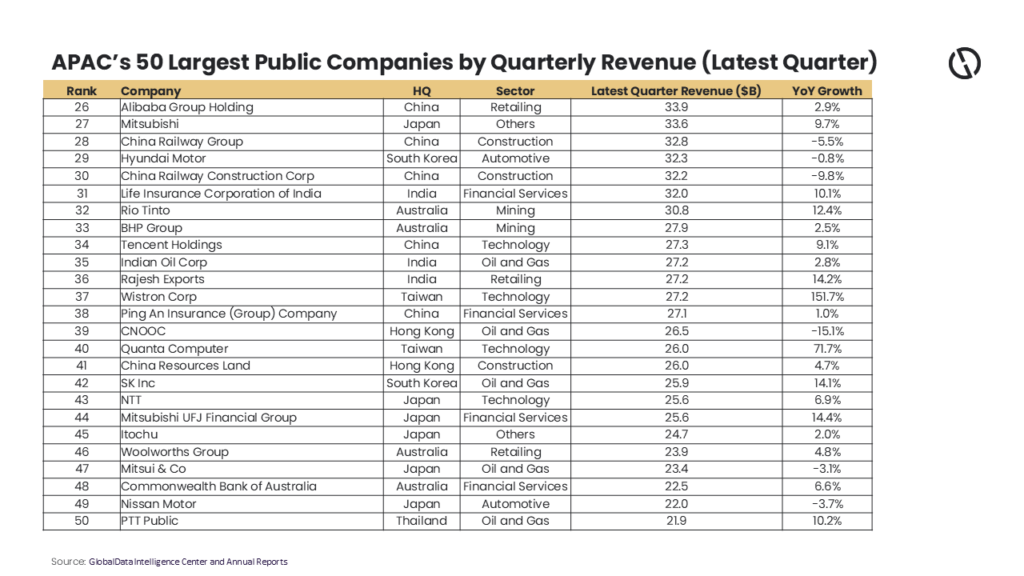

The latest quarterly revenue figures from Asia-Pacific’s (APAC) 50 largest listed companies reveal a region increasingly split between two powerful forces: the artificial-intelligence (AI) investment boom and a slowing industrial economy. While semiconductor and electronics champions delivered extraordinary growth, energy, construction and several China-linked cyclical businesses continued to grapple with weak demand, property-market stress and commodity volatility, according to GlobalData, a leading intelligence and productivity platform.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “The headline story belongs to memory. South Korea’s Samsung Electronics posted a remarkable 62.2% revenue increase, supported by record demand for AI memory chips, high-bandwidth memory (HBM), enterprise storage and premium smartphones. On the earnings call, management declared the memory upcycle structural rather than temporary, citing supply constraints and customers prioritising volume over price; customer demand for high-bandwidth memory already exceeds planned production capacity for the next three years.

“Taiwan’s TSMC grew 42.8%, reflecting sustained demand for advanced-node chips used in AI accelerators, cloud infrastructure and high-performance computing. The company continues to expand capacity for leading-edge manufacturing and advanced packaging as hyperscale AI spending remains robust.”

The AI wave also transformed memory suppliers. SK Hynix reported revenue growth of 185.9%, benefiting from its dominant position in HBM used by AI servers. Industry demand remains so strong that customers have reportedly secured substantial future supply commitments.

The ripple effects extended across hardware supply chains. Hon Hai Precision Industry, Wistron, Quanta Computer, and Foxconn all benefited from AI server assembly and data-center infrastructure spending. Meanwhile, China’s Lenovo Group and parent Legend Holdings gained from enterprise PC refresh cycles and infrastructure demand.

In contrast, Asia’s traditional energy heavyweights struggled.

Grandhi adds: “China’s PetroChina and China Petroleum & Chemical reported revenue declines of 2.2% and 3.9%, respectively. Lower crude prices, weaker domestic fuel demand, shrinking refining margins and China’s accelerating electric-vehicle adoption weighed on performance. Sinopec’s refining-heavy model has been particularly exposed to margin pressure.

Even offshore producer CNOOC saw revenue fall 15.1%, highlighting how softer commodity prices offset production gains.”

Automotive results reflected a mature industry facing uneven demand. Toyota Motor remained essentially flat, while Hyundai Motor and Nissan Motor posted modest declines. The sector continues to face intense EV competition from Chinese manufacturers, pricing pressure and slower global vehicle demand. By comparison, Honda Motor achieved moderate growth through stronger motorcycle and hybrid sales.

China’s domestic economy remains another dividing line. Construction giants including China State Construction Engineering, China Railway Group and China Railway Construction recorded revenue declines, reflecting persistent weakness in real estate investment and slower infrastructure activity. Financial institutions such as ICBC and Bank of China showed limited growth as lower interest rates compressed margins.

Yet consumer-facing businesses proved more resilient. JD.com, Alibaba Group, and Tencent Holdings delivered modest gains, supported by cloud services, digital advertising and stabilizing consumption trends.

Elsewhere, commodity-linked groups showed surprising strength. Singapore’s Wilmar International surged 49.1%, while Australia’s Rio Tinto and BHP Group benefited from resilient demand for iron ore and minerals critical to electrification and infrastructure.

GlobalData anticipates that APAC enters the second half with two competing forces: a powerful AI investment cycle funnelling capital into semiconductors, servers, cloud infrastructure and advanced manufacturing, and a slower-growth backdrop driven by China’s property slump, uneven consumer demand and trade fragmentation.

Grandhi concludes: “A potential Strait of Hormuz crisis adds a major wildcard. Higher oil prices would likely benefit upstream producers like PetroChina and CNOOC, while squeezing refiners, manufacturers and transport-heavy industries. Energy importers such as Japan, South Korea and India would face a sustained cost shock that hits consumption and margins.

“Meanwhile, US–China tech tensions continue to push supply-chain diversification across Taiwan, South Korea, India and Southeast Asia. APAC isn’t decoupling from global volatility; it’s where AI capital concentration, China’s property unwind, and Middle East energy disruption collide—widening the gap between AI winners and exposed laggards.”