Asia-Pacific’s (APAC) largest banks are entering a more fragmented era. The region’s financial heavyweights still dominate global rankings by revenue, but the latest numbers reveal a widening divergence between China’s state-backed lenders, Japan’s globally exposed megabanks, and India’s fast-expanding retail franchises, according to GlobalData, a leading intelligence and productivity platform.

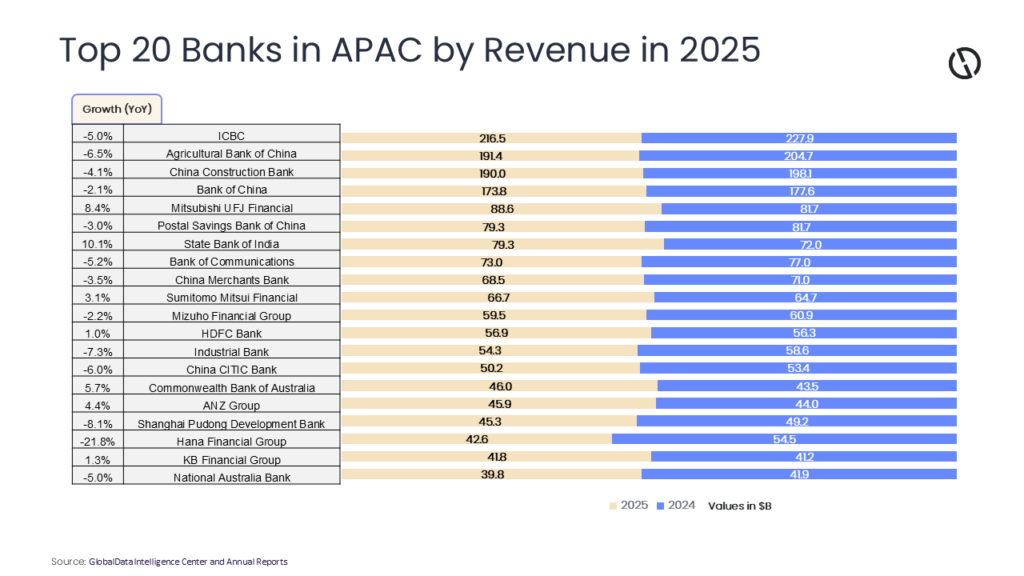

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “China’s Big Four—ICBC, Agricultural Bank, China Construction, and Bank of China—collectively shed roughly $36 billion in revenue year-on-year. It is the arithmetic consequence of Beijing’s deliberate policy to cut mortgage rates and compress net interest margins as a lifeline to a property sector still working through its most severe downturn in a generation.

Shanghai Pudong Development Bank dropped 8.1% to $45.3 billion and Industrial Bank Co fell 7.3% to $54.3 billion—both mid-tier lenders with above-average exposure to the commercial real estate sector, where troubled developers have forced loan restructurings that depress fee income alongside interest income. China CITIC Bank’s 6.0% decline to $50.2 billion tells a similar story.”

While China contracts, Japan’s megabanks are living through their best revenue environment in two decades. Mitsubishi UFJ Financial Group posted an 8.4% jump to $88.6 billion—the largest absolute revenue gain in this cohort. The driver is straightforward: the Bank of Japan’s exit from its decade-long negative-rate policy, which formally ended in March 2024, has allowed Japanese banks to begin earning actual returns on their massive domestic deposit bases and loan books. Every 25-basis-point rate hike adds billions to net interest income for an institution of MUFG’s scale.

Sumitomo Mitsui Financial Group rose 3.1% to $66.7 billion for the same reasons, though the effect has been somewhat offset by weakness in equity commission income and unrealized losses on the bond portfolios Japanese banks accumulated during the yield-curve-control years. Mizuho, meanwhile, edged down 2.2% to $59.5 billion—partly because it carries a higher proportion of fee-dependent businesses, including investment banking, where deal flow in Japan was uneven in 2025.

Grandhi adds: “State Bank of India posted double-digit revenue growth of 10.1%, outperforming most regional peers. Strong credit demand, expanding retail lending and improving asset quality continue to support India’s banking sector. Consumer loans, infrastructure financing and digital payments growth remain key tailwinds.

“HDFC Bank Ltd grew only 1%, but the muted figure partly reflects the normalization period following its merger integration with Housing Development Finance Corp. Investors remain focused on deposit mobilization and margin stability rather than pure top-line acceleration.”

Hana Financial’s reported revenue fell 21.8% in dollar terms from $54.5 billion to $42.6 billion, but the drop is exaggerated by a weaker won in 2024–25. In won terms, results were down yet manageable, pressured by softer household lending and higher provisions for delinquent small-business loans. KB Financial’s 1.3% reported rise likely masks stronger underlying growth once currency effects are stripped out.

Commonwealth Bank of Australia and ANZ Group grew revenues 5.7% to $46.0 billion and 4.4% to $45.9 billion as Australia’s mortgage market stayed resilient despite rate hikes. CBA benefited from low-cost retail deposits. NAB fell 5.0% to $39.8 billion, hurt by business and agriculture margin pressure.

Grandhi concludes: “GlobalData anticipates the outlook for APAC banking is increasingly shaped by geopolitics, supply-chain shifts, and regulatory demands for resilience. While Chinese banks prioritize economic stability, Indian and Japanese lenders are positioning to capture capital, with future success favoring institutions that navigate a politically fragmented, slower-growth environment.”