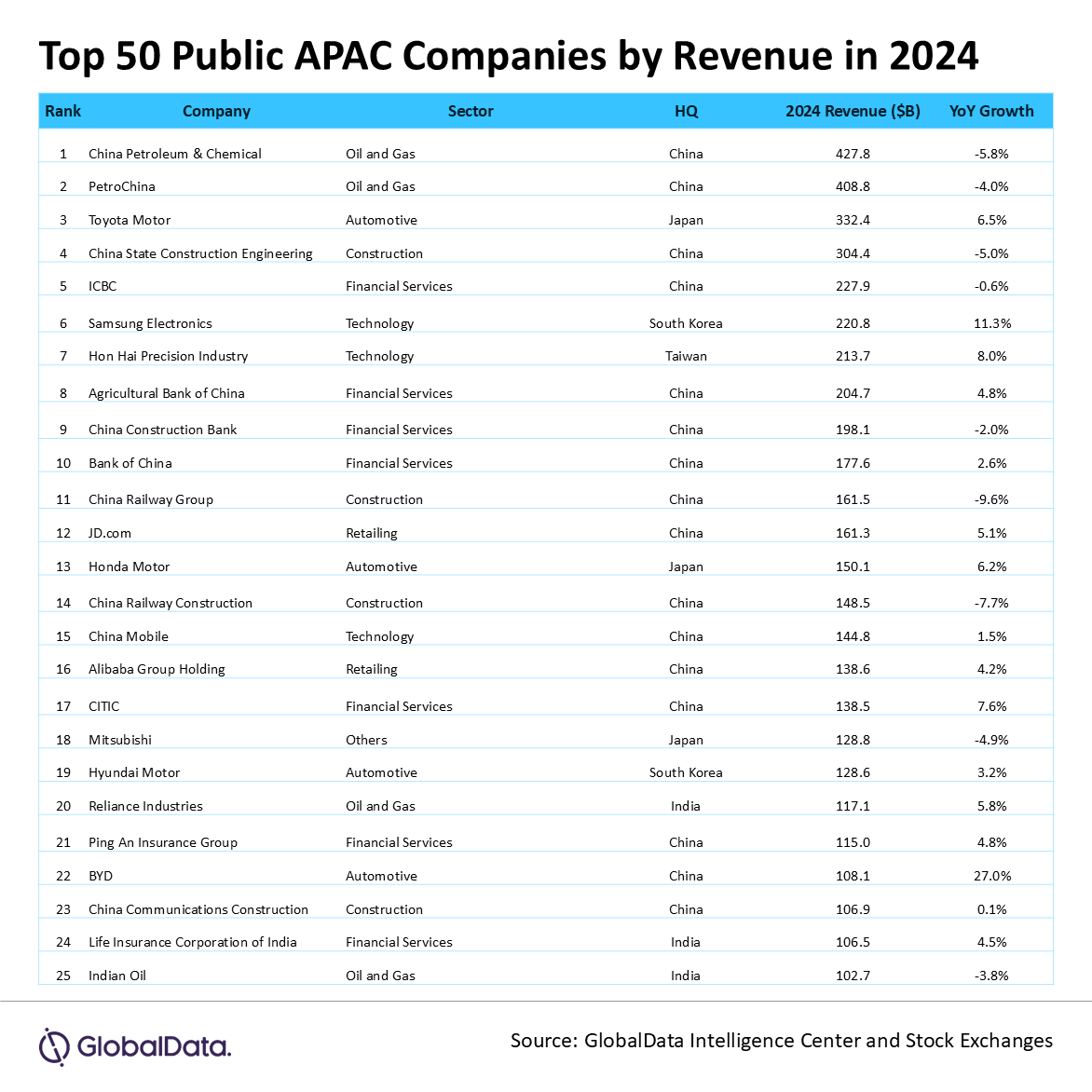

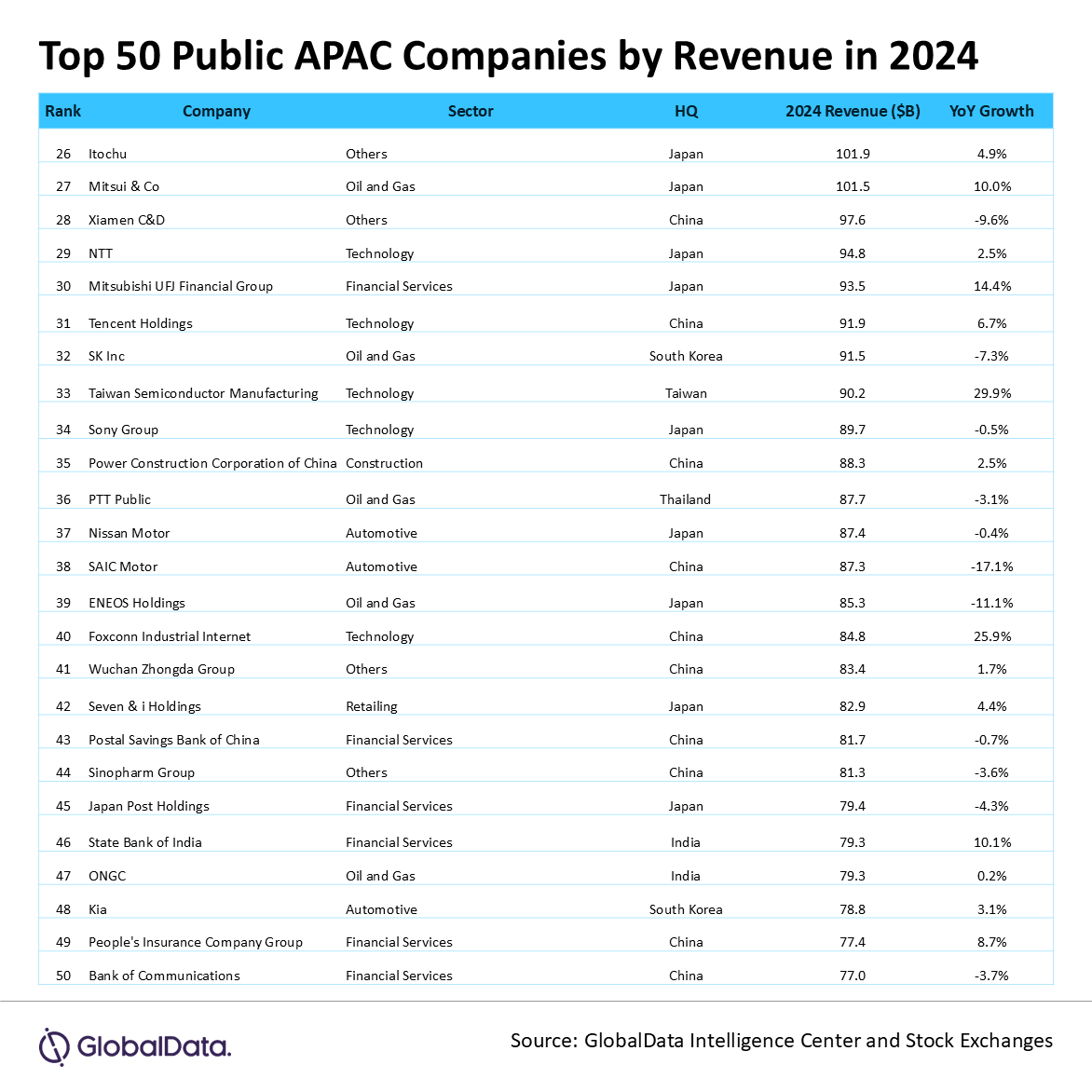

- China dominates the list with 26 companies

- BYD, TSMC, and Foxconn gain over 25% in revenue

- Financial services sector tops the list with 13 companies

The Asia-Pacific (APAC) region’s top 50 listed companies reported a modest 1.2% year-on-year (YoY) revenue growth in 2024, reaching a staggering $6.8 trillion. This slight uptick was primarily fueled by the booming technology sector, where demand for AI chips is skyrocketing. Additionally, the retail and automotive industries also experienced a resurgence, driven by the rapid rise of e-commerce and a rebound in consumer spending, according to GlobalData, a leading data and analytics company.

An analysis of GlobalData’s Company Reports Database reveals that three companies from the top 50 list reported an increase of over 25% in their revenue, while eight companies reported an over 5% decline in revenue. The list includes 26 companies from China, of which, 14 companies registered YoY growth.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “In 2024, the macro landscape was dominated by renewed trade uncertainties, particularly between the US and China, casting a shadow over APAC’s export-driven sectors. As global orders dwindled and tariffs soared, Asian manufacturers—especially in Japan, South Korea, and Taiwan—felt the squeeze. However, this turmoil opened doors for ASEAN and India, which emerged as attractive alternative production hubs amid multinational supply chain shifts. On a brighter note, a surge in domestic capital flows, a strong push for AI adoption, and innovative business models provided a lifeline for select sectors, helping to offset the external pressures.”

China

China firmly holds its ground with 26 of its companies featuring among the top 50, showcasing the immense scale of its domestic market and state-supported enterprise model. Despite facing revenue declines of 5.8% and 4.0% due to softness in the energy sector and crude oil price corrections, China Petroleum & Chemical Corp (Sinopec) and PetroChina continue to dominate the rankings at No. 1 and No. 2, respectively.

In the financial services arena, heavyweights like ICBC, China Construction Bank, and Agricultural Bank of China underscore China’s pivotal role in global banking. However, most of these institutions reported flat or slightly declining revenues, highlighting the challenges of a maturing credit market and a sluggish property sector recovery.

On a brighter note, tech giants such as Tencent, Alibaba, and China Mobile enjoyed stable growth, even though they did not feature among the top 10 companies by revenue. Meanwhile, BYD is making waves as a rising electric vehicle (EV) powerhouse, boasting an impressive 27% YoY revenue growth —a testament to Beijing’s push for EV innovation and global competitiveness.

Japan

Japanese companies secured 12 spots on the list, with Toyota Motor Corp leading the way, achieving 6.5% revenue growth to $332.4 billion and maintaining its third-place global rank. The auto sector thrived due to easing semiconductor shortages and strong exports, while trading houses like Itochu and Mitsui showcased Japan’s diverse trading prowess.

Grandhi adds: “TSMC skyrocketed nearly 30% YoY, securing the 33rd spot on the list. As the globe’s leading chipmaker, TSMC plays a pivotal role in the US-China tech rivalry. Its impressive growth, even amid high-end chip export restrictions to China, underscores Taiwan’s geopolitical and economic significance.”

India

India made its mark with five entries on the top 50 list, which include major players like Reliance Industries, Indian Oil, State Bank of India, and Life Insurance Corporation (LIC). Reliance achieved a solid 5.8% YoY revenue growth, fueled by its robust oil refining and retail operations. Meanwhile, LIC and SBI reported moderate growth, reflecting the benefits of India’s expanding middle class and the ongoing formalization of financial services.

South Korea and Southeast Asia

South Korea’s Samsung Electronics posted an 11.3% YoY growth, riding on the demand for AI hardware and memory chips. Hyundai and Kia also delivered solid performance amid robust global EV and SUV sales.

Thailand’s PTT Public, despite experiencing a minor contraction, remains Southeast Asia’s top revenue-generating firm, demonstrating the region’s energy dependency and PTT’s monopoly-like reach.

Grandhi concludes: “The 2025 landscape will be defined by escalating US-China trade tensions, tighter technology transfer restrictions, and weaker external demand. While central banks may initiate rate cuts, rising tariffs could disrupt asset prices. Companies with strong domestic markets are poised to thrive, while export-dependent firms may struggle. Nonetheless, APAC’s long-term fundamentals remain strong, with regional supply chain initiatives fostering new leaders.”