Europe’s biggest banks are seeing revenues shrink or stagnate, even as profits keep rising. Among the top 20 Europe, the Middle East and Africa (EMEA) lenders by revenue, 12 posted year-over-year declines in their top line in 2025, yet most still grew net income, in some cases dramatically. That divergence reflects a deliberate post-rate-cycle adjustment playing out across the continent, according to GlobalData, a leading intelligence and productivity platform.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “The region’s biggest lenders posted mixed results as slowing loan growth, softer dealmaking activity and mounting geopolitical risks weighed on performance. While several banks continued to deliver double-digit profit growth, revenue momentum weakened across much of Western Europe.”

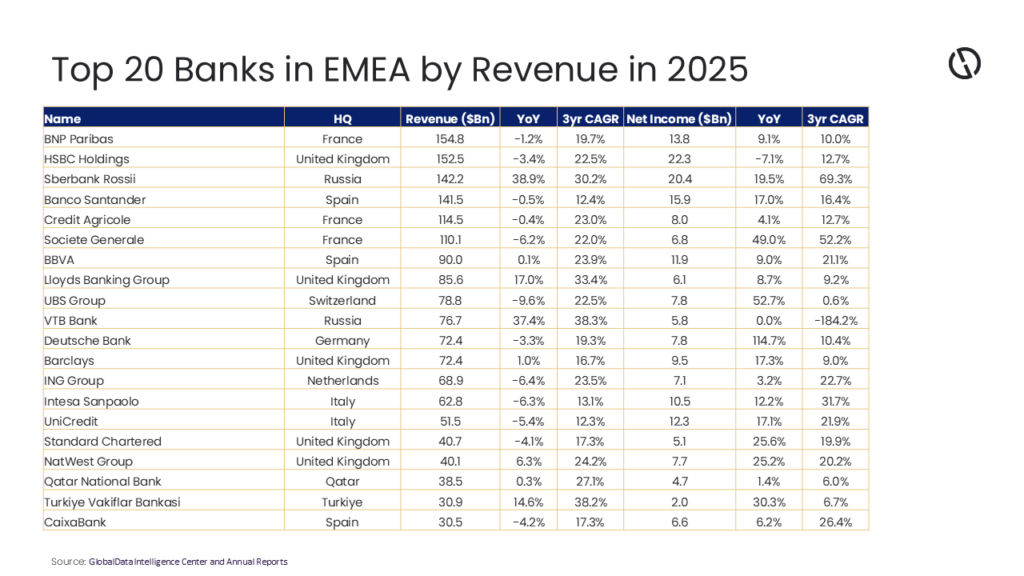

France’s BNP Paribas remained the region’s largest bank by revenue at $154.8 billion in 2025, though revenue slipped 1.2% from a year earlier. Net income still rose 9.1%, reflecting resilient corporate and investment banking and disciplined cost management. Domestic retail operations, however, stayed under pressure from regulated savings products and muted credit demand in France.

HSBC Holdings reported a 3.4% decline in revenue and a 7.1% drop in net income. It benefited enormously from higher global interest rates over the past three years, but margin expansion is moderating. Weakness in China’s property market and slower trade flows across Asia also weighed on its commercial banking franchise.

Grandhi adds: “Russian lenders stood apart. Sberbank’s revenue climbed 38.9% to $142.2 billion and net income rose 19.5% in 2025, producing a three-year CAGR of 69.3% for earnings. However, these are ruble-denominated businesses in a wartime economy under capital controls, with benchmark rates above 16%. VTB’s picture is starker: revenue up 37.4%, but its three-year CAGR for net income is negative 184.2%, reflecting catastrophic 2022 losses when sanctions first hit.”

Spanish lenders continued to outperform. Banco Santander lifted net income 17% despite flat revenue growth, helped by strong Latin America operations and improved efficiency. BBVA benefited from robust earnings in Mexico, where higher rates and loan expansion supported margins.

Societe Generale delivered one of the sharpest profit recoveries, with net income jumping 49% after restructuring, reduced exposure to underperforming businesses and stabilization in retail banking. Revenue still declined 6.2%, underscoring how hard sustained top-line growth is in mature markets.

In the UK, banks benefited from resilient consumer spending and higher interest margins. Lloyds increased revenue 17% on mortgage repricing and improved spreads. NatWest and Barclays also posted healthy profit gains as retail and corporate banking held up better than expected.

UBS remained in integration mode after taking over Credit Suisse. Revenue declined nearly 10%, though net income rose sharply as cost synergies and restructuring began feeding through. Deutsche Bank more than doubled net income on lower litigation costs, stronger fixed-income trading and restructuring gains, even as revenue contraction showed how Germany’s weak industrial economy continues to constrain activity. Italian lenders UniCredit and Intesa Sanpaolo also delivered strong profit growth despite declining revenue, benefiting from higher euro-zone rates and leaner structures.

Grandhi concludes: “GlobalData expects EMEA banks to face tougher conditions than those seen during the post-COVID-19 pandemic rate boom. US-China tensions and potential new US-EU tariffs could reduce trade-finance demand, while Middle East instability may keep energy prices, inflation and sovereign risk volatile. Expected ECB rate cuts in 2026 threaten to compress eurozone margins, and Basel IV rules will raise capital needs, limiting buybacks and dividends.

“Banks are likely to respond by accelerating digitization, cutting costs, and expanding wealth management and fee-based businesses. Diversified, fee-heavy groups like UBS, Santander and BBVA may prove more resilient than domestic lenders.”