Global banking rankings have been reshaped by deregulation, a European value renaissance, and a strong investment banking cycle, with JPMorgan Chase firmly retaining the top position in the first quarter (Q1) of 2026. However, governance concerns in India and a resurgent US dollar are already casting uncertainty over recent gains, signalling that market leadership and valuations could shift again in the coming months across global markets, according to GlobalData, a leading intelligence and productivity platform.

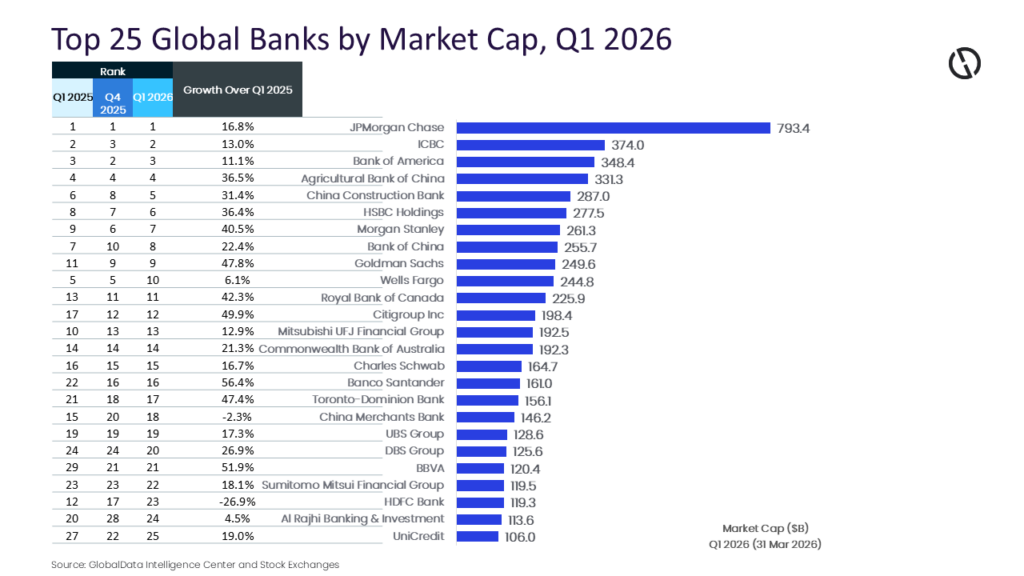

JPMorgan Chase retained the global crown at $793.4 billion, a 16.8% gain underpinned by a $20 billion technology budget, record trading revenues, and its unrivalled universal banking franchise. It is the one name on the leaderboard that commands consensus across every market cycle.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “Europe, however, delivered the year’s most striking narrative. The EURO STOXX Banks Index surged 76% in 2025 — its best performance since records began — as Banco Santander (+56.4%), BBVA (+51.9%), and UniCredit (+19.0%) underwent historic re-ratings. The catalyst: European banks had been trading at deep discounts to book value after years of negative rates and heavy regulation. A steepening yield curve, ECB rate normalisation, and a weaker US dollar through most of 2025 collectively unlocked a wave of global portfolio flows into European financials. Santander’s Latin American diversification and BBVA’s emerging-market rebalancing made each a standout beneficiary.”

On Wall Street, deregulation was the accelerant. America’s six largest banks collectively added $600 billion in market value in 2025. The Trump administration’s “Basel III Mulligan” — a softened capital framework releasing roughly $87.7 billion in system-wide capital relief — allowed banks to unlock billions for buybacks and lending. Goldman Sachs (+47.8%) completed its exit from consumer banking, doubling down on trading and wealth.

Citigroup (+49.9%) finally delivered on Jane Fraser’s restructuring, flattening its hierarchy from 13 management layers to eight and completing 20,000 job cuts. Morgan Stanley’s wealth arm pulled in $122 billion in new assets in Q4 2025 alone — a structural earnings floor that institutional investors rewarded handsomely.

Grandhi adds: “China’s state-owned banks Agricultural Bank of China (+36.5%), China Construction Bank (+31.4%) posted solid gains, riding Beijing’s fiscal stimulus and infrastructure spending. China Merchants Bank was the sole decliner (−2.3%), reflecting regulatory uncertainty around private-sector lenders.

“India’s HDFC Bank, however, suffered the most dramatic collapse in the ranking, tumbling from 5th to 23rd. A post-merger loan-to-deposit ratio approaching 100% had already strained margins when chairman Atanu Chakraborty resigned in March 2026, citing ‘differences over values and ethics.’ The stock shed 10% in three sessions; foreign investors pulled over ₹70,990 crore from Indian equities that month alone.”

The record valuations of 31 March are already under pressure. Trump’s “Liberation Day” tariffs knocked Citigroup 13% and Goldman Sachs 11% within days. More significantly, the US dollar, which fell over 9% in 2025, has staged a sharp reversal, climbing nearly 4% from January lows to a 10-month high above 100.64 on the DXY. The driver is the US–Iran conflict has effectively closed the Strait of Hormuz, triggering an energy price shock that has reignited inflation fears and pushed the Federal Reserve into a holding pattern, with markets now pricing no rate cuts before December 2026.

Grandhi concludes: “GlobalData anticipates that a stronger dollar is an unambiguous headwind for European banks, compressing the valuation gap that powered Santander, BBVA, and UniCredit’s re-rating and eroding dollar-translated earnings. For Asian energy importers Japan and India, rising oil costs squeeze margins and invite currency depreciation. For US investment banks like Goldman and Morgan Stanley, higher-for-longer rates support trading revenues; but consumer lenders face a twin threat from tariff-driven slowdown and proposed credit card rate caps. The banks that built capital strength and strategic clarity in 2025 are best placed to navigate what follows. The rankings of 31 March may look very different by 30 June.”