The fiscal year 2025 was one of the most divergent on record for global banking: at one extreme, state-owned Russian lenders capitalized on wartime interest rate regimes; at another, Chinese megabanks witnessed net interest margins compress under Beijing’s directive to support a slowing economy. Between these poles, US banks mostly held their ground while European lenders struggled for growth. What emerges is not a single banking cycle—but several, unfolding simultaneously across geographies, according to GlobalData, a leading intelligence and productivity platform.

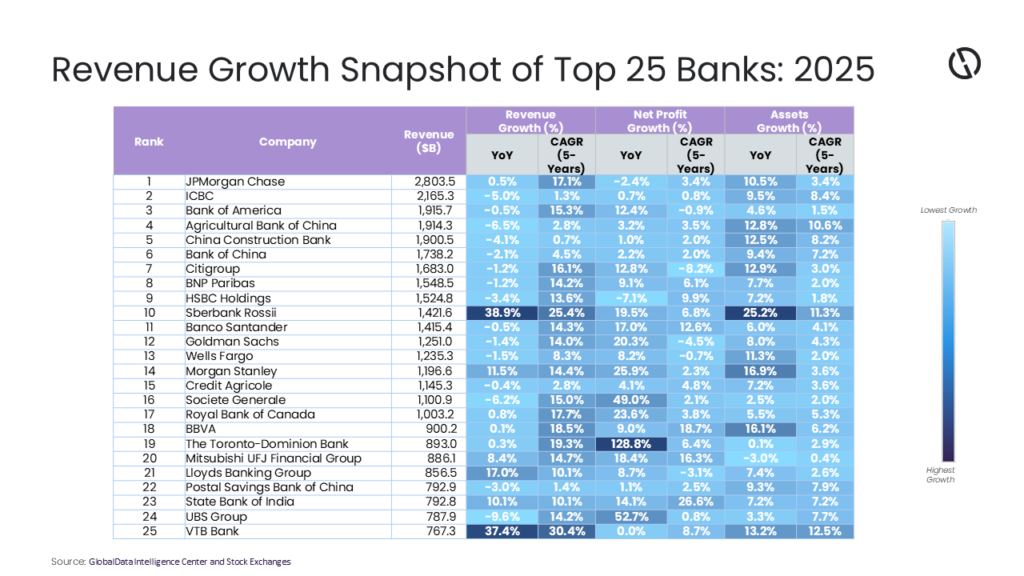

JPMorgan Chase & Co remains the revenue leader at $280 billion, though growth has slowed to 0.5% year-on-year (YoY) from a 17.1% CAGR since 2021. Net income slipped 2.4%, a modest decline that underscores a broader industry pattern: earnings momentum is cooling even as assets continue to rise. JPMorgan’s assets climbed 10.5% to $4.4 trillion, highlighting how deposit inflows and liquidity buffers remain elevated despite tighter financial conditions.

A similar dynamic is visible at Bank of America Corp and Citigroup Inc, where revenues dipped slightly while profits improved or stabilized. The divergence reflects lingering benefits from higher interest rates—supporting net interest income—offset by weaker dealmaking, higher funding costs and normalization in trading revenues after post-pandemic highs.

Chinese banks present a contrasting picture. Industrial and Commercial Bank of China Ltd, China Construction Bank Corp and Agricultural Bank of China Ltd all reported revenue declines ranging from 4% to 6.5%. Yet net income held steady or rose modestly.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “This reflects margin compression amid policy easing and lower lending rates, partially offset by cost controls and stable credit performance. Their balance sheets continue to expand rapidly—double-digit asset growth across the cohort—signalling ongoing credit support to the domestic economy despite weaker demand.”

European lenders show mixed recovery trajectories. BNP Paribas SA and Banco Santander SA posted resilient profit growth (9.1% and 17.0%, respectively), benefiting from higher rates in retail banking and geographic diversification. Meanwhile, HSBC Holdings Plc saw profits decline 7.1% despite solid multi-year growth, suggesting normalization after outsized gains tied to global rate cycles.

Among standout performers, Russia’s Sberbank Rossii and VTB Bank posted exceptional revenue growth—38.9% and 37.4%, respectively—alongside strong asset expansion.

Grandhi adds: “The surge reflects a rebound from prior-year disruptions and a domestically focused banking system operating under sanctions, where state support and limited competition have reshaped profitability dynamics rather than signaling broad-based efficiency gains.”

Japan’s Mitsubishi UFJ Financial Group Inc stands out for consistent profitability expansion, with net income up 18.4% and a 16.3% CAGR since 2021. The performance aligns with gradual monetary policy normalization in Japan, improving lending margins after years of ultra-low rates.

One subtle but important trend across the dataset is the persistent expansion of total assets even where revenues stagnate or decline. This suggests banks are still accumulating liquidity and extending credit, but at lower spreads. It also raises questions about capital efficiency, as balance sheet growth is not translating proportionally into earnings.

Another insight is the divergence between CAGR and current-year growth. Many banks show strong multi-year expansion—often above 14% revenue CAGR—yet flat or negative growth in 2025. This indicates that much of the post-2021 rebound has already been realized, and the sector is entering a more mature, slower-growth phase.

Grandhi concludes: “GlobalData anticipates that the global banking sector faces a more uncertain path ahead. In the US, the trajectory of interest rates and potential credit deterioration—particularly in commercial real estate—will shape profitability. In China, continued policy easing and structural economic slowdown may keep pressure on margins despite asset growth. European banks remain exposed to uneven growth and energy-linked economic risks.

“Geopolitical tensions, including prolonged conflicts and trade fragmentation, are likely to sustain volatility in capital flows and currency markets, benefiting trading desks but complicating long-term planning. Meanwhile, regulatory pressure on capital and liquidity is unlikely to ease. Overall, the era of easy gains from rising rates appears to be ending. The next phase will test banks’ ability to generate returns through efficiency, diversification and disciplined risk management rather than macro tailwinds alone.”