A memorandum of understanding (MoU) signed between the US and Iran recently has reopened the Strait of Hormuz and extended a ceasefire. Yet for global business, the MoU does not mark the end of the crisis; instead, it starts a 60-day negotiating clock on Iran’s nuclear programme, frozen assets, and Lebanon’s fragile ceasefire. The base-case outcome is a “phantom ceasefire” that keeps energy costs elevated and weighs on global growth well into 2027, according to GlobalData, a leading intelligence and productivity platform.

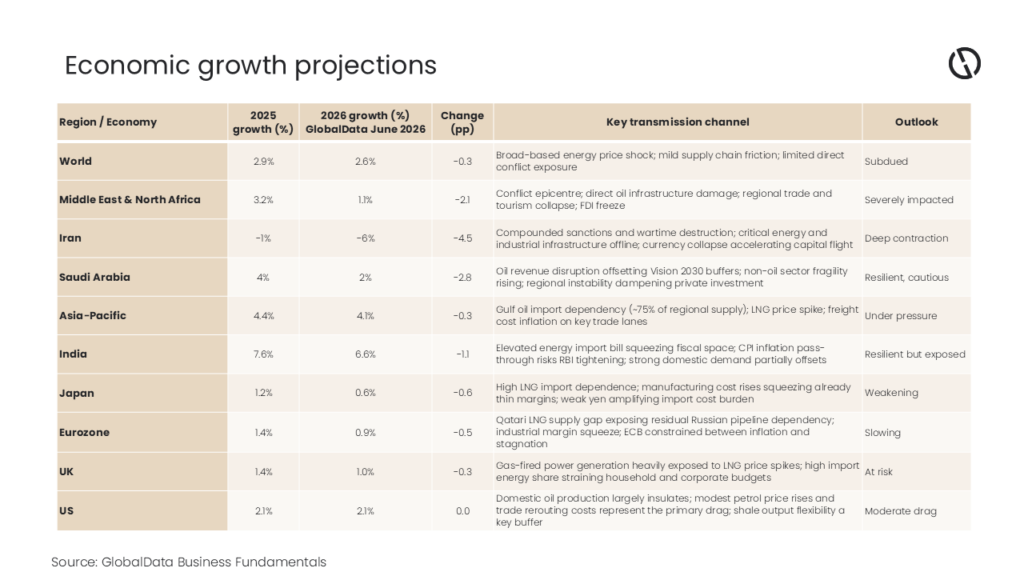

The economic damage from the 112-day conflict is already locked in. The Strait of Hormuz’s near-total closure drove global oil output down by 6.9 million barrels per day in Q2 2026, the largest quarterly fall since COVID-19. Brent crude surged past $120 per barrel, Qatari LNG faced force majeure, and GlobalData revised its 2026 global growth forecast down to 2.6%, from 2.9% in 2025. The reopening of the strait is material, but the damage is not yet over.

Ramnivas Mundada, Director of Economic Research and Companies at GlobalData, comments: “The MoU ends the shooting war. Whether it ends the economic war depends entirely on the next 60 days. Nuclear enrichment levels, Iran’s $24 billion in frozen assets, and Lebanon’s compliance are all unresolved. Markets have re-priced relief; what they have not re-priced is the risk of failure. Businesses that plan as if the crisis is over are making a dangerous assumption.”

What the MoU delivers, and what it defers

The MoU has four elements. First, the strait is reopening on alternative northern and southern routes while the main channel – containing an estimated 80 mines – is cleared. Second, a 60-day ceasefire extension reduces war-risk insurance premiums as traffic normalizes. Third, it creates a nuclear negotiating framework, covering a temporary moratorium on uranium enrichment and the disposition of Iran’s 440-kilogram stockpile of 60%-enriched uranium, as confirmed by the IAEA. Fourth, ceasefire compliance in Lebanon is linked to the overall deal – a provision Iran is already invoking after Israeli strikes continued post-signing.

Critically, the MoU does not lift sanctions, release frozen assets, or resolve the nuclear dispute. The US is pushing for a 20-year enrichment pause; Iran will not go above ten years. All final-status issues are deferred to the 60-day window.

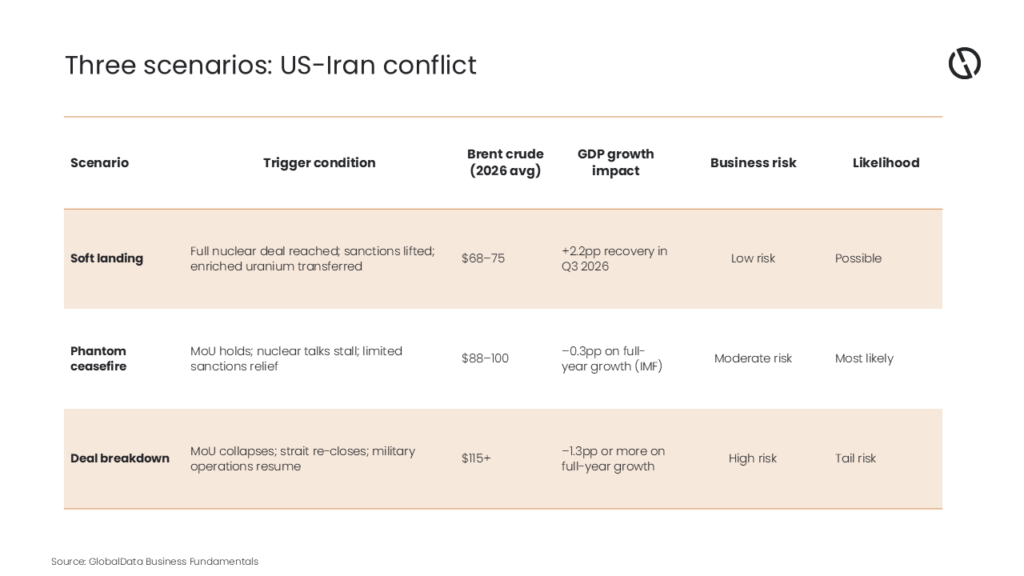

Three scenarios: what businesses must plan for

GlobalData’s scenario analysis, grounded in IMF and World Bank modelling, sets out three paths from the 60-day window.

Under GlobalData’s base case scenario, the “phantom ceasefire,” Brent crude’s range will sustain inflationary pressure across energy-importing economies into 2027. The IMF estimates that for every sustained $10 increase in oil prices, global GDP growth falls by 0.2–0.3 percentage points – a drag that compounds if the disruption persists beyond two quarters.

Asymmetric impact: who is most exposed

GlobalData cut its 2026 Middle East and North Africa growth forecast by 2.6 percentage points to 1.1%. Iran faces a contraction of 5.9%, a swing of more than seven points from its January baseline. Saudi Arabia’s forecast was trimmed from 4.6% to 1.7%. Asia’s large energy importers – China, India, Japan, and South Korea – absorb the bulk of Gulf oil exports and face higher energy bills and persistent inflation pass-through. Europe confronts an LNG supply gap as Qatari exports remain constrained, with ECB rate-cut timelines pushed back as inflation re-accelerates.

Disruption arriving at the northern-hemisphere planting season threatens harvests and food security across Africa, South Asia, and Latin America.

The 60-day clock: four variables to watch

- Nuclear enrichment framework: The US seeks a 20-year moratorium; Iran will not exceed ten years. This is the most likely cause of deal failure.

- Frozen asset release: Iran expects $12 billion before final negotiations begin. The US has not released any funds to date.

- Lebanon compliance: Iran has declared any continuing Israeli military presence a violation of the MoU. Israel has stated it will maintain troops in southern Lebanon indefinitely, a live tripwire.

- Gulf production restarts: Iraqi output from the Zubair field fell more than 70% during the conflict. Damaged infrastructure and logistics backlogs will constrain recovery for months, even with the strait open.

Business implications

GlobalData advises businesses to plan against the phantom ceasefire as the central case. For European industrials, the structural LNG shift is already underway: US supply at premium prices is the new baseline through at least 2027. Supply chain managers reliant on Gulf inputs should stress-test Q3 and Q4 cost assumptions against sustained disruption. Financial risk managers should treat the frozen asset negotiations as the single most sensitive near-term variable for the Brent price trajectory.

Mundada concludes: “The MoU is a necessary first step, but not a sufficient one. Businesses and investors should use this period of relative stability to build resilience, not to wind down their contingency plans. The potential consequences of deal failure are larger than markets are currently pricing.”