The top 20 public insurance companies in Asia-Pacific (APAC) reported subdued premium growth in 2023 owing to broader economic and regulatory challenges such as inflationary trends, and implementation of IFRS 17. As a result, their average premium earned* grew by a paltry 1.3% while experiencing a modest 5.5% uptick in total revenue, reveals GlobalData, a leading data and analytics company.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “In 2023, one of the roadblocks for insurers came in the form of IFRS 17. The new accounting standard has increased complexity, changed financial reporting, and affected capital requirements. While these changes have presented challenges, they have also brought benefits such as improved transparency, risk management, and comparability.”

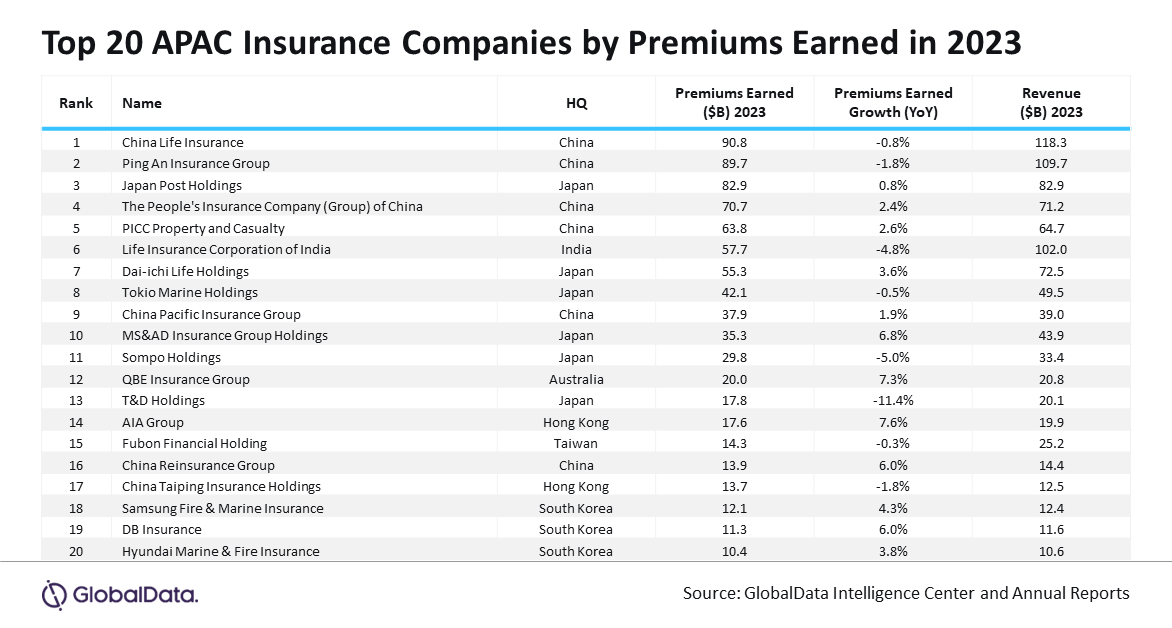

Of the top 20, 12 insurers reported year-on-year (YOY) growth in premium earned in 2023. Notable performers were AIA Group, QBE Insurance, and MS&AD Insurance Group.

AIA Group

A 7.6% growth in premium earnings for AIA Group can be attributed to its shift in the product mix towards long-term savings and a greater bancassurance contribution in Mainland China.

QBE Insurance

Strong premium rate increase and targeted new business growth, partially offset by deliberate property portfolio exits in North America and Australia, and reduced exposure across other property lines drove QBE Insurance revenue by 10.2%.

MS&AD Insurance Group

MS&AD Insurance Group reported 17.5% growth in revenue due to a 4.2% growth in income from Mitsui Sumitomo Insurance Co and 2% rise in revenue from Mitsui Direct General Insurance due to rise in premium rates.

Biggest losers

T&D Holdings and Sompo Holdings saw their earned premiums decline by 11.4% and 5% respectively, leading to an overall reduction in revenue owing to tightening underwriting standards, particularly in regions prone to natural disasters.

Grandhi concludes: “APAC region continues to grapple with economic uncertainties and evolving regulatory frameworks, insurers will need to maintain agility and a forward-looking approach to capitalize not only on growth opportunities arising out of retirement and health segments, but also on emerging risks from adoption of electric vehicles and cyber-attacks. Firms that can balance the demands of risk management with the pursuit of profitable growth, particularly in emerging markets, will be well-positioned to thrive in the years ahead.

“Both local and global factors are also at play shaping the region’s insurance industry, with climate change presenting significant pricing and policy-writing challenges, and artificial intelligence (AI) offering new business and operational opportunities. Despite these challenges, the industry is optimistic by a market, which still has scope for further penetration.”

*“Premiums earned” refers to the premium collected by an insurance company for the portion of a policy that has expired.