- JPMorgan Chase retains top spot

- European banks continued to post strong gains

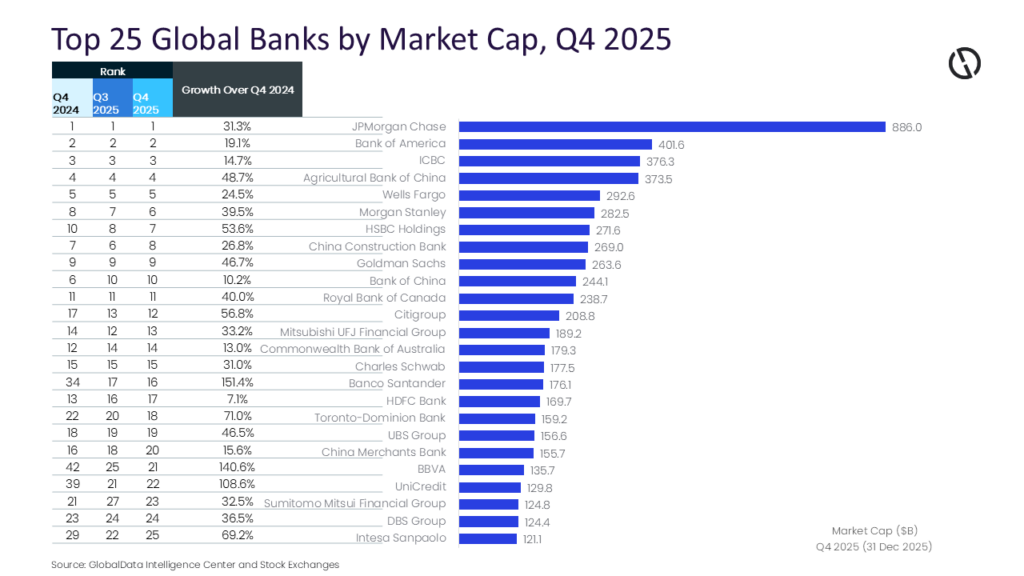

The aggregate market capitalization (MCap) of the top 25 global banks increased by 35.8% year-on-year (YoY), reaching $6.1 trillion in the fourth quarter (Q4) ended 31 December 2025. The gains were broad-based across North America, Europe and parts of Asia, reflecting resilient earnings, higher-for-longer interest rates that continued to support margins in many markets, and improved investor sentiment toward financials, according to GlobalData, a leading intelligence and productivity platform.

Murthy Grandhi, Company Profiles Analyst at GlobalData, comments: “European banking franchises delivered the year’s most striking comeback, led by Spain’s Banco Santander, whose market value surged 151.4% from $70 billion to $176.1 billion, lifting its ranking from 34th to 16th globally. BBVA followed with a 140.6% rise, while Italy’s UniCredit and Intesa Sanpaolo also posted sharp gains, up 108.6% and 69.2%, respectively. These outsized moves signal a decisive shift in investor sentiment toward Europe’s banks after years of restructuring, tighter cost discipline, and stronger net interest margins in a higher-rate environment. Overall, the biggest percentage gainers were concentrated in Europe and Canada, reflecting a rerating from previously discounted valuations, supported by strong deposit franchises and robust capital positions.”

US banks lead the chart

US banks continued to dominate the global rankings in 2025, led by JPMorgan Chase, whose market cap rose 31.3% to $886 billion. Bank of America stayed second, up 19.1% to $401.6 billion, helped by diversified earnings and strong capital-markets activity. Together, the two US giants underscore the sustained dominance of American universal banks.

Investment banking leaders also outperformed as dealmaking recovered in late 2025: Morgan Stanley rose 39.5% to $282.5 billion, and Goldman Sachs climbed 46.7% to $263.6 billion on robust trading, capital markets, and wealth-management growth.

Resilient Chinese banks

Chinese banks remained firmly in the global top tier, supported by huge domestic franchises and gradually improving investor sentiment toward China. ICBC ranked third, with market value up 14.7% to $376.3 billion. Agricultural Bank of China surged 48.7% to $373.5 billion, closing the gap with larger rivals. China Construction Bank and Bank of China also stayed in the top ten list. China Construction Bank rose 26.8% to $269 billion, though it slipped to eighth, while Bank of China gained 10.2% to $244.1 billion and held tenth. Investors drew confidence from policy support and improving asset-quality trends, despite an uneven recovery.

APAC banks

Asia-Pacific banks outside China strengthened their role as regional leaders. Japan’s Mitsubishi UFJ Financial Group’s market capitalization increased by 33.2% to $189.2 billion, and Sumitomo Mitsui Financial Group rose 32.5% to $124.8 billion, both helped by a better rate environment and steady fee income. Singapore’s DBS Group advanced 36.5% to $124.4 billion, reinforcing its position as a leading Southeast Asian franchise. In emerging markets, India’s HDFC Bank grew a more modest 7.1% to $169.7 billion, yet remains among the developing world’s largest banks.

Grandhi concludes: “GlobalData anticipates that global banks head into 2026 with measured optimism, supported by strong capital ratios, improved risk controls, and diversified revenue streams, while digitization and cost discipline continue to bolster their efficiency. The operating backdrop is expected to feature moderating inflation, uneven growth, and gradual rate cuts—an environment that should sustain asset quality and modest lending but likely compress net interest margins from recent peaks. Key risks include geopolitical tensions, weaker trade and policy-driven market volatility, along with China-related uncertainty and ongoing commercial real estate stress, particularly for US regional lenders.”