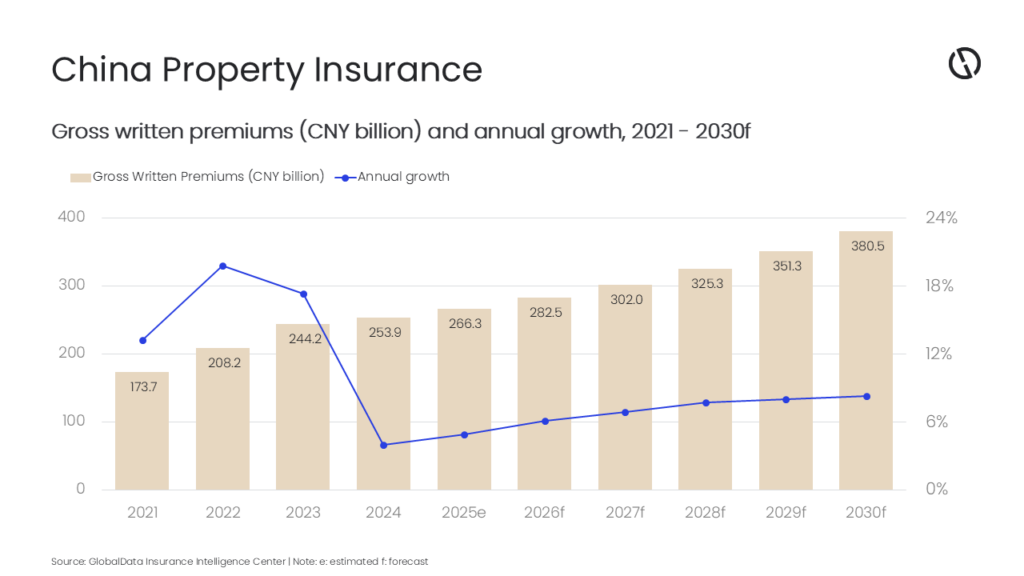

The Chinese property insurance industry is projected to grow at a compound annual growth rate (CAGR) of 7.7%, increasing from CNY282.5 billion ($39.6 billion) in 2026 to CNY380.5 billion ($53.7 billion) by 2030, in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database forecasts that the Chinese property insurance industry is expected to register an annual growth rate of 6.1% in 2026, up from 4.9% growth in 2025. Growth is likely to be sustained by initiatives to narrow the home insurance protection gap, rising disaster-risk solutions (including parametric covers), and continued technology adoption in pricing and claims. Industry actions supporting this trajectory include inclusive home insurance pilots, catastrophe-risk modelling, and the development of catastrophe and disaster insurance solutions addressing both urban and rural exposures. These measures are expected to bolster penetration and improve risk adequacy across property lines.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “The China’s property insurance market growth during 2021–25 reflects firm non-life sector performance and balanced product expansion beyond motor. However, GlobalData projects slower growth during 2026–30 but on a significantly larger premium base as penetration deepens. Regulatory agencies have maintained a stable sector outlook by easing capital pressures and backing disciplined underwriting, which should support sustainable growth and pricing adequacy across property lines.”

The Wang Fuk Court fire in Hong Kong in November last year amplified public awareness of the home insurance protection gap in mainland China and highlighted reliance on estate or contractor policies where household covers are absent. In response, Chinese P&C carriers are introducing customized inclusive home insurance to close protection gaps. However, growth may be constrained by low awareness and underwriting challenges in underpenetrated segments, indicating the need for product redesign and targeted education efforts.

Insurers are investing in advanced catastrophe modelling, sensors, satellite data, and AI to strengthen underwriting and accelerate claims settlement, which are key levers for improving property insurance penetration. Earthquake catastrophe models are intended to improve pricing accuracy and risk prevention. Broader adoption of AI, big data, IoT, and remote sensing is also strengthening urban disaster-risk management and enabling rapid post-event claim settlement, in some cases within minutes.

Sahoo adds: “As China’s weather-risk market expands, regulatory approvals for parametric solutions and weather derivatives are likely to increase capacity and spur innovation in property catastrophe protection. The parametric payouts after Typhoon Matmo and Typhoon Ragasa demonstrate that index-based programs can deliver rapid liquidity and help narrow protection gaps for climate-driven perils.”

Broader innovation in non-life products aligned with national priorities such as green energy, high-tech manufacturing, and disaster coverage will also support the property insurance growth, as insurers tailor solutions to evolving industrial and urban exposures. Infrastructure and power markets are seeing increased capacity and more competitive terms, with China’s power insurance premiums growing on the back of new projects and improved risk management.

Sahoo concludes: “Property insurance premium growth momentum in China is set to pick up over the next five years. Realizing this upside will hinge on closing the home insurance protection gap, embedding catastrophe-risk finance, and maintaining underwriting discipline under a supportive regulatory regime. Technology investments from catastrophe models to AI-enabled claims will help raise resilience and customer confidence during 2026–30.”