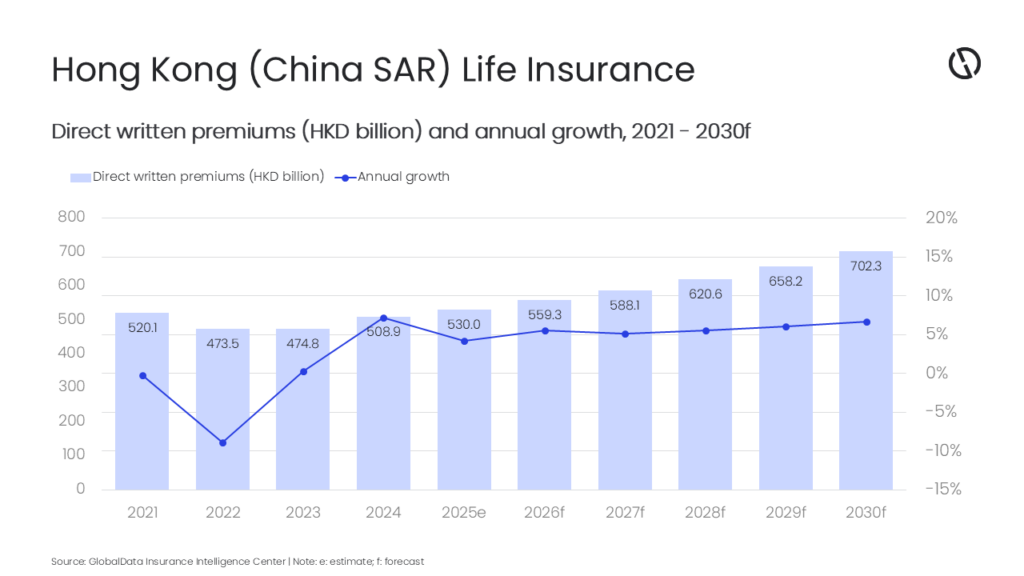

The Hong Kong (China SAR) life insurance market is projected to grow from HKD559.3 billion ($71.6 billion) in 2026 to HKD702.3 billion ($89.9 billion) in 2030, registering a compound annual growth rate (CAGR) of 5.9% in terms of direct written premiums (DWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Global Insurance Database forecasts Hong Kong’s life insurance DWP to register 5.5% growth in 2026. The growth will be fueled by aging demographics, cross-border demand, more sophisticated product offerings, and robust regulatory frameworks.

Manogna Vangari, Insurance Analyst at GlobalData, comments: “Going into 2026 and beyond, Hong Kong’s life insurance industry is well-poised for steady growth. However, success will depend heavily on how insurers navigate rising regulatory costs, manage currency and market risk, and differentiate themselves in a competitive landscape.”

GlobalData forecasts that new business DWP will exceed HKD270 billion ($34.6 billion) in 2026, representing a year-on-year growth of 10.2%, and is expected to grow at a CAGR of 9.1% over 2026–30. Non-linked life insurance business is projected to make up 96.6% of total life DWP in 2026 and to grow at a CAGR of 6% during the same period. Meanwhile, single-premium policies are expected to grow by 5.4% in 2026 and to achieve a CAGR of 10.8% across 2026–30.

In H1 2025, provisional data from Hong Kong’s Insurance Authority (IA) showed a strong rise in long-term new business: linked insurance premiums jumped 60.8% year-on-year to HKD6.9 billion ($883.1 million). Also, about 44,000 qualifying deferred annuity policies were issued, generating HKD2.8 billion ($358.4 million), accounting for approximately 1.6% of total individual new business premiums.

Vangari adds: “Hong Kong’s demographic profile underscores the insurance market’s trajectory. The population is rapidly aging and is projected to reach a ‘super-aged’ society by 2030, with those age 65 and above comprising about 23.6% of the total population, fueling demand for retirement income, annuities, and other long-term protection products.”

Meanwhile, whole life insurance remains the dominant line, estimated at a 55.5% share of life insurance DWP in 2026. It is projected to grow at a CAGR of around 2.6% through 2030.

GlobalData expects endowment insurance, the second-largest line, to represent about 10.6% of life insurance DWP in 2026 and to grow at a CAGR of approximately 6.4% over 2026–30. These endowment products, such as participating policies, indexed universal life (IUL), and wealth legacy solutions, are gaining prominence due to their margin potential and appeal to clients seeking both protection and growth. Insurers are also intensifying efforts to target high-net-worth (HNW) clients, driven by intergenerational wealth transfer.

Vangari continues: “Bancassurance channels are seeing notable growth, encouraged by shifting interest rate expectations. Hong Kong’s Interbank Offered Rate began to decline in May 2025, reducing the attractiveness of time deposits and prompting customer demand toward savings and protection products. These trends, combined with product breadth supported by regulatory clarity (especially around IUL and multi-currency or downside-protected strategies), are expected to underpin sustained inflows from HNW clients.”

Other lines, including general annuities, pensions, term life, and miscellaneous life products—are expected to make up the remainder, around 33.9%.

Vangari concludes: “Hong Kong’s life insurance sector stands to benefit from premium expansion, demographic shifts, and enhanced bancassurance channels, supporting sustained growth in protection, retirement, and HNW solutions through 2026–30. However, risk-based capital reporting and intensified conduct supervision will increase compliance and operational demands but should bolster market integrity and policyholder confidence—supporting sustainable premium growth.”