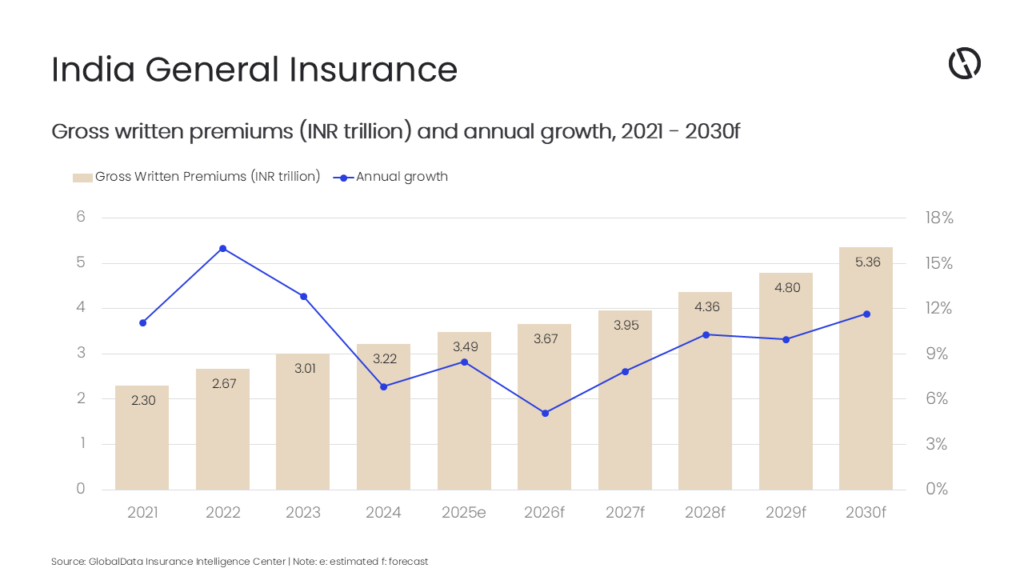

India’s general insurance industry is projected to grow at a robust compound annual growth rate (CAGR) of 10.0%, increasing from INR3.6 trillion ($43.4 billion) in 2026 to INR5.4 trillion ($62.2 billion) by 2030, in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the industry to register 8.5% growth in general insurance premiums in 2025. The growth is expected to moderate to 5.1% in 2026 before accelerating again from 2027 onward. The moderation in 2026 reflects a normalization following the post-GST surge and the impact of accounting changes. Motor and health together accounted for 72.6% of general insurance premiums in 2025, underscoring its role as the sector’s growth engine.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Digitalization of sales and claims processing, GST exemptions on key retail lines, and strong auto and health insurance demand have supported growth during 2021-25. Growth during 2026-30 is expected to be driven by stonger policyholder protection, faster claims settlement, and broader catastrophe-risk coverage. Reforms to strengthen insurance’s role as “invisible infrastructure,” with a focus on inclusion and climate resilience, are expected to bolster market penetration in Tier II and Tier III cities and among micro, small, and medium enterprises.”

The industry’s medium term growth will be supported by strong economic activity and regulatory reforms that streamline product approvals and expand distribution. Structural reforms, including 100% FDI, enhanced powers for the Insurance Regulatory and Development Authority (IRDAI), and composite licensing, are expected to attract capital, deepen product innovation, and strengthen policyholder protection. These measures will be key to closing India’s protection gap as penetration rises from a low base.

Personal Accident & Health (PA&H) accounts for the largest share of general insurance premiums, at 40.9% in 2025, up from 35.7% in 2021. It is expected to grow by 8.8% in 2026. While affordability reforms have spurred uptake in health insurance, service quality and grievance redressal remained in focus during 2021-25. The removal of GST on retail health insurance from September 2025 made protection more affordable, boosting policy uptake; Q4 2025 data showed standalone health insurance premiums up by 13.2% quarter-on-quarter.

Sahoo adds: “New product launches with extensive OPD and wellness coverage signal aggressive product innovation aimed at reducing out-of-pocket costs. However, rising grievances and recent regulatory penalties over claims and governance lapses highlight service gaps and the regulator’s resolve to protect policyholders and enforce standards.”

Motor insurance is the second-largest line of business, accounting for 31.7% of general insurance GWP in 2025. The segment shows a structural shift, with growth in the sale of electric vehicle (EV) insurance reflecting higher vehicle values and technology-rich components.

Sahoo continues: “Usage-based products gained traction, signaling deeper adoption of telematics-led underwriting. Meanwhile, digital brokers are enhancing post-accident support by assigning dedicated claims managers, coordinating with garages and surveyors, and escalating disputes to expedite fair settlements. Such channels are also emphasizing digital documentation to cut paperwork and reduce claim delays.”

At the same time, car insurance premiums face upward pressure as reinsurers reprice catastrophe exposure and repair-cost inflation rises. The strong 2025 auto sales backdrop supports sustained demand for motor coverage.

States have started institutionalizing risk transfer by approving a comprehensive disaster home insurance program that blends parametric (fast, trigger-based payouts) with indemnity cover up to INR1 million for families living below the poverty line to close protection gaps for climate-exposed households and reduce ad-hoc fiscal relief.

Rising public investment in infrastructure will support the growth of property insurance, which accounted for 20.2% of general insurance GWP in 2025. During 2026-27, infrastructure investment is expected to reach $128.6 billion, a major boost for property insurance. In addition, a focus on Tier II and Tier III cities in terms of housing, transport, and urban infrastructure will support the growth of property insurance during 2026-30.

Sahoo concludes: “India’s general insurance industry is expected to grow on the back of strengthening policyholder protection, product innovation in motor and health, the expansion of parametric and disaster pools to manage climate risk, and a step-up in digital claims and distribution.

“Reforms such as tax exemption, GST reliefs, and stronger grievance redressal, paired with robust digital platforms and disciplined natural catastrophe (NatCat) pricing, position the market for sustained premium growth. However, insurers need to remain watchful about the impact of the West Asia crisis, which has already increased risk premiums for marine, aviation, and transit (MAT) business and construction costs in the country, with an expected wider impact on the economy.”