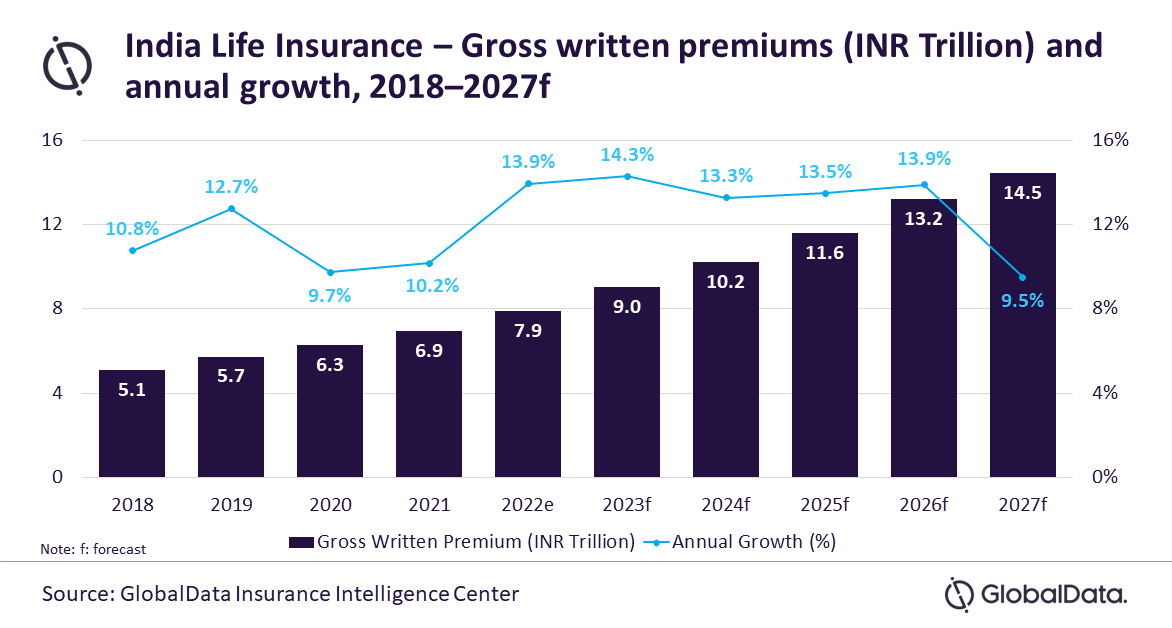

India’s life insurance industry is set to grow at a compound annual growth rate (CAGR) of 12.5% from INR9.0 trillion ($128.0 billion) in 2023 to INR14.5 trillion ($170.6 billion) in 2027, in terms of gross written premiums (GWP), forecasts GlobalData, a leading data and analytics company.

According to GlobalData’s Insurance database, the Indian life insurance industry’s growth is forecasted to peak at 14.3% in 2023. The growth will be supported by the introduction of conducive regulatory policies, increasing insurance awareness, and product innovation aided by the licensing of new insurance companies.

Deblina Mitra, Senior Insurance Analyst at GlobalData, comments: “Continuing on the strength of growing awareness and the adoption of group insurance practices, life insurance GWP is expected to have recorded double-digit growth in 2022. This trend is forecasted to continue till 2026.”

Group insurance GWP grew at a CAGR of 13.3% during 2018–21, outpacing retail insurance’s CAGR of 11.9% during the same period.

The December 2022 regulatory amendments are expected to ease the life insurance operations. The changes allow direct private equity investments in insurance companies instead of mandatory investments via a special purpose vehicle (SPV).

Insurance subsidiaries can now become promoters, giving flexibility in ownership provisions. This will infuse more capital, enabling insurers to expand their operations.

The regulation also lowered the solvency capital margin required on unit-linked (without guarantee) and government-backed life insurance lines, freeing up to INR20.0 billion ($26.38 billion). Insurers can leverage this capital to innovate products and strengthen their distribution.

To ensure insurance for the entire population by 2047, the regulation eased tie-up between corporate agents and marketing firms to tie up with up to six insurers from three insurers earlier. It also extended the regulatory sandbox framework for up to 36 months for both insurers and intermediaries to experiment new products and processes. This will help improve market competition, supporting growth.

The entry of new players – Acko Life (insurtech startup) and Credit Access Life (microinsurer), in April 2023, will also support the growth and increase insurance penetration. More insurers are expected to receive licenses in 2023.

Mitra continues: “Despite these positive developments, the premium growth is expected to be partially impacted by the new tax rules.”

From April 2023, all new non-linked policies with an annual premium of over INR500,000 ($6,764.7) will be subjected to tax applicable on the maturity benefits. With non-linked insurance accounting for 85.4% of life insurance GWP in 2022, this could impact growth over 2023–27.

Mitra concludes: “The entry of new insurers will improve the competitive landscape of the life insurance industry in India and aid in the creation of more inclusive product propositions over the next five years. The growth, however, might be exposed to new taxes.”