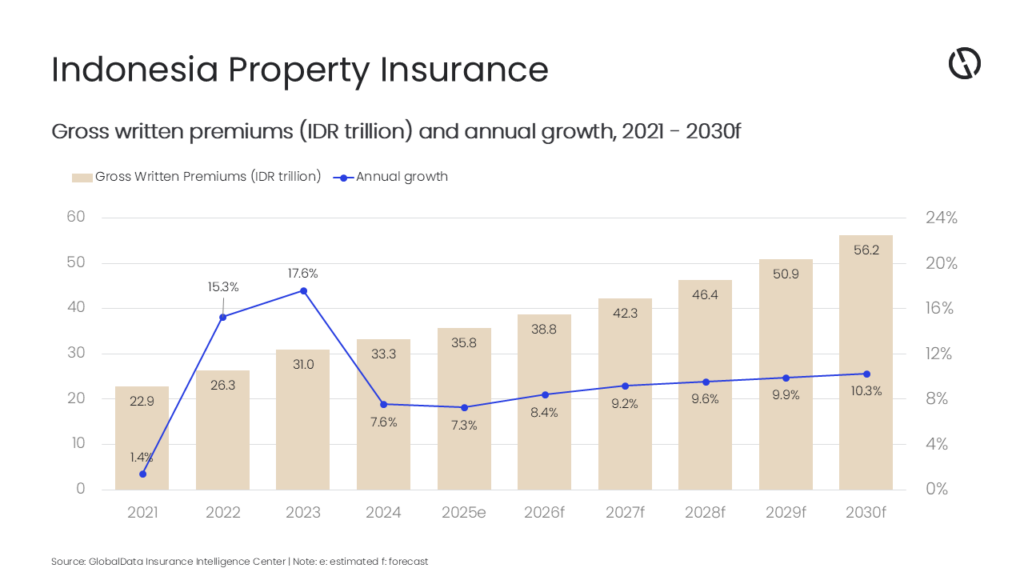

Property insurance in Indonesia is projected to grow at a compound annual growth rate (CAGR) of 9.7%, increasing from IDR38.8 trillion ($2.4 billion) in 2026 to IDR56.2 trillion ($3.5 billion) by 2030, in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the Indonesian property insurance premiums will grow at a rate of 8.4% in 2026, supported by rising risk awareness amid recurring flood and fire events, regulatory-led innovation, and the government’s risk mitigation investments. Catastrophic events in Bali and across Indonesia continue to expose significant uninsured losses, increasing demand for comprehensive property coverage, particularly for flood and fire protection.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Post-flood risk awareness, evolving underwriting strategies, and product enhancements targeting catastrophe perils are expected to support industry growth in 2026. Market momentum is also expected to benefit from parametric frameworks designed to speed up claim payments (7–14 days) and expand risk transfer capacity for public assets, potentially catalyzing broader take-up among private insureds.”

Indonesia is expected to introduce a new parametric scheme for public assets in 2026, co-developed with insurers and reinsurers. The scheme is designed to deliver transparent, trigger-based payouts and enhance liquidity following earthquakes or floods, with the potential to expand to private property solutions over time.

The protection gap remains a defining structural driver. Less than 0.1% of Indonesian homes are covered by disaster insurance, and GlobalData’s Global Insurance Database shows property insurance penetration in Indonesia at 0.13% in 2026. With more than 80% of losses from major floods uninsured, there is substantial headroom for growth as distribution, affordability, and product relevance improve.

Severe flooding in Bali in December 2025 damaged hundreds of assets and triggered a week-long emergency. Such climate-driven losses typically translate into higher claims and, over time, increased demand for comprehensive flood coverage across home and commercial property segments. Insurers have reported rising property claims linked to floods, reinforcing these trends.

Sahoo adds: “Physical risk mitigation will also shape underwriting and demand. Government-led flood defenses—from river normalization and emergency repairs in Bali to coastal barriers in North Jakarta—aim to reduce future losses. While these projects can moderate claim frequency, residual risk from extreme events still necessitates robust flood and fire coverage.”

Capacity and pricing conditions remain mixed. Property rates softened in Q3 2025 due to improved reinsurance capacity, supporting near-term affordability and coverage expansion. However, rising natural catastrophe claims are expected to influence reinsurance renewals, with higher pricing, increased retentions, and tighter capacity potentially lifting property rates and strengthening underwriting discipline over the medium term.

Man-made catastrophe risk is increasing the need for policy wordings that include riot, strike, and civil commotion. Large-scale fires and unrest affecting public buildings in Makassar (August 2025) and Surabaya (December 2025) exposed potential coverage gaps where protection is absent or limited. This is likely to increase demand for enhanced endorsements in commercial property programs and may contribute to higher pricing in high-risk locations.

Sahoo concludes: “Indonesia’s property insurance market is entering a pivotal growth phase. Persistent flood and fire losses have increased protection gaps, and regulatory-led innovation are reshaping demand, pricing, and capacity in favor of broader property coverage. With emergency mitigation investments and rising risk literacy, Indonesia’s property line is positioned for sustained premium growth and deeper market relevance through 2030.”