In an environment defined by continuous volatility and interconnected risks, traditional underwriting models are increasingly misaligned with how risk behaves. As climate, geopolitical, technological, and social disruptions accelerate, underwriting must evolve from static, point-in-time decisions to liquid underwriting, a continuous, signal-driven approach designed to interpret risk dynamically across the policy lifecycle, says GlobalData, a leading intelligence and productivity platform.

Celent, a GlobalData company, addresses this challenge in its latest report, Liquid Underwriting: Transforming Underwriting into a Living System. Building on the concept of liquid risk introduced in the earlier report Navigating Liquid Risk: Rethinking Insurance for a World of Disruption, the new study reframes underwriting as a living system capable of interpreting risk continuously, responding to events in real time, and operating coherently within systemic uncertainty.

Fábio Sarrico, Senior Insurance Analyst at Celent and author of the report, says: “Risk no longer behaves like isolated events. It behaves like a system. If underwriting continues to assume stability in a world defined by fluidity, insurers will see volatility not only in loss ratios, but in strategic control, capital efficiency, and trust. liquid underwriting is the operational response to that reality.”

What is liquid underwriting?

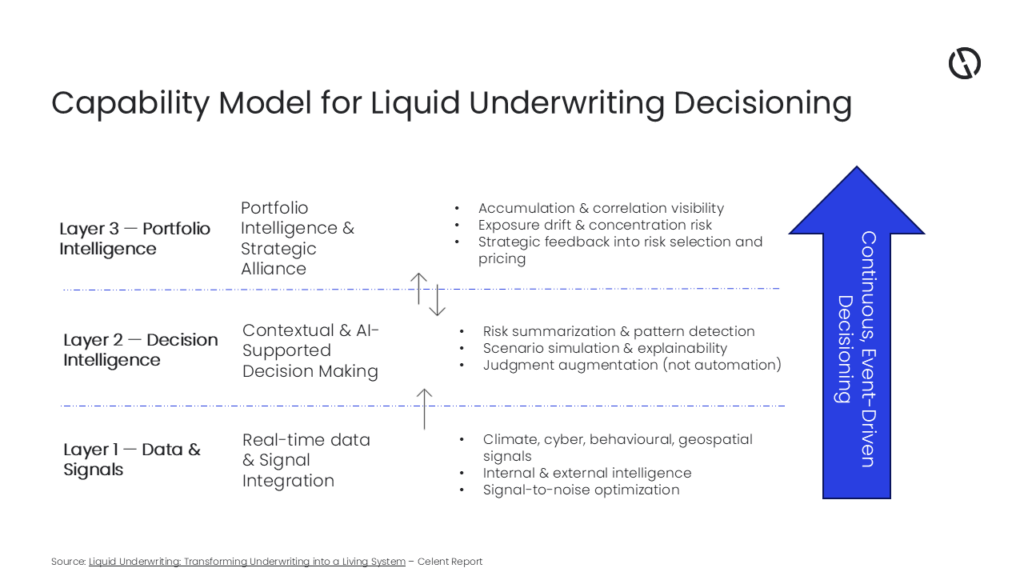

Liquid underwriting is a continuous, context-aware underwriting model that integrates real-time signals, risk interpretation, and portfolio awareness to support adaptive decision-making as conditions evolve. Where traditional underwriting assumes stability, liquid underwriting assumes motion. Where traditional models extrapolate from history, liquid underwriting listens to signals.

Rather than concentrating decisions at fixed moments such as submission or renewal, liquid underwriting treats underwriting as an ongoing discipline that unfolds across the policy lifecycle.

Why it matters now?

The limitations of static underwriting are already visible. Climate risks evolve faster than annual cycles can capture. Geopolitical events reshape exposure in hours rather than quarters. Technological and social dynamics introduce second- and third-order effects that evade traditional actuarial models.

Sarrico explains: “Insurers are not facing a data shortage. They are facing a decision-coherence problem. Signals are everywhere, but underwriting systems were never designed to interpret them continuously or at portfolio level.”

The report highlights that addressing this gap requires more than incremental automation. It requires a structural shift in how underwriting decisions are made, supported, and governed.

A framework for underwriting as a living system

The liquid underwriting report provides insurers with a clear framework to operationalize this shift, including:

- A precise definition of liquid underwriting as a continuous decisioning discipline

- Core capabilities required for contextual, event-responsive underwriting

- The evolving role of underwriters as interpreters of uncertainty, augmented—not replaced—by AI

- Architectural implications, including decoupled, event-driven, API-first foundations

- Strategic implications for product design, portfolio steering, resilience, and trust

Sarrico concludes: “Liquid underwriting is not an end state. It is an operating posture. The future of underwriting will not belong to those who try to eliminate complexity, but to those who can interpret it—continuously, coherently, and at scale.”