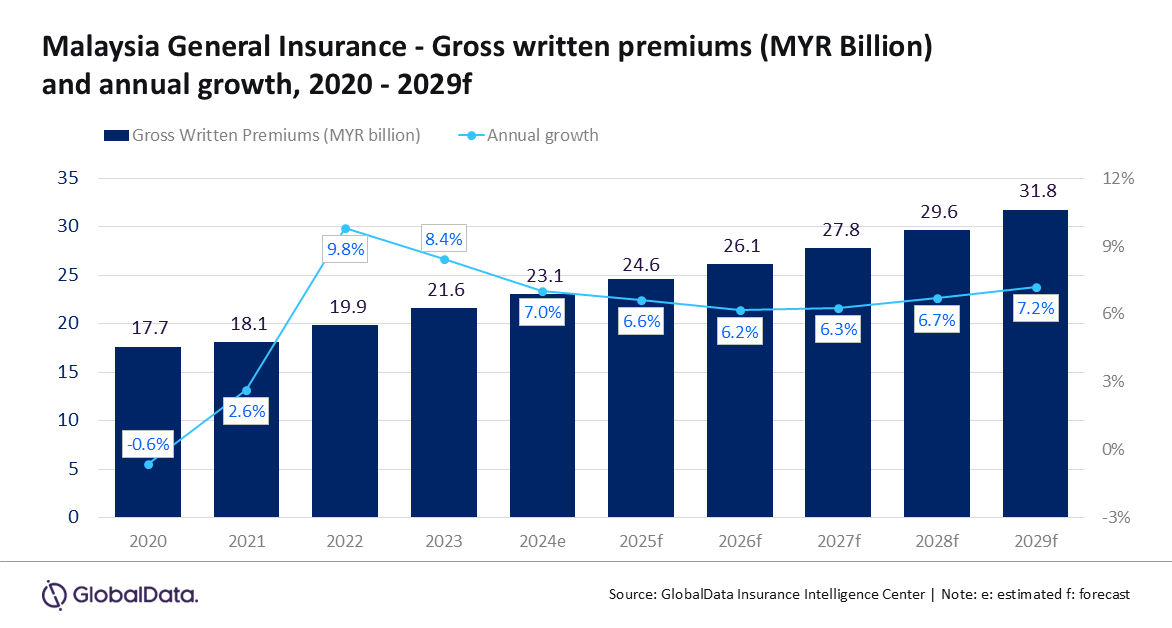

The general insurance industry in Malaysia is projected to grow at a compound annual growth rate (CAGR) of 6.6% from MYR24.6 billion ($5.5 billion) in 2025 to MYR31.8 billion ($7.2 billion) by 2029, in terms of gross written premium (GWP), according to GlobalData, a leading data and analytics company.

GlobalData’s Insurance Database estimates the Malaysian general insurance industry to reach MYR24.6 billion ($5.5 billion) in 2025, reflecting an annual growth rate of 6.6%. This growth is attributed to increased premium rates across lines, strong demand for natural catastrophe insurance, economic recovery, rising vehicle sales, and escalating healthcare costs. Motor, property, and personal accident and health (PA&H) insurance lines contributed 82.6% of the general insurance GWP in 2024.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Regulatory initiatives to develop the insurance market and increase insurance penetration will drive the growth of the general insurance industry in Malaysia. Additionally, the rising traffic accident rate and increasing frequency of natural disasters will support higher policy uptake and premium growth in the industry.”

The Bank Negara Malaysia’s (BNM) Financial Inclusion Framework 2023–2026 set an objective to increase insurance/takaful penetration to around 5% by 2026. In 2024, the penetration rate stood at 4.4%. The framework includes strategic measures such as scaling up microinsurance and microtakaful products by making such products widely available and promoting digital insurance to make insurance affordable.

In December 2024, BNM capped the annual health insurance premium hike at 10% per year for the next three years, considering the latest surge in health premiums, even to the extent of a more than 50% hike by a few insurers. Also, the introduction of the new Risk-Based Capital 2 (RBC2) framework starting in Jan 2027 will strengthen the insurance industry. Such initiatives will boost customer confidence and support growth.

Motor insurance is the largest line of business and is expected to account for 44.7% of the general insurance GWP in 2025. The rising vehicle sales and road accidents will support the growth of motor insurance. According to the Ministry of Transport, on average, 1.3 million people die in road accidents each year. Also, the rising demand to cover natural disaster-related damages to vehicles will support the growth of motor insurance in 2025.

According to the Malaysian Automotive Association (MAA), the total vehicle sales increased by 2.1% year-on-year to reach 816,747 units in 2024. Despite the uncertainties on the impact of the US-China trade war, MAA expects the automotive sector to register growth in 2025, driven by an increase in electric vehicle (EV) sales. In 2024, the registration of EVs increased by 64%, and EVs accounted for 2.54% of the total vehicles registered in Malaysia.

Property insurance is the second-largest line of business with an estimated 26.2% share of the general insurance GWP in 2025. After registering a growth of 4.6% in 2024, property insurance is expected to register a growth of 5.8% in 2025, driven by the robust expansion of the construction sector and the frequent occurrence of extreme weather events, especially floods. An increase in torrential rains across various states in Malaysia has spurred demand for fire insurance with flood coverage.

PA&H insurance is the third-largest line of business, estimated to account for 11.4% of the general insurance GWP in 2025. The growth of PA&H insurance will be supported by a surge in health insurance premium rates driven by high medical inflation, which reached 15% in 2024.

Sahoo adds: “High healthcare costs heightened health consciousness among consumers, supporting the demand for health insurance policies. Premium rates will continue to increase in the presence of the aging society, rising non-communicable diseases, and a strained public healthcare system. PA&H insurance is forecasted to grow at a CAGR of 7.6% during 2025-29.”

Other general insurance lines, such as financial lines, liability, and marine, aviation, and transit, are estimated to account for the remaining 17.7% share of the general insurance GWP in 2025.

Sahoo concludes: “The growth of Malaysia’s general insurance market remains positive. Rising consumer awareness, regulatory developments, and the increasing frequency of natural disasters will play a pivotal role in shaping the industry’s trajectory over the next few years. However, the expected new reciprocal tariffs from the US will create uncertainties and change the dynamics.”