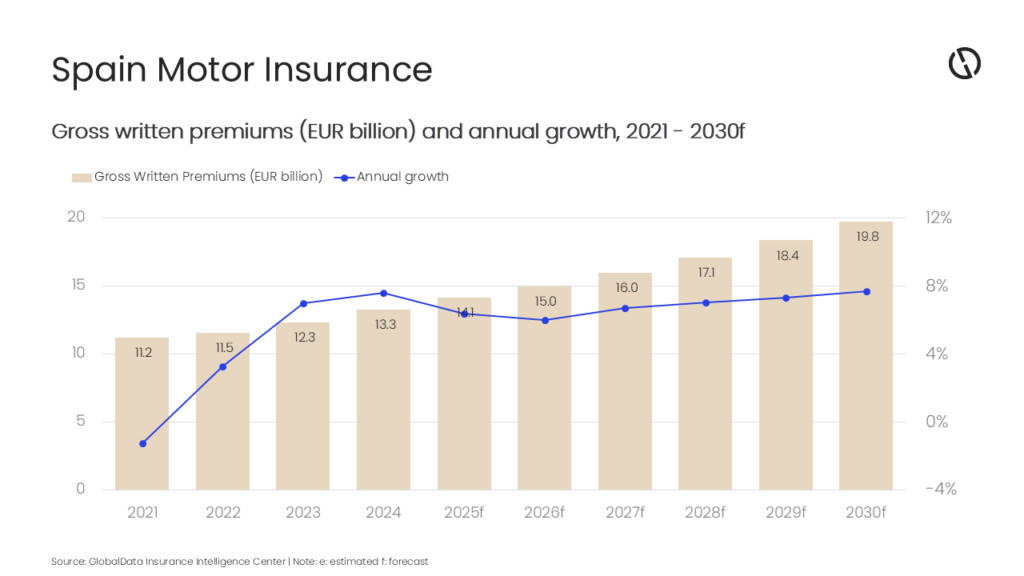

The motor insurance industry in Spain is projected to grow at a compound annual growth rate (CAGR) of 7.2%, increasing from €15.0 billion ($17.4 billion) in 2026 to €19.8 billion ($21.6 billion) by 2030, in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the Spanish motor insurance industry will register an annual growth rate of 6.0% in 2026, supported by expanding digital distribution, wider adoption of telematics-powered pricing, and new micro‑mobility mandates to increase premium volume. Broader European adoption of usage-based insurance (UBI) and AI-enabled underwriting is reshaping pricing and claims efficiency, underpinning multi‑year premium growth for auto insurers.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “The industry is expected to ease slightly from 6.4% to 6.0% in 2026 as pricing normalizes from recent highs, while remaining supported by regulatory-driven new business from light personal vehicles (LPVs). Pricing conditions have softened in parts of Europe, but Southern Europe shows resilience and moderate growth, supported by rising repair costs. This is expected to keep the Spanish motor expansion on a growth track in 2026.”

Growth in the motor insurance industry will continue to be supported by mandatory third‑party liability coverage, rising vehicle ownership, and a shift toward comprehensive and usage‑based policies, as repair costs increase with advanced technologies. Regulatory changes requiring liability coverage for e‑scooters and other LPVs starting January 2026 will expand Spain’s insured base and spur product launches, further supporting momentum and growth.

Motor hull and third-party liability products held an almost equal share of the motor insurance premiums – 49.6% and 50.4%, respectively, in 2025. The growth of both motor hull and third-party liability lines will be supported by regulatory changes. The mandatory liability insurance for e‑scooters and high‑powered e‑bikes will create fresh premium pools and broaden protection.

Distribution and competition are also intensifying in the Spanish motor insurance industry. Investments in AI‑powered claims handling and embedded insurance partnerships with automakers and mobility platforms are reshaping product design and distribution. Insurtech and incumbents are broadening direct-to-consumer (D2C) channels to capture price‑sensitive and digital‑first customers. The launch of the direct online auto channel in 2025 targeted faster binding and transparent pricing.

In addition, products such as fully digital auto for expatriates will streamline contracting and claims processing in multiple languages, a move that taps a known protection gap. Meanwhile, online channels are scaling rapidly as consumers shift purchasing and servicing to digital channels, boosting self‑service adoption and embedded insurance uptake across the auto segment.

Sahoo adds: “Profitability pressures persist in the Spanish motor insurance industry. The loss ratio remained high above 80% in recent years, increasing from 80.6% in 2023 to 81.3% in 2024 and 81.4% in 2025. This signals underwriting strain and the need for continued pricing and efficiency actions. Despite the increase, the loss ratio is partially offset by telematics, which strengthens risk differentiation and fraud reduction through granular driving data and real‑time incident insights.”

Heightened climate‑related losses also weigh on reinsurance capacity and risk costs, keeping insurers focused on disciplined underwriting, product enhancements, and claims automation to protect margins. The Valencia floods in October 2024 destroyed around 130,000 vehicles and resulted in around €1.2 billion in claims in Spain, according to El Consorcio de Compensación de Seguros. At the same time, connected-car and data privacy regulations, such as the GDPR, continue to shape how telematics data can be used in pricing and claims, requiring robust governance and secure, transparent operations.

Sahoo concludes: ” The Spanish motor insurance market is expected to sustain growth momentum in the next five years, supported by mandated LPV insurance from 2026, deepening UBI penetration, and continued digitalization across distribution, pricing, and claims. Insurers that scale telematics, optimize D2C capabilities, and industrialize AI‑driven underwriting and fraud controls are best positioned to capture above‑market growth and improve underwriting performance in the evolving motor insurance landscape.”