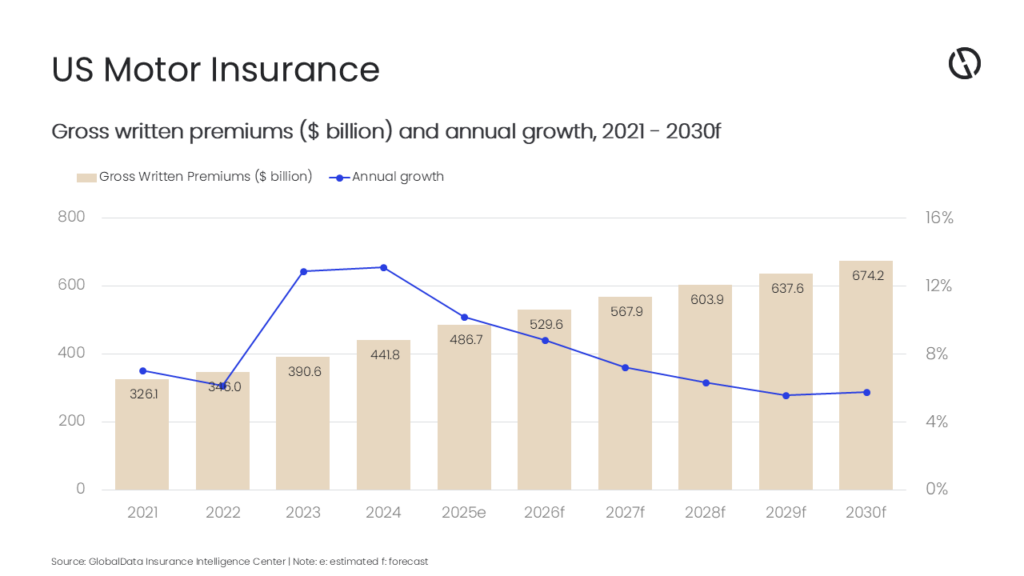

The US motor insurance industry is projected to grow at a compound annual growth rate (CAGR) of 6.2%, increasing from $529.6 billion in 2026 to $674.2 billion by 2030, in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the US motor insurance industry will register an annual growth rate of 8.8% in 2026, supported by increased minimum liability requirements, climate-driven claims inflation, and technology-led product innovation. Regulatory hikes to statutory auto limits in major states such as California, Massachusetts, and North Carolina in 2025 are raising required coverage and pushing up premiums, while telematics, embedded distribution, and OEM-branded agencies broaden access and personalization for consumers.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Motor insurance growth in the US is expected to be supported by the elevated pricing, which remains high compared to the pre-pandemic patterns. Cost inflation in vehicle parts and labor further support the growth of commercial auto insurance.”

New‑vehicle prices continue to climb, as average transaction prices for 2026 models rose 2.6% year-over-year to $49,077, according to Kelley Blue Book, This will drive policies with higher insured values, especially for technology‑heavy electric vehicles (EVs) that carry higher repair costs.

Tariff policy is another factor driving the growth of motor insurance, as ongoing tariffs on vehicles and parts will push auto premiums higher in 2026. The US imports most of its motor vehicles and parts from Mexico, Canada, China, Japan, and South Korea.

Climate and catastrophe trends are reshaping motor claims and pricing in the US. Average full‑coverage auto premiums are projected to rise in 2026, led by tariffs and climate‑driven repair costs. Catastrophic events such as the Los Angeles County wildfires in January 2025 destroying thousands of vehicles, and hurricanes in Florida in 2024, which generated over 100,000 auto claims, will elevate comprehensive claim frequency and severity, sustaining upward pressure on premium rates.

Sahoo adds: “Protection gaps were exposed during the Wisconsin flood in August 2025, where most vehicles lacked flood coverage. Although auto flood losses are covered under comprehensive policies, liability‑only drivers faced out‑of‑pocket costs. This is expected to increase the demand for protection against flood, hail, and wildfire losses, which will reinforce coverage uptake in hazard‑prone regions.”

Technology and innovations in distribution are expanding the market and sharpening product pricing. Usage‑based insurance and telematics continue to scale through insurer programs and new data sources. Such innovations support more precise territorial ratemaking as there is ZIP code-based tracking and faster risk adjustments, while the broader telematics market is integrating AI and cloud analytics to improve claims and fraud detection. Also, end‑to‑end digital claims experiences drive higher satisfaction and retention, even as gaps in proactive updates still force customers to switch channels.

Insurers are leveraging AI and telematics to accelerate underwriting and claims, while auto manufacturers such as Volvo and Honda launched multi‑carrier insurance agencies in more than 18 states to embed and bundle auto with home and umbrella coverage. This move will broaden access, support bundling discounts, and add premium volume through new channels.

Sahoo concludes: “The US motor insurance market is on the growth track. Increasing risk factors, tariff‑driven cost inflation, and technology‑enabled pricing and distribution should keep premiums on a multi‑year growth path. Carriers that advance telematics‑driven underwriting and digital claims, manage climate‑exposed comprehensive risk, and navigate state‑by‑state regulatory change are best positioned to sustain growth and retention.”