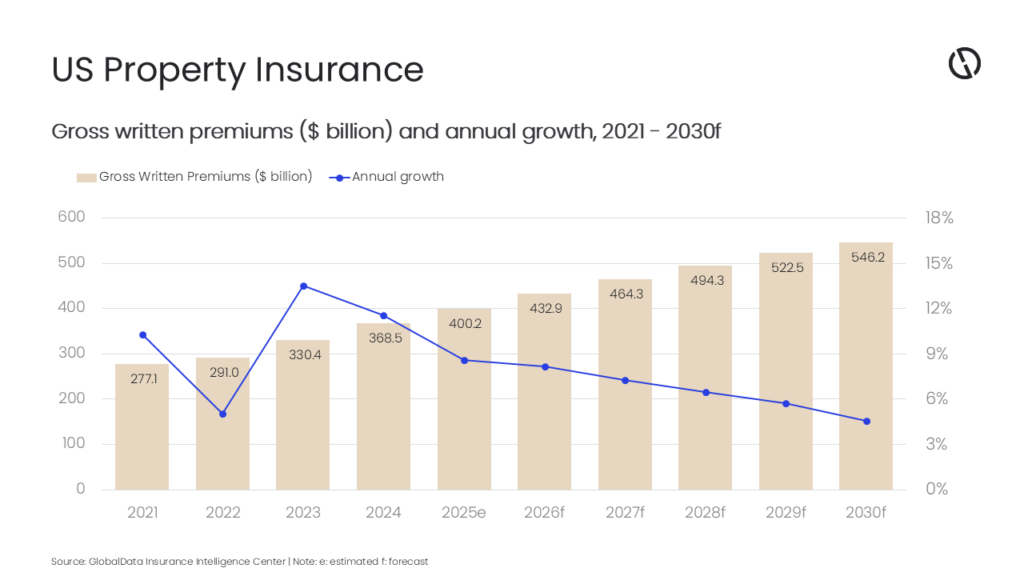

The US property insurance industry is forecast to grow at a compound annual growth rate (CAGR) of 6.0%, with gross written premiums (GWPs) increasing from $432.9 billion in 2026 to $546.2 billion by 2030, according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the US property insurance industry will register an annual growth of 8.2% in 2026, as carriers navigate persistent natural hazard exposures, evolving regulations, and the expansion of specialty and flood solutions. Growth is also expected to be supported by elevated loss costs and repricing amid recurring climate-driven catastrophes and higher reconstruction costs. Elevated catastrophe losses have become structural, with 2025 marking a sixth straight year above $100 billion of insured global catastrophe losses, as per Swiss Re.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Premium dynamics will continue to reflect the frequent occurrence of severe weather events, an upward trend in materials and labor costs, increasing reinsurance cost and consideration of mitigation measures in the risk models. While premium growth in 2025–26 is expected to moderate from prior peaks, pricing remains upwardly biased given record wildfire losses, persistent severe convective storms, and inflation in labor and materials.”

Home insurance rates are likely to continue to increase as carriers reprice for inflation and catastrophe risk. Out of the total global natural catastrophe losses, the US accounted for most of the insured losses, led by record wildfire claims and severe convective storms. These back-to-back, high-severity seasons reinforce carriers’ need for stronger capital, reinsurance, and pricing, elevating homeowners’ premiums, especially in fire- and storm‑exposed states.

Sahoo adds: “Homeowners’ insurance was the main driver, with a 49.3% share in property insurance GWP in 2025. Following years of extreme losses and rapid price escalation, 2026 is likely to offer a period of relative stabilization in homeowners’ insurance, although costs and risk exposure will likely stay elevated. The line of business remains challenged by premium affordability.”

According to the Federal Reserve Bank of Dallas, insurance now consumes about 14% of homeowners’ monthly payments in 2025, which includes mortgage principal and interest. High-risk markets such as Florida and California face insurer withdrawals, non‑renewals, and reliance on residual market plans, dynamics that continue to widen protection gaps. States are responding with policy and regulatory recalibration to stabilize access and capacity.

Sahoo continues: “Reinsurance and alternative capital are buttressing property capacity. Farmers Insurance secured $400 million of indemnity-based catastrophe bond protection, part of a broader surge in insurance-linked securities (ILS) and catastrophe bonds, including record issuance of wildfire catastrophe bonds in 2025. These structures diversify carriers’ risk and can temper rating pressure at renewals. These placements are increasingly strategic in a world of frequent, severe secondary perils.”

Digital modernization is raising expectations in claims and underwriting. Customer satisfaction is highest when claims are managed end‑to‑end via digital channels; however, channel switching remains prevalent due to a lack of proactive communication on claims processing.

Insurers are deploying AI-enabled inspections and virtual assessments to pre-empt non-catastrophe losses and improve claims accuracy. At the portfolio level, advanced AI weather forecasting and geospatial analytics are enhancing catastrophe modelling, enabling more precise pricing and capital allocation amid a higher-volatility peril mix.

Specialty property exposures are also reshaping growth opportunities. The data center buildout tied to AI has driven brokers to expand purpose-built facilities with large limits and integrated coverages for construction, delay in start-up, and business interruption.

Sahoo concludes: “US property insurance will continue to expand during 2026–30, as the market advances from crisis repricing to disciplined, mitigation-informed growth. Private flood expansion, alternative capital, and digital/AI risk tools are widening protection options, while state and national initiatives will stabilize access and align rate adequacy with resilience. Insurers that blend rigorous underwriting with proactive mitigation and customer-centered digital claims will be best positioned to capture durable premium growth through 2030.”