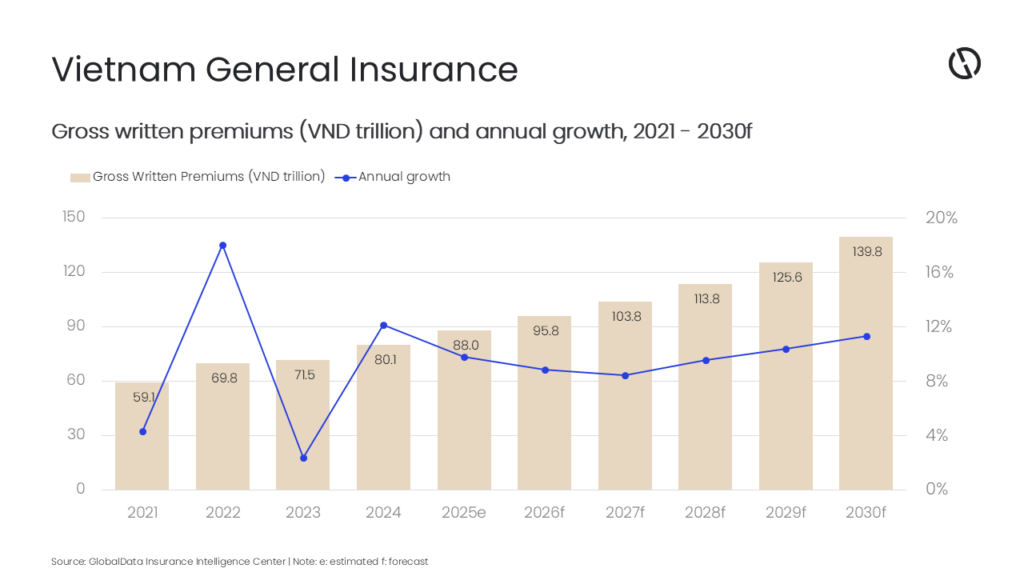

Vietnam’s general insurance industry is forecast to grow at a compound annual growth rate (CAGR) of 9.9%, increasing from VND95.8 trillion ($3.7 billion) in 2026 to VND139.8 trillion ($5.2 billion) by 2030, in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData’s Insurance Database estimates that the Vietnamese general insurance industry will register an annual growth rate of 8.8% in 2026, supported by regulatory tailwinds, rising digital distribution, and heightened awareness of catastrophe risk. New mandates, including compulsory fire insurance for high-rise and large residential complexes, the growth of e-insurance and embedded models, and banks’ deeper push into insurance, are expected to underpin demand across property, health, and motor lines over the next five years. Intensifying climate events will also strengthen the case for coverage.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Structural reforms will support the growth of general insurance in Vietnam. The Ministry of Finance’s adoption of risk-based capital from 2028 will strengthen solvency and market confidence. Also, the proposed amendments to the insurance law aim to streamline licensing, ongoing international investment, and mergers and acquisitions (M&A) activities in the industry.”

Personal Accident & Health (PA&H) accounts for the largest share of general insurance premiums at 37.5% in 2025 and is expected to grow at a CAGR of 12.6% during 2026-2030. This growth is supported by rising medical costs and regulatory improvements in claims and fraud controls. According to the National Statistics Office (NSO), the Consumer Price Index (CPI) in Vietnam increased by an average of 3.31% in 2025. The prices of medicines and health services surged 13.07%, adding 0.61 percentage points to the CPI.

Property insurance is the second-largest line of business, occupying a 25% share of general insurance GWP in 2025. Increased demand for comprehensive catastrophe coverage following severe typhoons and fires is expected to support property insurance growth at a CAGR of 7.5% during 2026–2030.

Sahoo adds: “Policy catalysts are translating into premium inflows. From July 1, 2025, Vietnam mandated fire insurance for all apartments of five floors or more (or over 1,000 square meters). Insurers have responded with tailored, all-risk apartment products featuring digital purchase and claims capabilities to boost compliance and uptake. This addresses a long-standing protection gap in urban property risks and is expected to lift property insurance premiums and improve claims outcomes in future events.’

Motor insurance is the third-largest line of business, with a share of 22.8% of general insurance GWP in 2025. Motor insurance is expected to grow at a CAGR of 8.1% during 2026–2030, supported by rising vehicle sales and product innovation, including electric vehicle (EV) battery coverage.

Sahoo continues: “Inspections identified low payout ratios and delayed settlements in motorbike liability insurance at some carriers, leading to fines and increased oversight. A proposal has emerged to abolish mandatory motorbike insurance. If adopted, it could reshape motor product design and distribution strategies. In light of these developments, restoring customer confidence through timely claims and transparent product terms will be critical to sustaining motor insurance growth during 2026–2030.”

Natural catastrophe (NatCat) exposure continues to shape pricing, coverage design, and reinsurance demand. Following typhoons Ragasa, Bualoi, and Matmo, insurers processed over 1,000 property and engineering claims with estimated losses of $63.7 million, alongside 2,650 motor claims cases, according to the consolidated report submitted by insurers to the Insurance Supervisory Authority in October 2025, revealing capacity pressures in non-life.

Innovation in climate resilience is gaining traction. Weather index (parametric) products—such as Igloo’s satellite-triggered flood coverage in Vietnam—enable faster payouts. Public-private partnerships and the Building Resilience Index aim to align underwriting with resilient construction and incentivize risk-mitigating investments through pricing and product design.

Furthermore, banks are deepening their insurance ecosystems, strengthening distribution and product innovation. Asia Commercial Bank (ACB) is seeking shareholder approval to establish a new non-life subsidiary. Broader bank expansion into insurance is expected to widen access, integrate protection into everyday financial journeys, and unlock new premium streams across insurance lines.

Sahoo concludes: “Vietnam’s general insurance growth is underpinned by regulatory developments, digital channels, and rising risk awareness across property, health, and motor insurance. The strong 10.4% CAGR during 2021–25 provides a strong base, while the expected CAGR in 2026–30 reflects a maturing, technology-enabled marketplace that aligns underwriting discipline and product innovation to close persistent protection gaps.”