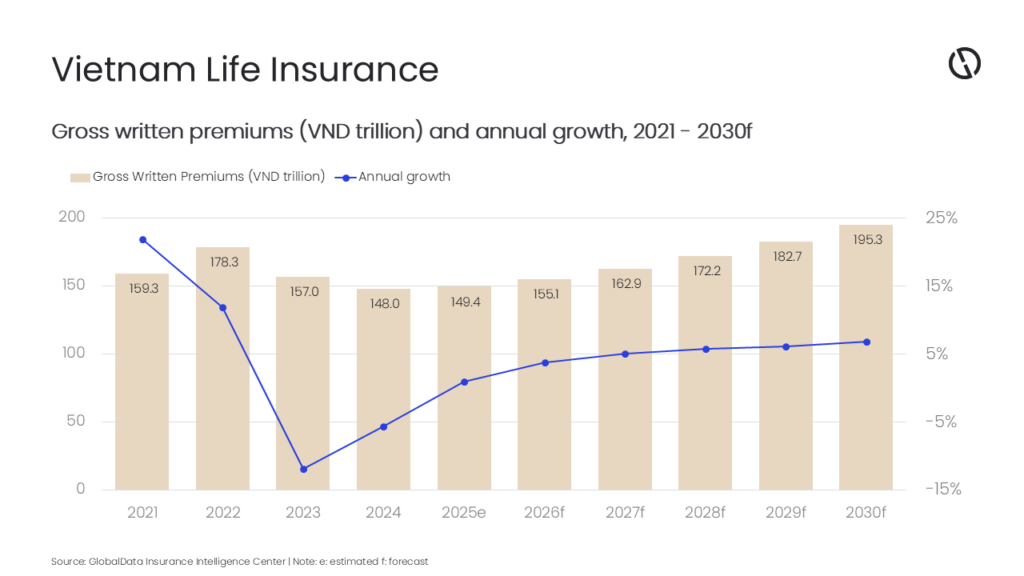

The Vietnamese life insurance industry is projected to grow at a compound annual growth rate (CAGR) of 5.9%, increasing from VND155.1 trillion ($6.0 billion) in 2026 to VND195.3 trillion ($7.2 billion) by 2030 in terms of gross written premium (GWP), according to GlobalData, a leading intelligence and productivity platform.

GlobalData expects the industry’s growth to accelerate to 3.8% in 2026 as the market stabilized in 2025 with an estimated 0.9% annual growth after two years of contraction, as distribution adapts, digital journeys deepen, and banks re-engage on improved terms. The broader insurance market is projected to expand in 2026, signaling a return to healthier premium dynamics that will also support the life insurance recovery.

Digital distribution shifts set the tone for recovery. Starting in 2026, growth is expected to be supported by Vietnam’s pro-digital regulatory agenda, the accelerating shift from bancassurance to e-insurance, and insurers’ pivot toward health and protection products. Regulators and market participants are refocusing on transparent, technology-led sales, with e-insurance rapidly overtaking bancassurance due to widespread smartphone adoption and clearer digital compliance standards.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “Embedded insurance and AI-enabled service, starting from automated claims processing to personalized coverage recommendations, are improving customer experience and trust. Platforms are scaling hybrid digital-agent models to bring term life and comprehensive health products online, while bolstering claims and service capabilities. These initiatives are poised to lift life insurance uptake in the medium term as consumers migrate to simpler and more transparent purchase paths.”

Policy reform and social protection initiatives provide structural tailwinds. Vietnam’s Insurance Supervisory Authority has mapped a 2026–30 sector agenda emphasizing market efficiency, consumer protection, and coverage expansion. Concurrently, the government is advancing social insurance and wage reforms, including a 7.2% regional minimum wage increase from January 2026, which supports income security.

Sahoo adds: “The life insurance market is expected to enter a period of higher-quality and more robust development, aligning with the Government’s objective of achieving life insurance coverage for 18% of Vietnam’s population by 2030. In support of this, insurance companies are undertaking transformation efforts that signal a market recovery characterized by improved quality and sustainability.”

Product strategy is shifting toward protection and health benefits as the market rebuilds. After a difficult period, life insurers are prioritizing comprehensive protection propositions, responding to demographic change and heightened consumer focus on health. Insurers are partnering with technology companies to accelerate digital health and wellness ecosystems, while product innovation from unit-linked solutions with legacy features to universal life and critical illness riders broadens value propositions. The recent surge in flu cases across Asia has reinforced the need for preventive and senior-focused benefits, sharpening demand for well-structured health-linked protection and potentially supporting premium growth within life and health lines.

Sahoo continues: “Banks are deepening their presence in insurance, expanding distribution capacity, and increasing competitive intensity. By establishing or acquiring insurance subsidiaries, banks are integrating protection within financial ecosystems. As insurers adapt their distribution models and banks recalibrate their participation, the sector has returned to growth, aided by diversified channels, better-aligned incentives, and enhanced product suites. This evolution will support increased premium flows in life insurance while narrowing protection gaps via wider access and cross-segment collaboration.”

Insurtech momentum is also building in Vietnam. By deploying AI to streamline underwriting and claims, Insurtechs are positioned to capture demand migrating from bank channels to independent, digitally enabled options. This also aligns with regulatory expectations for transparent advice and should contribute to a more resilient, customer-centric life market over 2026–30.

Health financing reforms are likely to bolster demand for protection within life insurance. Vietnam is moving to launch supplementary health insurance alongside the universal mandatory scheme to reduce high out-of-pocket burdens. Health-linked riders and protection policies within life portfolios are expected to help reinforce premium growth and improve financial resilience for vulnerable groups.

Sahoo concludes: “Vietnam’s life insurance market will be supported by a pro-growth regulatory agenda, digital-first distribution, and a decisive pivot toward health and protection offerings. With banks deepening their role, Insurtechs scaling next-generation platforms, and the state expanding social protection and health financing, the life market is positioned to reduce protection gaps and deliver sustained premium growth through 2030.”