Bispecific (bs) antibody drug conjugates (ADCs) are an emerging therapeutic approach that presents advantages over traditional ADCs. With 84% of bsADCs in the preclinical or discovery stages, the pipeline is still nascent. However, with four candidates in Phase III, the race for the first approval in this novel landscape is underway, according to GlobalData, a leading data and analytics company.

ADCs are a key therapeutic modality in targeted cancer treatment, which combine the precision of monoclonal antibodies with the potency of cytotoxic drugs. With 21 global approvals, ADCs generated $13.6 billion in 2024, according to GlobalData. BsADCs represent further opportunities in this field, by leveraging bispecific antibodies that simultaneously bind two distinct targets. With the ability to target multiple antigens, these bispecific constructs present opportunities to enhance the therapeutic ability of the ADCs by increasing selectivity and reducing off-target toxicity.

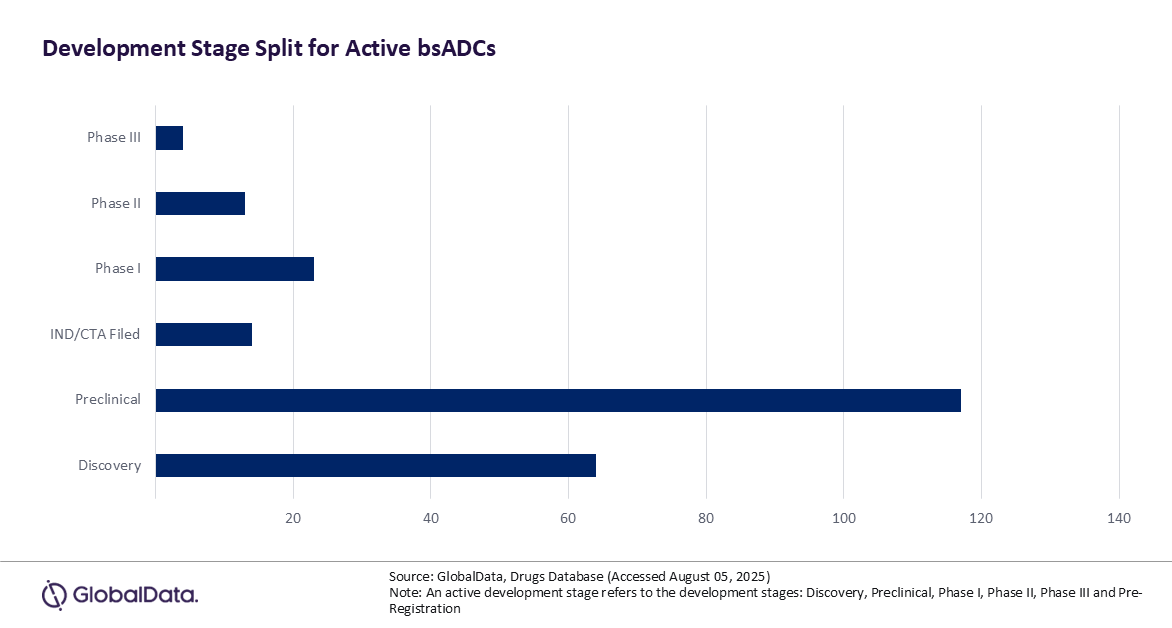

According to GlobalData’s Drugs Database, there are currently 211 bsADCs in the development pipeline, representing only 14% of the 1,554 active ADCs. Furthermore, 84% of bsADCs are in the early development stages of preclinical or discovery and are yet to reach clinical trials, highlighting the early life cycle of this landscape. However, there are four bsADCs in Phase III, all hoping to become the first approved therapy for this unique drug class.

All four Phase III bsADCs are being developed for East Asian markets. Systimmune and Bristol Myers Squibb’s izalontamab brengitecan, Shanghai JMT-Bio Technology’s JSKN-003, and Chia Tai Tianqing Pharmaceutical Group’s TQB-2102 are focused on China, whereas Amgen’s maridebart cafraglitide targets the Japanese market.

Jasper Morley, Pharma Analyst at GlobalData, comments: “This regional concentration aligns with the dominance of Chinese companies in ADC development and suggests that the first bsADC approval may occur in Asia, rather than in the US or EU. Alternatively, the most advanced bsADC in development for the US is Avenzo Therapeutics’ DB-1418, currently only in Phase II for non-small cell lung cancer.”

In continuation with traditional ADCs, three of these four Phase III products are oncology-based. Alternatively, Amgen’s maridebart cafraglitide is under development for obesity and type 2 diabetes. This antibody-peptide conjugate functions as a glucagon-like peptide (GLP-1R) agonist and a gastric inhibitory polypeptide receptor (GIPR) antagonist. Success for this product would mark the first non-oncology approval for an ADC product, potentially broadening the clinical perception of the modality.

Morley concludes: “The emergence of bsADCs marks a promising evolution in targeted therapeutics. While 84% of products remain in early development, the four late-stage contenders are poised for regulatory approval in East Asia. These products could provide new standards for efficacy and selectivity, while also expanding the therapy area scope past oncology. Upcoming years will decide whether bsADCs remain a niche innovation or emerge as a cornerstone of precision medicine.”