Oil and Gas Sector Strategies for Low Carbon Fuels Market Overview, Production Outlook, Trends and Analysis

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Oil and Gas Sector Strategies for Low Carbon Fuels Market Report Overview

Oil and gas players are exploring many strategies to branch into the low-carbon fuels market. One pathway includes producing renewable diesel and SAFs through coprocessing or the conversion of existing refineries by repurposing existing equipment. Another pathway includes long-term investments into renewable standalone refineries, which require greater upfront capital but can scale production to far higher capacities than co-processing and conversion refineries.

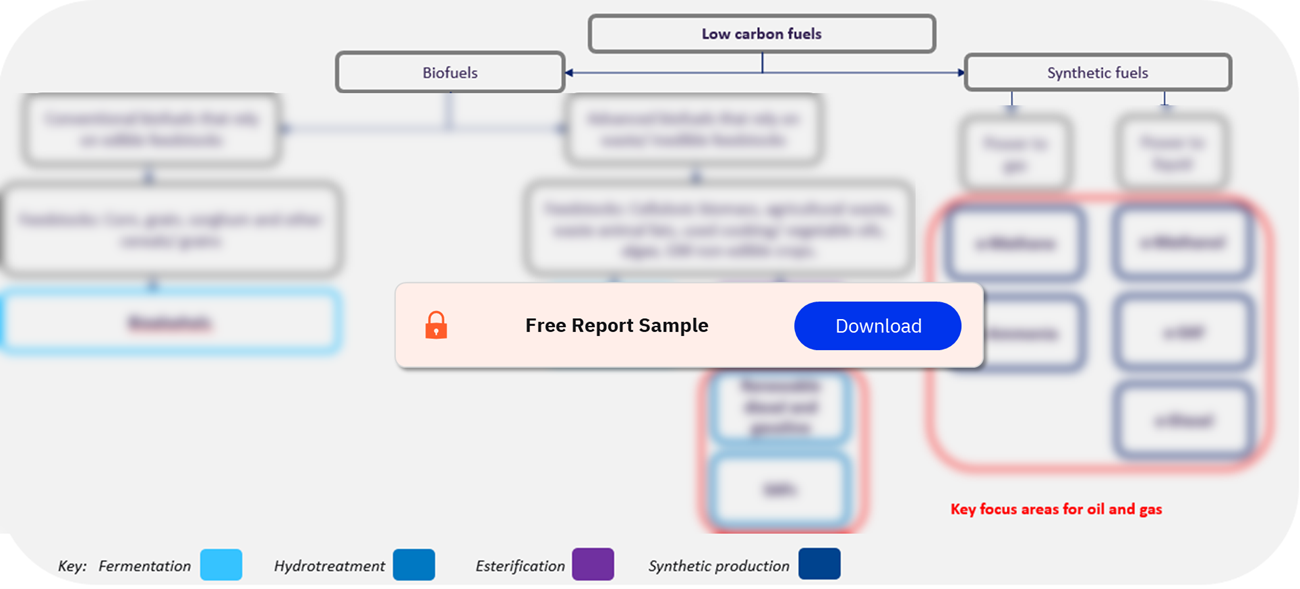

Oil And Gas Focus Areas in The Low Carbon Fuels Market

Buy the Full Report for More Insights into the Oil and Gas Sector Strategies for Low Carbon Fuels Market, Download a Free Report Sample

| Key Fuel Alternatives | · Renewable Diesel

· SAFs · Synthetic Fuels |

| Key Companies | · Valero Energy Corp

· Eni SpA · Nestle Corp · Canadian Natural Resources · BP PLC |

| Key Projects | · Decatur Renewable

· Rotterdam Renewable · Martinez Renewable · St. Charles Renewable |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

The oil and gas sector strategies for low carbon fuels market research report provides oil and gas sector strategies for low-carbon fuels. It enlists legislative framework for biofuels, with primary focus on RD and SAF. It furthermore provides sector strategies for transitioning into renewable fuels, including refinery retrofitting.

Sector Strategies for Transitioning to Renewable Fuels

Oil and gas companies are investing in different types of renewable refinery which are coprocessing, crude oil refinery conversion, and renewable standalone. Renewable standalone is the most capital intensive, as it requires a newly built refinery tailored specifically for renewable fuels. However, renewable standalone refineries are unconstrained by an existing refinery footprint and so have the potential to produce higher renewable fuel volumes than coprocessing and conversion plants. Therefore, while they require higher initial investments, they can also yield higher profits in the event of a strong increase in demand for renewable fuel products.

Furthermore, some companies have been investing in retrofitting as a diversification strategy due to the predicted decline in fossil fuel demand. Moreover, retrofitting provides a good alternative for a struggling conventional refinery.

Buy the Full Report for More Strategy Insights into the Oil and Gas Sector Strategies for Low Carbon Fuels Market, Download a Free Report Sample

Major Fuel Alternatives for the Oil and Gas Sector

The fuel alternatives that hold the most opportunity for oil and gas players are renewable diesel, sustainable aviation fuels (SAFS), and synthetic fuels. They offer a route to decarbonization that allows the industry to continue providing products and services to its existing consumer industries while diversifying its assets and decreasing the risk of its infrastructure becoming obsolete.

Renewable Diesel: Renewable diesel (RD) production and consumption are both set to grow significantly, between 2020 and 2032, where they are set to reach a peak. The vast majority of RD capacity is coming from the US. One of the causes behind this growth was federal and state policies, aimed at reducing emissions by encouraging production of alternative fuels. For example, the Renewable Fuel Standard (RFS), and the Blender’s Tax Credit mandated a minimum amount of biofuel production.

SAFs: SAFs will experience the strongest growth between 2020 and 2035 and, as a result, represent a promising area of development for the oil and gas industry. In terms of production, North America is set to increase its production the most. However, in terms of consumption, the region with the predicted highest growth is Asia.

Synthetic Fuels: Synthetic fuels have the potential to play a key role in decarbonizing hard-to-abate industries, such as aviation and maritime, as well as help automotive manufacturers meet increasingly stringent emission standards.

Buy the Full Report for More Fuel Alternative Insights into the Oil and Gas Sector Strategies for Low Carbon Fuels Market, Download a Free Report Sample

Low Carbon Fuels Market – Competitive Landscape

The oil and gas companies that are leading the production of renewable diesel in 2024 are Valero Energy Corp, Eni SpA, and Nestle Corp among others. Furthermore, the leading producers of SAFs in 2024 are BP PLC, Darling Ingredients Inc, and Nestle Corp among others. Additionally, Canadian Natural Resources is the only major oil and gas company among the top synthetic fuel producers.

Low Carbon Fuels Market by Competitors

Buy the Full Report for More Competitor Insights into the Oil and Gas Sector Strategies for Low Carbon Fuels Market, Download a Free Report Sample

Low Carbon Fuels Market – Major Projects

A few of the prominent projects in the low carbon fuels market are Decatur Renewable, Rotterdam Renewable, Martinez Renewable, and St. Charles Renewable among others. The majority of large renewable diesel projects are based in the United States.

Low Carbon Fuels Market by Projects

Buy the Full Report for More Project Insights into the Oil and Gas Sector Strategies for Low Carbon Fuels Market, Download a Free Report Sample

Scope

The report provides:

- Oil and gas sector strategies for low-carbon fuels.

- Legislative framework for biofuels, with specific focus on RD and SAF.

- Sector strategies for transitioning into renewable fuels, including refinery retrofitting.

- Crude oil refinery conversion and coprocessing vs renewable standalone.

- Renewable diesel: market outlook and leaders.

- SAFs: market outlook and leaders.

- Synthetic fuels: market outlook and leaders.

Key Highlights

Capacities for all three types of renewable refineries (crude oil refinery conversion, coprocessing and renewable standalone) are forecast to keep increasing through to 2030.

Crude refinery conversion and crude refinery co-processing capacities are both set to grow at a CAGR of 14% between 2024 and 2030.

Renewable standalone capacity is growing at the highest rate, with a CAGR of 30% between 2024 and 2030.

For all three types of refineries, between 2024 and 2030, a shift can be witnessed where capacity is increasingly being devoted to SAFs as opposed to RD.

RD production and consumption are both set to grow at a CAGR of 12% and 12.5%, respectively, between 2020 and 2032, where they are set to reach a peak.

Global SAF production and consumption are both set to grow at a CAGR of 44% between 2020 and 2035.

Synthetic fuel production from low-carbon hydrogen is set to keep growing, with a positive CAGR of 58% between 2025 and 2030, with a spike in capacity in 2030 (over 10mtpa).

Reasons to Buy

- Identify decarbonizing market trends within the oil and gas sector, including the analysis of the strategies that the biggest industry players are implementing.

- Develop market insight into the major technologies and pathways used to decarbonize the industry, including refinery retrofitting as well as investment into standalone refineries, with a focus on renewable diesel, sustainable aviation fuels, and synthetic fuels.

- Identify the key policies driving development and which countries have the most established legislative framework for said technologies.

- Facilitate the understanding of what is predicted to happen in the renewable fuels market within the next decade.

Marathon Petroleum Corp

Chevron Corp

Eni SpA

Valero

BP plc

China Petroleum and Chemical Corporation (Sinopec)

Phillips 66

Canadian Natural Resources

GAIL (India)

Enel SpA

Repsol SA

HF Sinclair Corp

Petroleo Brasileiro SA

Compania Espanola de Petroleos SAU

Calumet Inc

PBF Energy Inc

TotalEnergies SE

CVR Energy Inc

ExxonMobil Corp

Global Clean Energy Holdings Inc

World Energy LLC

PBF Energy Inc

Corral Petroleum Holdings AB

PT Petramina (Persero)

Darling Ingredients Inc

Beijing Haixin Energy Technology Co Ltd

Henan Junheng Industrial Group Biotechnology Co Ltd

Seabord Energy

ECO Biochemical Technology Co Ltd

Shijiangzhuang Changyou Bioenergy Co Ltd

Crimson Renewable Energy LLC

Azure Sustainable Fuels Corp

Gevo Inc

DG Fuels LLC

Summit Agricultural Group

AGT Food and Ingredients Inc

Federated Co-operatives Ltd

Steamboat Fuels LLC

Evolve Transition Infrastructure LP

Hobo Renewable Diesel LLC

Parkland Corp

Ecovyst Inc

Overseas Shipholding Group Inc

Clean Energy Fuels Corp

Carnarvon Energy Ltd

Suncor Energy Inc

Kinder Morgan Inc

Green Plains Inc

Global Partners LP

Calumet Specialty Products Partners LP

Dalek US Holdings Inc

Imperial Oil Ltd

Acelen (Brazil)

Henan Junheng Industrial Group Biotechnology Co Ltd

Oriental Energy Co Ltd

World Kinect Corp

Green Plains Inc

Johnson Matthey Plc

Ecovyst Inc

Calumet Specialty Products Partners LP

Worley Ltd

General Electric Co

Sasol Ltd

Airbus SE

Rolls-Royce Plc

Viva Energy Group Ltd

Puma Energy Holdings

OMV AG

Shell Plc

Mitsui & Co Ltd

European Energy AS

Yara International AS

Skive GreenLab Biogas ApS

Intercontinental Energy Corp

CWP Global

Climate Impact Corp

HIF Global

Aqua Aerem Pty Ltd.

Table of Contents

Table

Figures

Frequently asked questions

-

What are the major fuel alternatives that hold the most opportunity for oil and gas players?

The fuel alternatives that hold the most opportunity for oil and gas players are renewable diesel, sustainable aviation fuels (SAFS), and synthetic fuels.

-

Which companies are the leading producers of SAFs in 2024?

The leading producers of SAFs in 2024 are BP PLC, Darling Ingredients Inc, and Nestle Corp among others.

-

Which country has the largest renewable diesel projects?

The majority of large renewable diesel projects are based in the United States.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Sample Report

Oil and Gas Sector Strategies for Low Carbon Fuels Market Overview, Production Outlook, Trends and Analysis was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Ethanol and Biodiesel reports