Spain Defense Market Size, Trends, Budget Allocation, Regulations, Acquisitions, Competitive Landscape and Forecast to 2029

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Spain Defense Market Report Overview

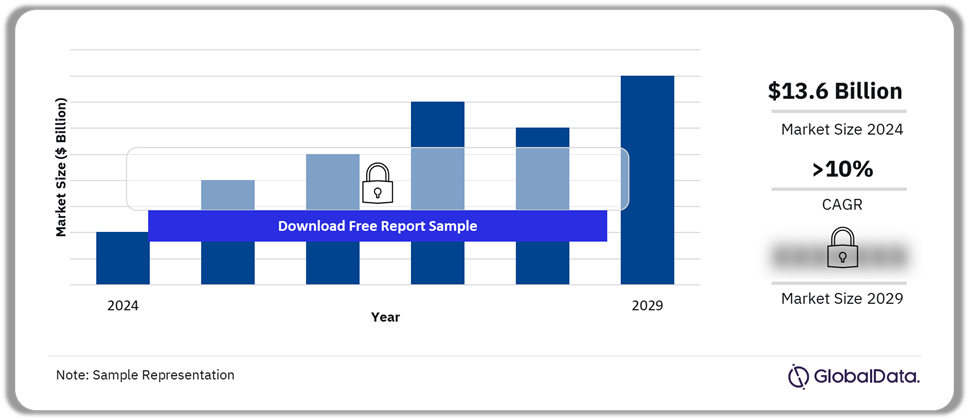

In 2024, Spain’s defense budget is worth $13.6 billion. For the 2024 financial year, the Spanish government chooses to repeat the 2023 budget that will result in a slightly smaller budget. Political deadlock in the Spanish parliament resulting from a narrowly divided government is responsible for this decreased budget. The country’s defense budget will grow at a CAGR of more than 10% during 2025-2029. The invasion of Ukraine and the resulting instability are the main drivers responsible for increasing the defense spending in the country.

Spain Defense Market Outlook, 2024-2029 ($ Billion)

Buy the Full Report for More Insights into the Spain Defense Market Forecast

The Spain defense market research report provides the market size forecast and the projected growth rate for the next five years. Furthermore, our analysts have carried out a comprehensive industry analysis to determine key market drivers, emerging technology trends, key sectors, and major challenges faced by market participants. The Spain defense market study has also assessed key factors and government programs that are expected to influence the demand for military platforms over the forecast period.

| Market Size (2024) | $13.6 billion |

| CAGR (2025-2029) | >10% |

| Forecast Period | 2025-2029 |

| Historical Period | 2020-2024 |

| Key Drivers | · Conflict in Ukraine

· Development of the domestic defense industry |

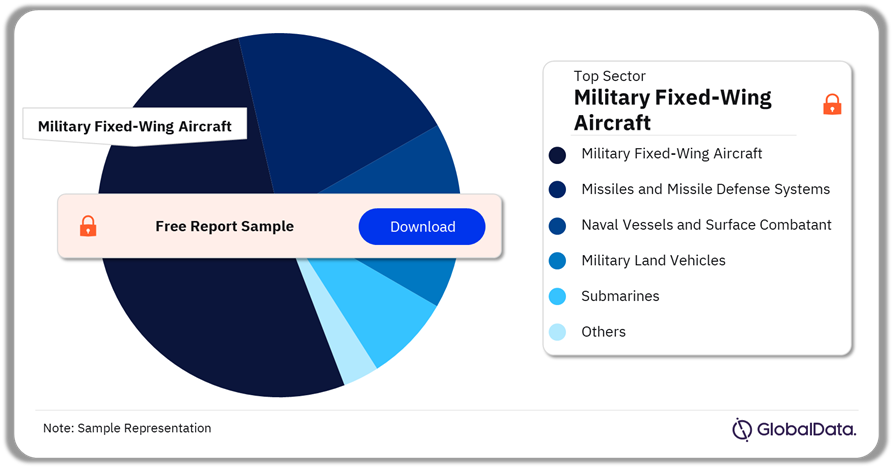

| Key Sectors | · Military Fixed-Wing Aircraft

· Missiles and Missile Defense Systems · Naval Vessels and Surface Combatants · Submarines · Military Land Vehicles |

| Leading Companies | · Dassault Aviation SA

· Airbus SE · Indra Sistemas SA · Enaire · Abengoa SA |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

Spain Defense Market Drivers

Conflict in Ukraine and the growing development of the domestic defense industry are a few of the factors driving Spain defense market growth.

- Conflict in Ukraine: The conflict in Ukraine is the largest driver of Spanish acquisition spending, with the Spanish government committing to increasing spending by a certain percentage of GDP by 2029. Statements by Spanish officials following the invasion of Ukraine have highlighted that they view unity between allied Western forces as being critical for ongoing security.

Buy the Full Report for More Information on Spain’s Defense Market Drivers

Download a Free Report Sample

Spain Military Doctrines and Defense Strategies

Defense planning for the armed forces is a cyclical process, beginning with the concept of employment of the armed forces, which is a guiding framework for defense priorities under the national security strategy. The next stage is the development of structure and funding for personnel, finance, technology, and industry-related areas for defense planning. The cycle is completed once the resource, operational, and force plans are transposed into the Military Planning Directive (DPM). The Spanish Armed Forces’ military doctrine is aligned with the NATO framework. Land, maritime, aerospace, cognitive (intangible environments such as communication techniques, and perceptions), and cyber are considered the operational domains of the Spanish Armed Forces.

Being a committed member of NATO and the EU is one of the strategic alliances practiced by Spain. Although the individual capability of the Spanish military remains sub-optimal, its sovereignty and security are guaranteed by Article 5 of the NATO constitution. The country has recommitted its support to the organization in the wake of Russia’s invasion of Ukraine.

Buy the Full Report for More Insights on the Military Doctrines and Defense Strategies in the Spain Defense Market

Spain Defense Market Segmentation by Sectors

The key sectors in the Spain defense market are military fixed-wing aircraft, missiles and missile defense systems, naval vessels and surface combatants, submarines, and military land vehicles, among others. In 2024, military fixed-wing aircraft accounted for the highest Spain defense market share.

Spain Defense Market Analysis by Sectors, 2024 (%)

Buy the Full Report for More Sector Insights into the Spain Defense Market

Buy the Full Report for More Sector Insights into the Spain Defense Market

Spain Defense Market - Competitive Landscape

A few of the leading defense companies operating in Spain are:

- Dassault Aviation SA

- Airbus SE

- Indra Sistemas SA

- Enaire

- Abengoa SA

Dassault Aviation SA: Dassault Aviation SA, headquartered in Paris, Ile-de-France, France, is a subsidiary of Groupe Industriel Marcel Dassault SA. The company is a designer and manufacturer of combat aircraft and business jets. The company provides business jets under Falcon, military aircraft under Rafale and Mirage, and unmanned combat air vehicles (UCAV) under nEUROn brands. Dassault Aviation serves defense, civil, and space satellite agencies. It also develops space transportation systems and microlaunchers. The company offers various aerospace vehicles, including intermediate experimental vehicles, suborbital vehicles, and air-borne micro-launchers.

Spain Defense Market Analysis by Companies

Buy the Full Report for More Company Insights into the Spain Defense Market

Buy the Full Report for More Company Insights into the Spain Defense Market

Segments Covered in the Report

Spain Defense Market Sectors Outlook (Value, $ Billion, 2020-2029)

- Military Fixed-Wing Aircraft

- Missiles and Missile Defense Systems

- Naval Vessels and Surface Combatants

- Submarines

- Military Land Vehicles

Scope

The report provides:

- A detailed analysis of Spain’s defense market, with market size forecasts covering the next five years.

- Insights into the strategy, security environment, and defense market dynamics of the country. .

- Defense Budget Assessment: This chapter covers the defense budgeting process, market size forecasts, drivers of expenditure, and allocation analysis. It also examines key market trends and insights.

- Military Doctrine and Security Environment: Detailed analysis of military doctrine, strategic alliances, geopolitical dynamics, and the political, social, and economic factors influencing the security environment.

- Market Entry Strategy and Regulations: This section elaborates on essential aspects of procurement policy and market regulations, market-entry routes, key defense procurement bodies, and major deals.

- Market attractiveness and emerging opportunities: It evaluates the attractiveness of various defense sectors, indicating cumulative market value, and highlights the top sectors and defense segments by value in the country.

- Defense Platforms Import and Export Dynamics: Provides an understanding of the defense platform imports and exports of the country from 2016 to 2023. Both imports and exports of the country are provided in terms of value ($M) and volume (units), categorized by country and sector.

- Defense Platform Acquisitions: It offers an overview of defense platform acquisitions by value. It lists current defense procurement schedules for the major ongoing and planned military platforms that have been formulated in the country and elaborates on the reasons leading to the procurement of the same.

- Fleet Size: Outlines the current fleet sizes of the Army, Air Force, and Navy, detailing the year of acquisition, units in service, and the prime contractor for the equipment.

- Competitive Landscape: Profiles the main defense companies operating in the country, offering insights into their business overviews, latest contracts, and financial results.

Key Highlights

• Modernization of equipment and contribution to NATO are key factors driving defense expenditure

• Major ongoing procurement program include procurement of New Generation Fighter (NGF) – Future Combat Air System, Eurofighter Typhoon Tranche 4, F-110 Class Frigates, European MALE RPAS (Eurodrone), Ground Based Air Defence (GBAD) System

Reasons to Buy

- Determine prospective investment areas based on a detailed analysis of Spain’s defense market trend over the next five years.

- Understand the underlying factors driving demand for different defense and internal security segments in Spain and identify the opportunities offered.

- Strengthen your understanding of the market in terms of demand drivers, market trends, and the latest technological developments, among others.

- Identify the major threats driving the Spain defense market and provide a clear picture of future opportunities that can be tapped, resulting in revenue expansion.

- Channel resources by focusing on the ongoing programs undertaken by the Spain government.

- Make correct business decisions based on an in-depth analysis of the competitive landscape consisting of detailed profiles of the top defense equipment providers in the country. The company profiles also include information about the key products, alliances, recent contracts awarded, and financial analysis, wherever available.

Table of Contents

Frequently asked questions

-

What is the Spain defense market size in 2024?

The defense market size in Spain is $13.6 billion in 2024.

-

What will the Spain defense market growth rate be during the forecast period?

The defense market in Spain is expected to achieve a CAGR of more than 10% during 2025-2029.

-

Which sector holds the highest share of the Spain defense market in 2024?

Military fixed-wing aircraft holds the highest share of the Spain defense market in 2024.

-

Which are the key companies operating in the Spain defense market?

A few of the leading defense companies operating in Spain are Dassault Aviation SA, Airbus SE, Indra Sistemas SA, Enaire, and Abengoa SA, among others.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Sample Report

Spain Defense Market Size, Trends, Budget Allocation, Regulations, Acquisitions, Competitive Landscape and Forecast to 2029 was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Aerospace and Defense reports