Uveitis – Global Drug Forecast and Market Analysis to 2029

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Corticosteroids are typically the first line of therapy for most patients with uveitis as these drugs are very effective and have anti-inflammatory effects. However, as corticosteroids are associated with the development of cataracts and changes in intraocular pressures, it is becoming increasingly common for other immunosuppressants such as antimetabolites and calcineurin inhibitors to be prescribed alongside first-line treatments. Immunosuppressants suppress the inflammatory response, which is what drives uveitis. This means that 45.2% of drug sales for uveitis are expected to be generated by long-acting immunosuppressants in 2029, a rise from 28% in 2019.

Magdalene Crabbe, Senior Pharma Analyst at GlobalData, comments: “Long-acting non-steroidal drugs are the future of therapy in the uveitis space. Uveitis is characterised by ocular inflammation, and immunosuppressants can offer a quick anti-inflammatory response without the risks often associated with corticosteroids. Further, long-acting immunosuppressants work for two or more weeks.”

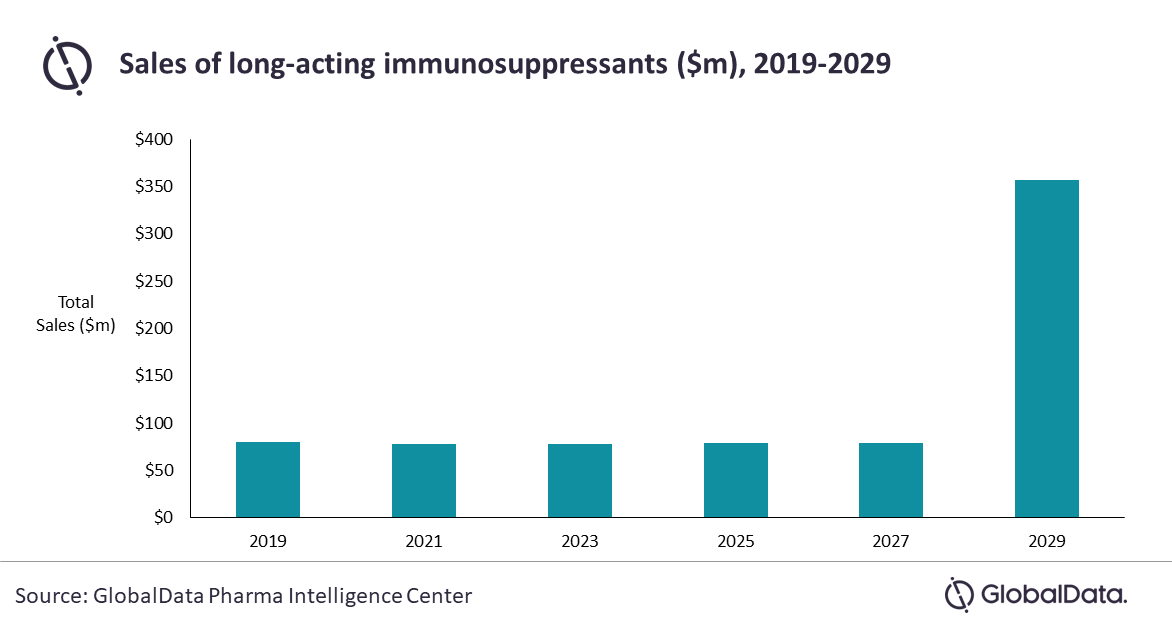

Uveitis drug sales in the nine major markets (9MM*) are expected to almost triple from $286m in 2019 to $790m in 2029. Sales of long-acting immunosuppressants reached $80m in 2019, and these drugs are expected to generate $357m in 2029.

While more chronic and recurrent uveitis patients will experience relief from treatment with long-acting immunosuppressants, a key issue in this therapy area is the need to develop drugs that can be administered by the patient.

Crabbe continues: “The greatest advantage of some immunosuppressants is the fact that they are inserted into the eyes, which reduces the risk of systemic side effects. This is especially important for patients with autoimmune diseases and comorbidities that negatively affect patients’ quality of life.”

*9MM: US, France, Germany, Italy, Spain, UK, Japan, Canada, and Australia

Scope

Overview of epidemiological data, including information about disease duration (acute, chronic, recurrent), localization (anterior, intermediate, posterior, or panuveitis), and etiology (non-infectious, infectious, or idiopathic).

Examination of pathophysiology, symptoms, diagnosis, and disease management.

Annualized forecast of sales of uveitis therapeutics in the 9MM.

Examination of unmet needs, ongoing clinical trials, and profiles of individual marketed drugs.

Assessment of pipeline drugs, including clinical and commercial aspects of each therapy in development for the treatment of uveitis in adults.

Review of key market drivers and barriers.

Discussion of market potential and opportunities for drug developers in the uveitis space.

Key Questions Answered in This Report

– What were the market leading drugs for uveitis in 2019?

– When will the late-stage pipeline products launch in each of the 9MM?

– What are the major clinical and environmental unmet needs in the uveitis market?

– What are the key commercial opportunities for pharmaceutical companies developing therapies for uveitis?

Key Highlights

- Drugs for non-infectious uveitis generated an estimated $286.3M in 2019, across the 9MM. GlobalData projects that the market will expand at a Compound Annual Growth Rate (CAGR) of 10.7%, reaching $789.7M in 2029.

- Corticosteroids and immunosuppressants such as methotrexate, azathioprine, and tacrolimus are frequently used to treat patients with uveitis. The main issue with corticosteroids is their potential to cause elevated intraocular pressures and cataracts. Most patients develop these complications after long-term treatment with steroids.

- Immunosuppressants such as azathioprine and tacrolimus take several weeks to bring about therapeutic outcomes. Humira (adalimumab) was the first biologic to gain approval for the treatment of uveitis. However, the drug is injected subcutaneously, and this has been linked to dermatological side effects and discomfort.

- Anterior uveitis makes up the majority of diagnosed prevalent cases of the disease. However, symptoms can overlap with conjunctivitis and keratitis. This can lead to misdiagnosis and delayed initiation of effective treatment.

- A number of drugs that are being developed for uveitis are also in the pipeline for other inflammatory diseases. This is useful because a significant percentage of patients with non-infectious uveitis also have an immune system-related comorbidity.

- Factors that will contribute to growth in the market include continued use of AbbVie’s Humira for the treatment of both anterior and posterior uveitis, the introduction of non-steroidal therapies for the management of patients with anterior uveitis, and the assumed increase in the number of people who develop recurrent uveitis in line with the growing prevalence of autoimmune conditions.

- Barriers to growth include the use of inexpensive generic formulations of immunosuppressants in all of the 9MM and lack of compliance among patients who are instructed to apply eye drops up to six times per day.

- The top-selling late-stage pipeline agent in 2029 will be EYS-606. This is because the drug is expected to be the only gene therapy that will become available to treat anterior uveitis during the forecast window.

Reasons to Buy

The report will enable you to:

- Develop and design your in-licensing and out-licensing strategies through a review of pipeline products and technologies, and by identifying the companies with the most robust pipeline.

- Develop business strategies by understanding the trends shaping and driving the uveitis therapeutics market.

- Drive revenues by understanding the key trends, innovative products and technologies, market segments, and companies likely to impact the uveitis therapeutics market in the future.

- Formulate effective sales and marketing strategies by understanding the competitive landscape and by analysing the performance of various competitors.

- Identify emerging players with potentially strong product portfolios and create effective counter-strategies to gain a competitive advantage.

- Organize your sales and marketing efforts by identifying the market categories and segments that present maximum opportunities for consolidations, investments and strategic partnerships.

Novartis

Wakamoto

Allergan

Johnson & Johnson

Bausch & Lomb

EyePoint Pharmaceuticals

Alimera

Pfizer

Intrapharm

Baxter Healthcare

Shionogi

Astellas

Janssen

AbbVie

Merck

Roche

Genentech

Mitsubishi Tanabe Pharma

Chugai

Santen

Aciont

Eyevensys

Oculis

Enzo Biochem

Panoptes Pharma

Tarsius Pharma

Alvotech

Dobecure

Mitotech

Sun Pharma

EyeGate Pharma

Amgen

Affibody

Revolo Biotherapeutics

Apitope International

Palatin Technologies

Reven Pharmaceuticals

Table of Contents

Table

Figures

Frequently asked questions

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

Uveitis – Global Drug Forecast and Market Analysis to 2029 was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Ophthalmology reports