The Q3 2025 global risk analysis showed a slight rise in economic risk, with the overall score increasing from 53 in Q2 to 53.2 in Q3. This increase is largely due to the full implementation of tariffs and the fading impact of frontloading, when companies accelerated activities before tariffs began, contributing to a heightened risk environment, says GlobalData, a leading intelligence and productivity platform.

GlobalData’s latest report, “Global Risk Report Quarterly Update – Q3 2025,” reveals that some regions, such as the Asia-Pacific, continue to drive global economic growth, while others, including Europe and the Americas, face significant hurdles due to political fragmentation and economic instability. The Middle East and Africa region, meanwhile, grapples with geopolitical conflicts and humanitarian crises. Globally, Ireland stands as the country with the least risk whereas Yemen stands as the country with the highest risk. As the world moves forward, addressing these risks will require coordinated efforts.

Annapurna Pillutla, Economic Research Analyst at GlobalData, comments: “As 2025 progressed, the global economy faced heightened uncertainty and inconsistent momentum. Following a robust first half, bolstered by frontloaded imports, swift supply chain adaptations, and targeted fiscal interventions, growth has slowed, leaving the outlook precarious. GlobalData forecasts a deceleration in global economic growth, from 3.02% in 2024 to 2.80% in 2025, and further to 2.77% in 2026, reflecting a gradual slowdown in activity and increasing worries about the sustainability of the earlier expansion phase.”

Europe – Rising risks and slowing growth

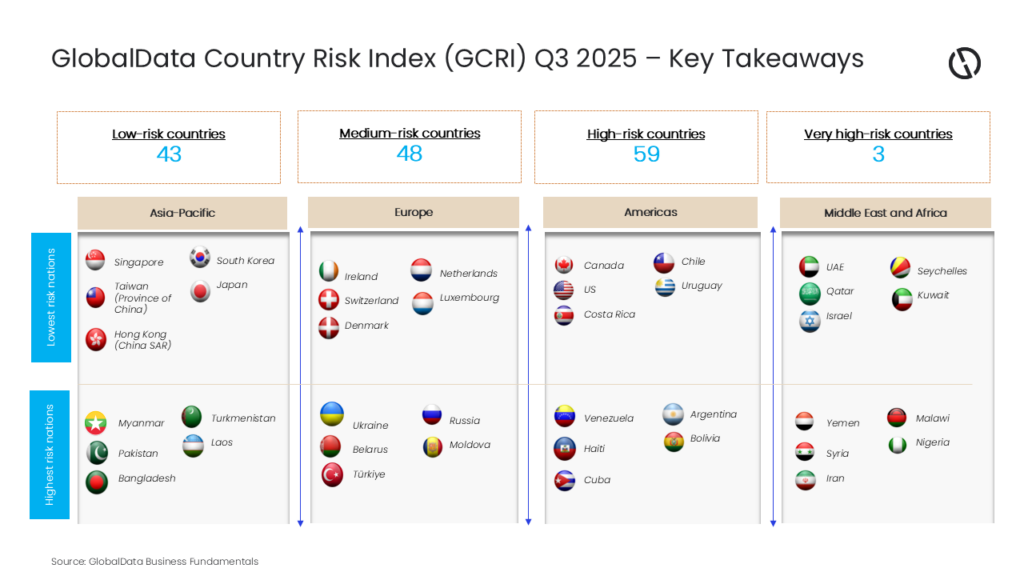

Europe’s regional risk score rose to 39.5 in Q3 2025 from 39.3 in Q2 2025, driven by tariff impacts and trade barriers. Political fragmentation and an aging population present challenges, while renewed investment in France supports growth amidst structural issues. In Europe, the lowest-risk countries include Ireland, Switzerland, and Denmark, while Turkiye, Belarus, and Ukraine were the highest-risk countries.

The region’s economic growth is expected to slow, easing to 1.45% in 2025 from 1.89% in 2024. It is projected to pick up slightly to 1.54% in 2026, supported by fiscal stimulus and a recovery in Germany.

Asia-Pacific – Trade deals ease risks amid slowing growth

The Asia-Pacific’s risk score slightly decreased to 51.5 in Q3 2025, as the US reached trade agreements with Japan, South Korea, Vietnam, Indonesia, and Bangladesh, easing tariff pressures. In the Asia-Pacific region, the countries with the lowest risk were Singapore, Taiwan (Province of China), and Hong Kong (China SAR), while the countries with the highest risk were Bangladesh, Pakistan, and Myanmar.

The region’s economic growth is projected to slow from 4.64% in 2024 to 4.47% in 2025 and 4.19% in 2026. Yet, the region is expected to lead global growth in 2025, driven by strong domestic demand in Kyrgyzstan, Vietnam, and India. Challenges include trade uncertainties, geopolitical tensions, and natural disasters.

Americas – Heightened risks from tariffs and political volatility

In Q3 2025, the Americas’ risk score remained at 54.8, with heightened risks from tariffs increasing raw material costs and consumer inflation. Political volatility, governance weaknesses, and economic instability persist. Across the Americas, Canada, the US, and Costa Rica continued to have the lowest risk, while Cuba, Haiti, and Venezuela had the highest risk.

The region’s economic growth is projected at 1.45% in 2025 and 1.82% in 2026, supported by stronger ties and investments from Asia, though gains are uneven. Significant political risks exist in Venezuela, Haiti, and Nicaragua, while climate change, forced displacement, and migration exacerbate regional political and social conflicts.

Middle East and Africa – Rising challenges amid economic diversification

In Q3 2025, the Middle East and Africa’s risk score increased slightly to 63.5 from 63.2 in Q2 2025, facing challenges from reduced global demand and ongoing geopolitical tensions. Economies like Saudi Arabia and the UAE are using technology and tourism for growth diversification. In the Middle East region, the lowest risk countries were the UAE, Qatar, and Israel, while Iran, Syria, and Yemen remained the highest risk nations.

The region’s economic growth is expected to rise from 1.48% in 2024 to 2.02% in 2025 and 2.09% in 2026, driven by higher oil production and reforms. However, the region remains vulnerable to geopolitical conflicts, political instability, corruption, and oil price shocks, alongside worsening humanitarian crises.

Pillutla concludes: “GlobalData’s Q3 2025 assessment underscores a world economy entering a more fragile phase as tariff impacts fully filter through supply chains and the temporary boost from frontloading fades. While the overall rise in global risk is modest, the distribution of pressures is uneven. With growth expected to slow through 2026, coordinated policy, trade clarity, and conflict mitigation will be central to stabilizing the outlook.”