A resurgence of COVID-19 cases could reduce the on-premise consumption of ice creams in China, one of the most lucrative markets for these frozen desserts. Despite this, the Chinese ice cream market will expand to CNY62.7 billion ($4.2 billion) by 2026, registering a compound annual growth rate (CAGR) of 3.8% over 2021–26, says GlobalData, a leading data and analytics company.

GlobalData’s report, “China Ice cream – Market Assessment and Forecasts to 2026,” reveals that artisanal ice cream will register the fastest value CAGR of 4.5% over 2021–2026, followed by the take-home and bulk ice cream category.

Bobby Verghese, Consumer Analyst at GlobalData, comments: “Rising consumer purchasing power has catapulted China to one of the world’s top ice cream markets. Consumers are spoilt for choice with thousands of international and domestic brands fighting for shelf space. Innovation is rife, with consumers demanding natural and healthy formulations and novel flavors. By tapping events, such as the Single’s Day and 618 shopping festivals, and occasions such as the Qixi Festival and the Chinese New Year, leading brands have broken the perception of ice cream as a seasonal treat.”

The Chinese ice cream market has diverged, with both value-for-money and premium brands gaining equal traction. Premium brands have gained significant appeal, supported by quality- and brand-conscious Millennial and Gen Z consumers who are influenced by Western culinary trends.

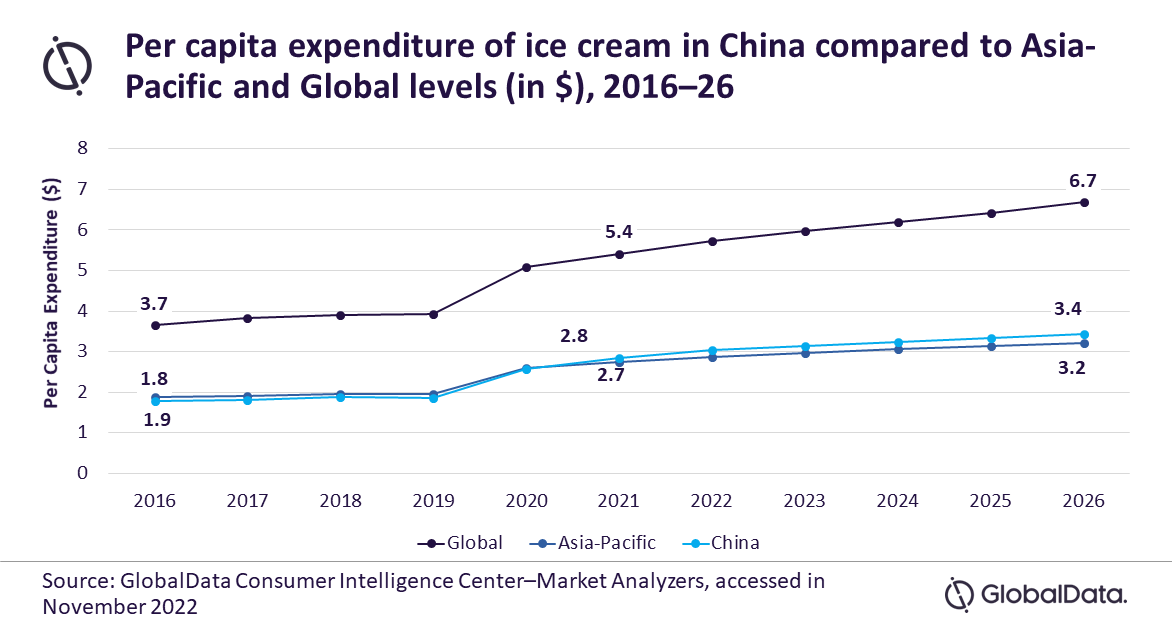

Consequently, China’s per capita expenditure (PCE) on ice cream increased from $1.8 in 2016 to $2.8 in 2021, surpassing the regional average of $2.7. However, it lagged the global average of $5.4, thereby indicating ample room for further market growth. China’s PCE on ice cream will increase to $3.4 by 2026, catalyzed by intensive marketing campaigns and retailer push, according to GlobalData.

Convenience stores was the leading distribution channel in the Chinese ice cream market in 2021, followed by hypermarkets & supermarkets, and food & drinks specialists. Yili Group, Unilever, and China Mengniu Dairy were the top three companies in value terms in 2021, while Yili and Cornetto were the leading brands.

Verghese concludes: “The Omicron caseload resurged in late 2022 as authorities relaxed the stringent Zero-COVID policy amid the economic slowdown and rising public resentment. With consumers sheltering at home, on-premise and on-the-go consumption of ice cream will be hit. Moreover, the rising raw material costs due to the pandemic and the Russia–Ukraine conflict are escalating product prices. Urban shoppers are already bemoaning the dearth of cheap traditional popsicles in retail stores. Also, authorities are cracking down on obscure local brands that sell costly ice cream without clearly indicating prices on packaging labels.”