Cybersecurity in Insurance – Thematic Intelligence

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Cybersecurity in Insurance Thematic Intelligence Report Overview

Cybersecurity is widely recognized as a disruptive theme by many industries including insurance. Robust cybersecurity defenses are essential in the insurance industry to mitigate the risk caused by rapid digitalization, and geopolitical conflicts. Global cybersecurity revenues in insurance are headed for strong growth over the next three years.

The ‘Cybersecurity in Insurance’ thematic intelligence report explores the impact of cybersecurity at every level of the insurance value chain. It provides a comprehensive analysis of the industry, including real-life case studies that showcase the areas of cybersecurity in which insurance companies should focus their time and resources to protect their networks, systems, and sensitive data. It also covers value chain insights, sectoral scorecard analysis, market players, and the competitive landscape within the theme.

| Page No. | 55 |

| Key Value Chain Components | · Hardware

· Software · Services |

| Leading Cybersecurity Adopters | · AIG

· Allianz · Aon |

| Leading Cybersecurity Vendors | · Accenture

· Alphabet · Check Point · Cisco · Cloudflare |

| Leading Specialist Cybersecurity Vendors | · Blackberry

· CyberCube · Portnox |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

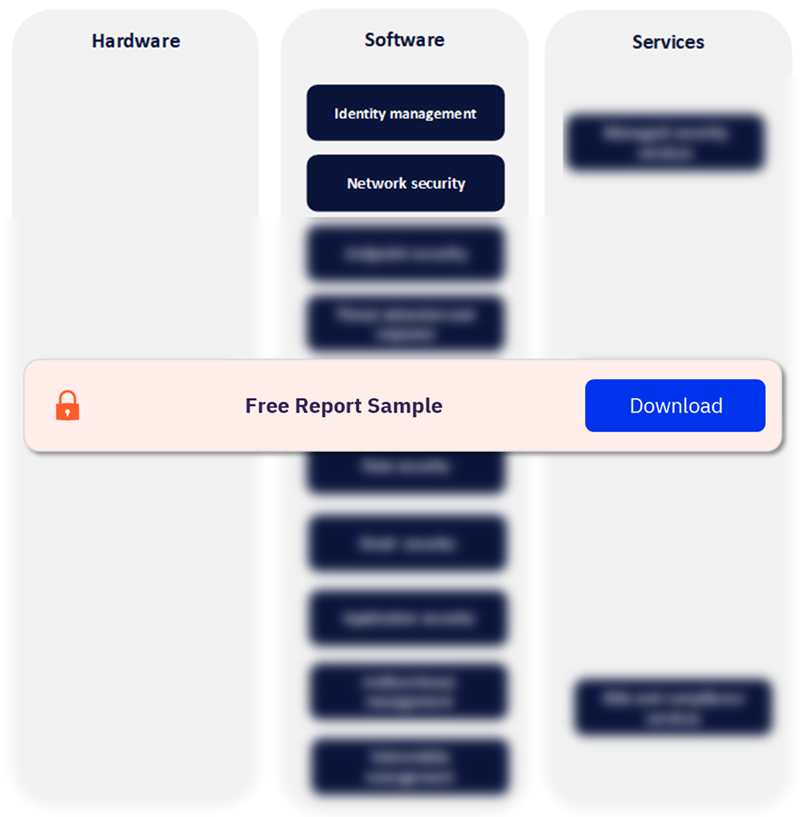

Cybersecurity Value Chain Analysis

The cybersecurity value chain is categorized into hardware, software, and services. The software component can be further sub-segmented into identity management, and network security, among others.

The Cybersecurity Value Chain

Buy the Full Report for More Insights into the Cybersecurity Value Chain in the Insurance Sector Download a Free Report Sample

Cybersecurity in Insurance – Competitive Landscape

A few leading insurance companies deploying cybersecurity are:

- AIG

- Allianz

- Aon

A few leading vendors associated with the cybersecurity theme are:

- Accenture

- Alphabet

- Check Point

- Cisco

- Cloudflare

A few leading specialist cybersecurity vendors in the insurance sector are:

- Blackberry

- CyberCube

- Portnox

Buy the Full Report to Know More About the Leading Players in the Cybersecurity Theme

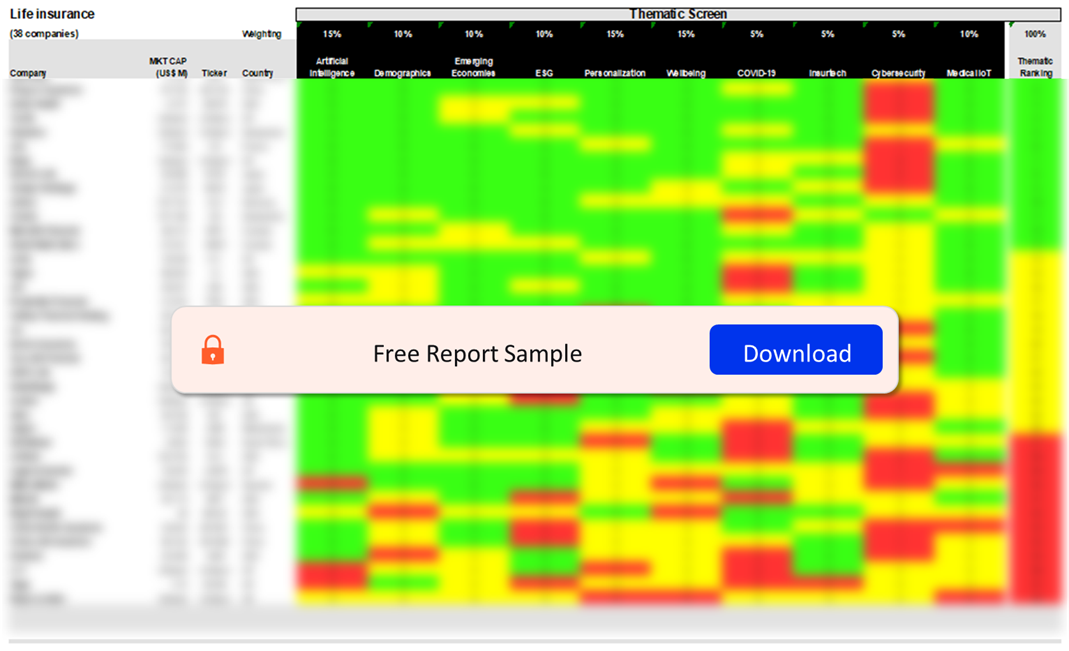

Sector Scorecard Analysis

At GlobalData, we use a scorecard approach to predict tomorrow’s leading companies within each sector. Our scorecard has three screens: a thematic screen, a valuation screen, and a risk screen.

- The thematic screen ranks companies based on overall leadership in the 10 themes that matter most to their industry, generating a leading indicator of future performance.

- The valuation screen ranks our universe of companies within a sector based on selected valuation

- The risk screen ranks companies within a particular sector based on overall investment risk.

Life Insurance Sector Scorecard

Buy the Full Report to Know More about the Insurance Sector Scorecards in the Cybersecurity Theme

Download a Free Report Sample

Scope

This report provides an in-depth look at the cybersecurity theme in the insurance sector, covering industry challenges, how cybersecurity impacts these challenges, the cybersecurity investment matrix, case studies, the value chain, market forecasts, industry signals, and more.

Key Highlights

- With increased digitalization, all insurance firms must now prioritize cybersecurity.

- COVID-19 has forced firms to digitalize at a fast pace, leaving more surface area open for cyberattacks.

- In 2019 global security revenues in the insurance industry were $5bn. By 2024 this figure will reach $6.4bn.

Reasons to Buy

- Position yourself for success by understanding how cybersecurity—one of the biggest themes of the decade—should be deployed within the insurance sector to mitigate the challenges of rapid digitalization.

- Source the leading and specialist vendors of cybersecurity technologies for the insurance sector. Discover what each vendor offers and who some of their existing clients are.

- Quickly identify attractive investment targets in the insurance industry by understanding which companies are most likely to be winners in the future based on our thematic scorecard.

- Gain a competitive advantage in the insurance industry by understanding the value of cybersecurity solutions for each segment of the insurance value chain.

- Benchmark yourself against the rest of the market.

Allianz

Aviva

Chubb

Hiscox

Marsh

Munich Re

Ping An

Swiss Re

Travelers

Zurich Insurance

Tokio Marine Holdings

Prudential Financial

Allstate

Bright Health

Table of Contents

Frequently asked questions

-

What are the key value chain components in the cybersecurity in insurance theme?

The key components of the cybersecurity value chain comprise hardware, software, and services.

-

Which are the leading insurance companies deploying cybersecurity?

A few of the leading insurance companies deploying cybersecurity are AIG, Allianz, and Aon among others.

-

Which are the leading vendors associated with the cybersecurity theme?

A few of the leading vendors associated with the cybersecurity theme are Accenture, Alphabet, Check Point, Cisco, and Cloudflare.

-

Which are the leading specialist cybersecurity vendors in the insurance sector?

A few of the leading specialist cybersecurity vendors in the insurance sector are Blackberry, CyberCube, and Portnox among others.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Sample Report

Cybersecurity in Insurance – Thematic Intelligence was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Insurance reports