Tech Apps in Banking – Report Bundle (7 Reports)

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Banks are currently undergoing technological churn owing to increased competition from fin-tech startups and growing concern about cyber-security. Online deposits, mobile wallets, e-bill payments, and other similar services have changed the way financial transactions are conducted today. As technological advancements continue to disrupt traditional banking methods, the world will witness a plethora of newer and faster banking solutions.

As a part of this bundle, you will gain access to in-depth insights available in the following reports:

- Thematic Research: Cybersecurity in Payments

- Thematic Research: Data Privacy in Banking

- Thematic Research: Digital Lending

- Thematic Research: Digital Transformation in Banking

- Thematic Research: Mobile Payments

- Thematic Research: Online Payments

- Thematic Research: The Internet of Things in Banking

Report 1: Thematic Research: Cybersecurity in Payments

As the world’s payment environment becomes more cashless, the growth in digital payment transaction value is expected to increase. This will translate into a growing opportunity for providers of cybersecurity products and services, as banking and payment providers will look to utilize newer and more advanced cybersecurity infrastructure and services for fending off cyber criminals. During 2019-24, the size of payment transactions by value is projected to grow, especially in the payment card and mobile payments spaces. AI is expected to play a significant role in defending against cyberattacks especially when hackers will continue to implement methods including the use of AI that will make cyberattacks more difficult to detect.

Cybersecurity Value Chain Analysis

For more value chain insights, download a free report sample

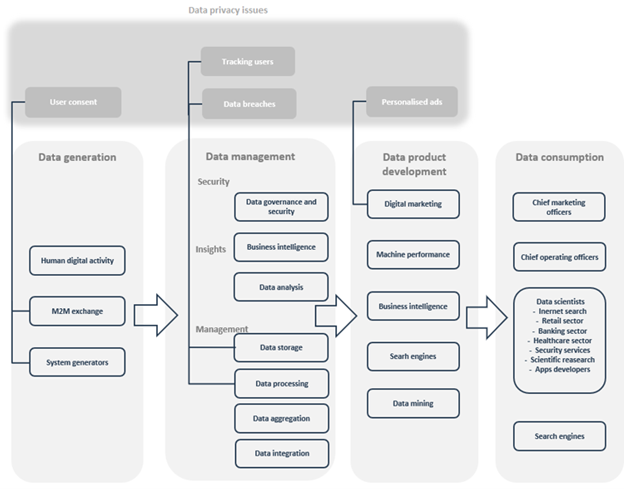

Report 2: Thematic Research: Data Privacy in Banking

Data underpins and enriches all aspects of a retail banking service or product, whether it is optimizing channel interactions, personalizing risk assessment (across credit, market, and operational risk), or assisting customers in making better financial decisions. Data is also essential for the development of game-changing new technologies like artificial intelligence (AI), big data, and the Internet of Things (IoT). Data privacy affects the entire financial services ecosystem, including direct-to-consumer banks, vendors, and fintech partners. Some technologies are inherently incompatible with data privacy. Distributed ledger technology (DLT), for example, is promising because it is transparent, traceable, and unchangeable.

Big Data Value Chain and Data Privacy

For more value chain insights, download a free report sample

Report 3: Thematic Research: Digital Lending

Digital lending necessitates a complex mix of capabilities, including credit risk assessment, automated loan processing, onboarding, and disbursement, all of which are dependent on a particular technology. Personalization is a differentiator for modern digital lenders across all dimensions of the digital experience. COVID-19 emphasized the need for personalization because it had a highly individual impact on customers and sectors, invalidating many of the generic assumptions that had previously underpinned long-standing credit risk models. Incumbent banks operating on legacy platforms can digitally transform by acquiring critical new technology capabilities and must collaborate with a wide range of innovative software vendors and public cloud providers to succeed in digital lending.

Digital Lending Value Chains

For more value chain insights into the digital lending industry, download a free report sample

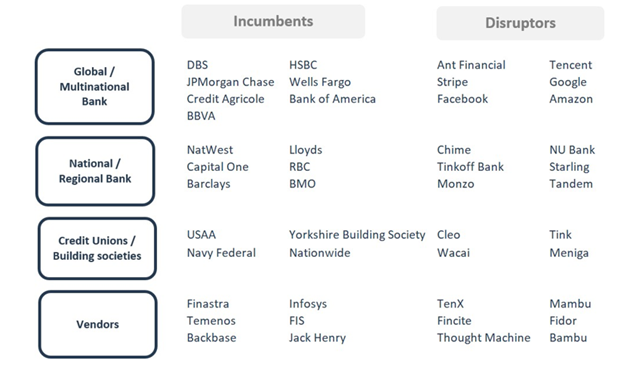

Report 4: Thematic Research: Digital Transformation in Banking

Digital banking comprises a vast ecosystem of provider types and business models. During the pandemic, many new digital banks were far better placed to adapt and evolve to different banking processes. As a result, there is now a renewed emphasis on building agility and flexibility into the underlying technological platform so incumbents may more easily pivot to offer clients new sources of value. Massive increases in client app usage, remote working, and security and fraud risk have all forced banks to adapt, and cloud-based technologies have been crucial in doing so.

Leading Players in the Digital Transformation Theme

To know more about the key players, download a free report sample

Report 5: Thematic Research: Mobile Payments 2022

The mobile payments market size was valued at $55.7 trillion in 2021 and is expected to achieve a CAGR of more than 21% between 2021-2025. Machine learning is largely being leveraged in the mobile payments industry for improving fraud detection and prevention. The mobile payments market has already replaced or eclipsed card-based payments in developing and emerging economies. This led to a massive disparity in the performance of mobile proximity payments between the developed and the developing world. Future mobile payment systems that attain omnichannel reach by utilizing the versatility of a mobile P2P or m-commerce system will be the most successful.

Mobile Payments Value Chain

For more insights on value chains in the mobile payments market, download a free report sample

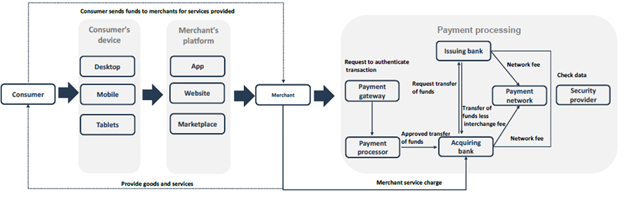

Report 6: Thematic Research: Online Payments

The e-commerce value was worth $4.8 trillion in 2021, with China representing just over a third of the value of transactions made during that period. Ecommerce is expected to grow further as an increasing number of consumers shop online rather than in physical stores. The COVID-19 pandemic accelerated this trend, as consumers worldwide were forced to rely on online shopping for the majority of 2020, and this trend continued in 2021 as well. As the global economy accelerates its shift away from cash, transactions will shift from physical POS to online platforms.

Online Payments Value Chain Analysis

For more value chain insights, download a free report sample

Report 7: Thematic Research: The Internet of Things in Banking

The IoT market was worth $622 billion in 2020 and is expected to achieve a CAGR of more than 12% during 2020-2024. The enterprise IoT dominates the overall IoT market and is expected to do so in the days to come. IoT has the potential to provide highly personalized and frictionless digital banking. More internet-connected ‘things’ will assist banks in anticipating what customers want, when they want it, and where they want it, delivering highly personalized content and functionality optimized for brief moments of interaction. AI, 5G, cybersecurity, and cloud computing are four key enabling technologies for IoT. In a post-COVID-19 world, a new wave of digital transformation is expected to fuel higher growth across the IoT.

IoT Value Chain Analysis

For more IoT value chain insights, download a free report sample

Key Players - Data Privacy in Banking – Thematic Research

Key Players - Digital Lending – Thematic Research

Key Players – Digital Transformation in Banking – Thematic Research

Key Players - Mobile Payments 2022 – Thematic Research

Key Players - Online Payments – Thematic Research

Key Players - The Internet of Things in Banking – Thematic Research

Table of Contents

Frequently asked questions

-

FAQs - Cybersecurity in Payments – Thematic Research

-

What will be the key area of growth for the payments market over the next few years?

Over the next few years, the key area of growth for payments will be e-commerce as consumer purchasing habits will shift from offline to online.

-

FAQs - Data Privacy in Banking – Thematic Research

-

Why has the need for cloud migration increased?

The increasing volume and velocity of data have increased the need for cloud migration.

-

FAQs - Digital Lending – Thematic Research

-

What are the components of digital lending value chains?

The components of digital lending value chains can be segmented into four parts: pre-sales and sales, set-up and onboarding, processing and underwriting, and closing and disbursement.

-

FAQs - Digital Transformation in Banking – Thematic Research

-

What are the components of digital transformation value chains?

The core components of digital transformation value chains are core banking/legacy systems (transaction processing), digital banking platforms (front-end channels), API management/strategy (middleware), money management/data infrastructure, and niche fintech partners.

-

FAQs - Mobile Payments 2022 – Thematic Research

-

What are the components of digital transformation value chains?

The core components of digital transformation value chains are core banking/legacy systems (transaction processing), digital banking platforms (front-end channels), API management/strategy (middleware), money management/data infrastructure, and niche fintech partners.

-

FAQs - Mobile Payments 2022 – Thematic Research

-

What are the different types of mobile payments?

Mobile payments can be segmented into four types: mobile proximity payment, m-commerce, mobile P2P, and mobile POS.

-

What are the different components of the mobile payments value chain?

The different components of the mobile payments value chain are consumer, merchant acceptance, and payment processing.

-

FAQs - Online Payments – Thematic Research

-

What was the most dominant payment tool in 2020?

In 2020, the dominant payment tool in most nations was card payments.

-

FAQs - The Internet of Things in Banking – Thematic Research

-

What are the business benefits of IoT?

Some of the business benefits of IoT include enhanced operational efficiency, reduced costs, improved decision-making, and better customer experience.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

Tech Apps in Banking – Report Bundle (7 Reports) was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Financial Services reports