Europe Regional Retail Banking Analysis by Consumer Credit, Retail Deposits and Residential Mortgages

Powered by ![]()

All the vital news, analysis, and commentary curated by our industry experts.

Europe Regional Retail Banking Report Overview

The low interest rate environment in Europe has kept net interest margins low. However, monetary policy tightening will have likely put an end to this prolonged period, as banks will now be more able to create a spread between deposit and lending rates. The European Central Bank’s (ECB) projections of the average annual inflation rate suggest that inflation will subside in 2023 but will remain above the 2% target rate until the second half of 2025. As a result, European economies are expected to stagnate in the coming years. The raising of interest rates in response to inflation will have a delayed effect, but we predict that this effect will be felt down the line in the form of economic growth rates hovering below 1%.

This report analyzes the European retail banking sector from a comparative perspective, highlighting key similarities and differences across markets within the region. The largest banks in each market-among other useful banking-related statistics, such as average net interest margin are provided alongside macroeconomic forecasts, giving a feel for the composition of a given country’s economy and retail banking sector.

| Key Countries | France, the UK, Germany, Sweden, Netherlands, Norway, Belgium, Denmark, Finland, Poland, Spain, Ireland, and Italy |

| Key Banks | Sparkassen, Credit Agricole, Lloyds Banking Group, Caisses d’Epargne, La Caixa, Intesa Sanpaolo, Banque Populaire, La Banque Postale, BNP Paribas, Deutsche Bank, Natwest Group, Barclays, HSBC, Virgin Money, and Banca BPER |

| Key Product Ownerships | Investment Product Ownership, Current Account Product Ownership, Credit Product Ownership, and Insurance Product Ownership |

| Enquire & Decide | Discover the perfect solution for your business needs. Enquire now and let us help you make an informed decision before making a purchase. |

Europe Regional Retail Banking Market Segmentation by Banks

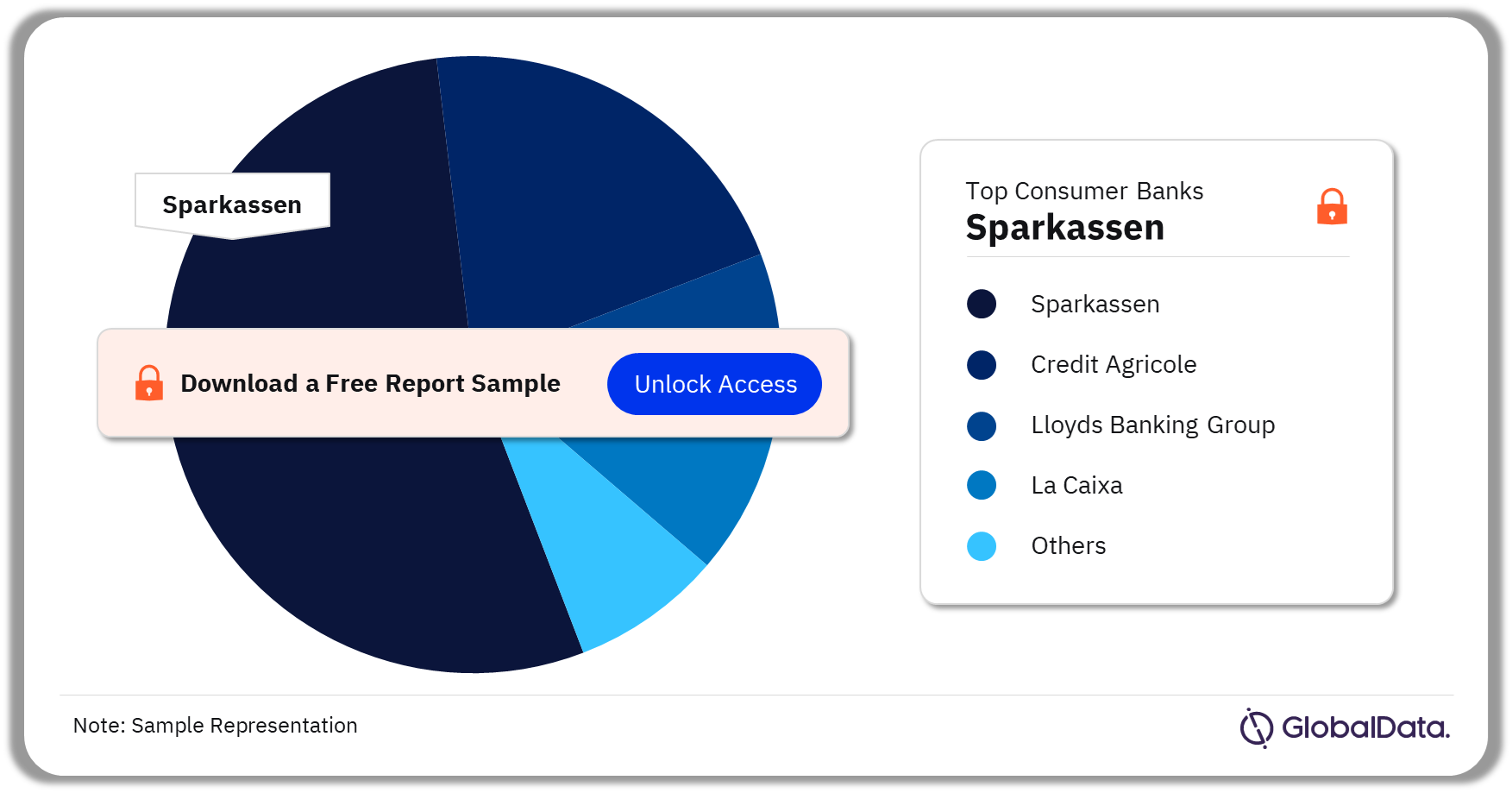

The top consumer banks in Europe are Sparkassen, Credit Agricole, Lloyds Banking Group, Caisses d’Epargne, La Caixa, Intesa Sanpaolo, Banque Populaire, La Banque Postale, BNP Paribas, Deutsche Bank, Natwest Group, Barclays, HSBC, Virgin Money, and Banca BPER among others. Sparkassen in Germany, Credit Agricole in France, and Lloyds Banking Group in the UK are the three largest banks by retail deposits in Europe.

Top European Consumer Banks Retail Deposits, 2022 (%)

For more insights on the top consumer banks in the Europe regional retail banking market, download a free sample report

Europe Regional Retail Banking Market Segmentation by Countries

The key countries in the Europe regional retail banking market are France, the UK, Germany, Sweden, Netherlands, Norway, Belgium, Denmark, Finland, Poland, Spain, Ireland, and Italy among others. The Netherlands has the highest levels of retail deposit market concentration in Europe, whereas the UK has the largest mortgage market.

Retail Deposit Balances: Germany and France possess the largest markets for retail deposits. Poland is predicted to have one of the fastest GDP growth rates and highest average inflation rates in the EU. The combination of these factors likely explains why the value of retail deposits held in Poland is expected to grow at the fastest rate of any of the countries covered here over the next four years.

Retail mortgage market concentration: The UK has the largest residential mortgage market in Europe at present, and this is predicted to remain the case over the next four years. For most countries, the inflation effect is keeping the value of the mortgage market afloat. However, in Denmark, the rate hike effect has dominated, and house prices have fallen at the fastest rate in more than a decade.

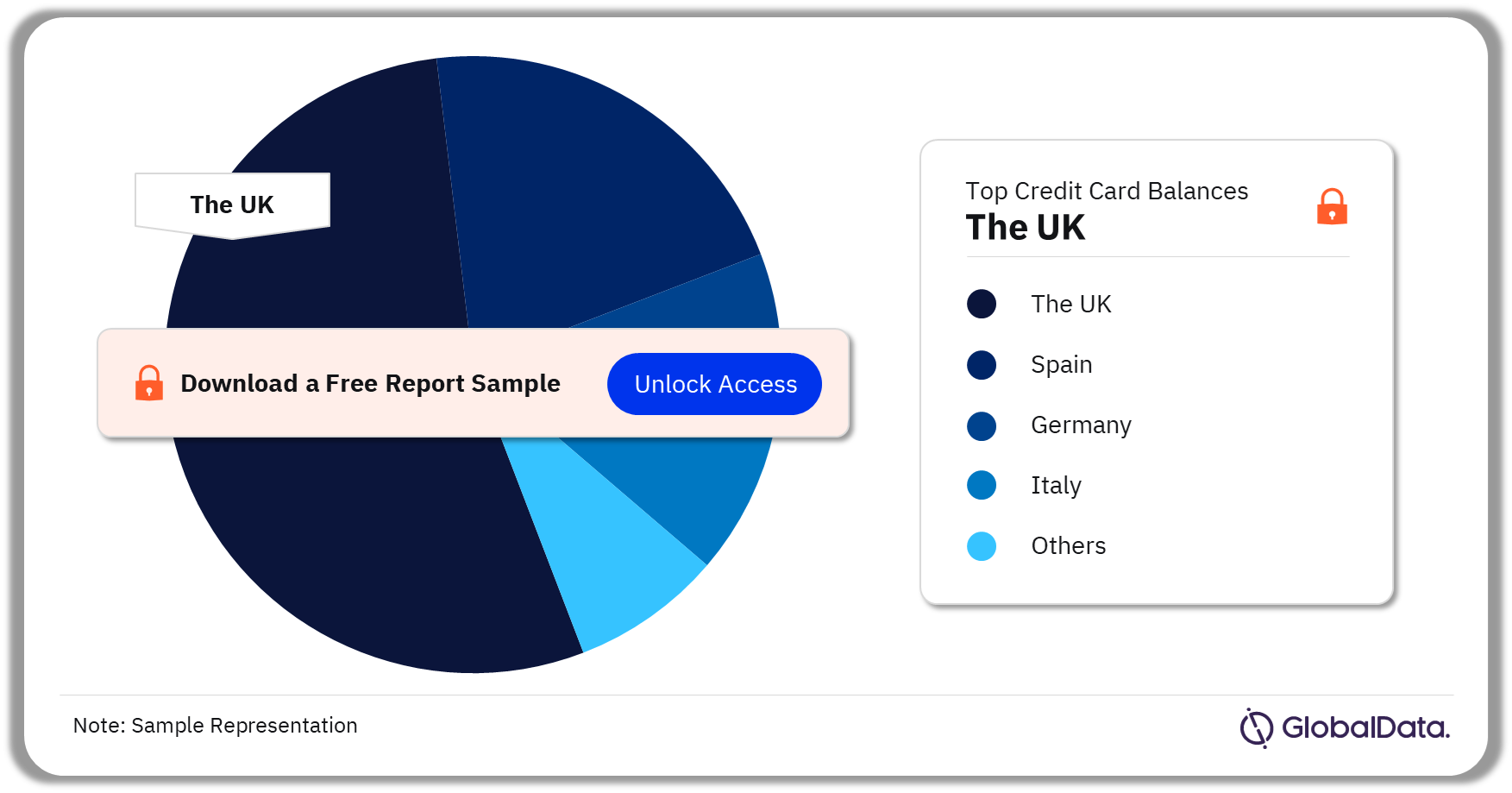

Credit Card Balances: The UK has the highest level of credit card debt of any country covered in this report. UK customers were the third-most likely to own a credit card out of the countries covered, behind France and Spain. The Netherlands has the smallest value of credit card balances left outstanding. This result is not surprising considering that only 44% of Dutch respondents made use of credit cards, the lowest percentage of the countries covered. Cultural aversion to the accumulation of debt is the most likely explanation for the country’s low credit card usage.

Personal Loan Balances: Germany has the highest value of personal loans outstanding. Yet despite this, German respondents were some of the least likely to have taken out a personal loan. Ireland has the lowest value of personal loans outstanding out of the countries covered.

Europe Regional Retail Banking Market Analysis by Credit Card Balances, 2022 (%)

For more country-wise insights on the Europe regional retail banking market, download a free sample report

Europe Regional Retail Banking Market Segmentation by Product Ownership

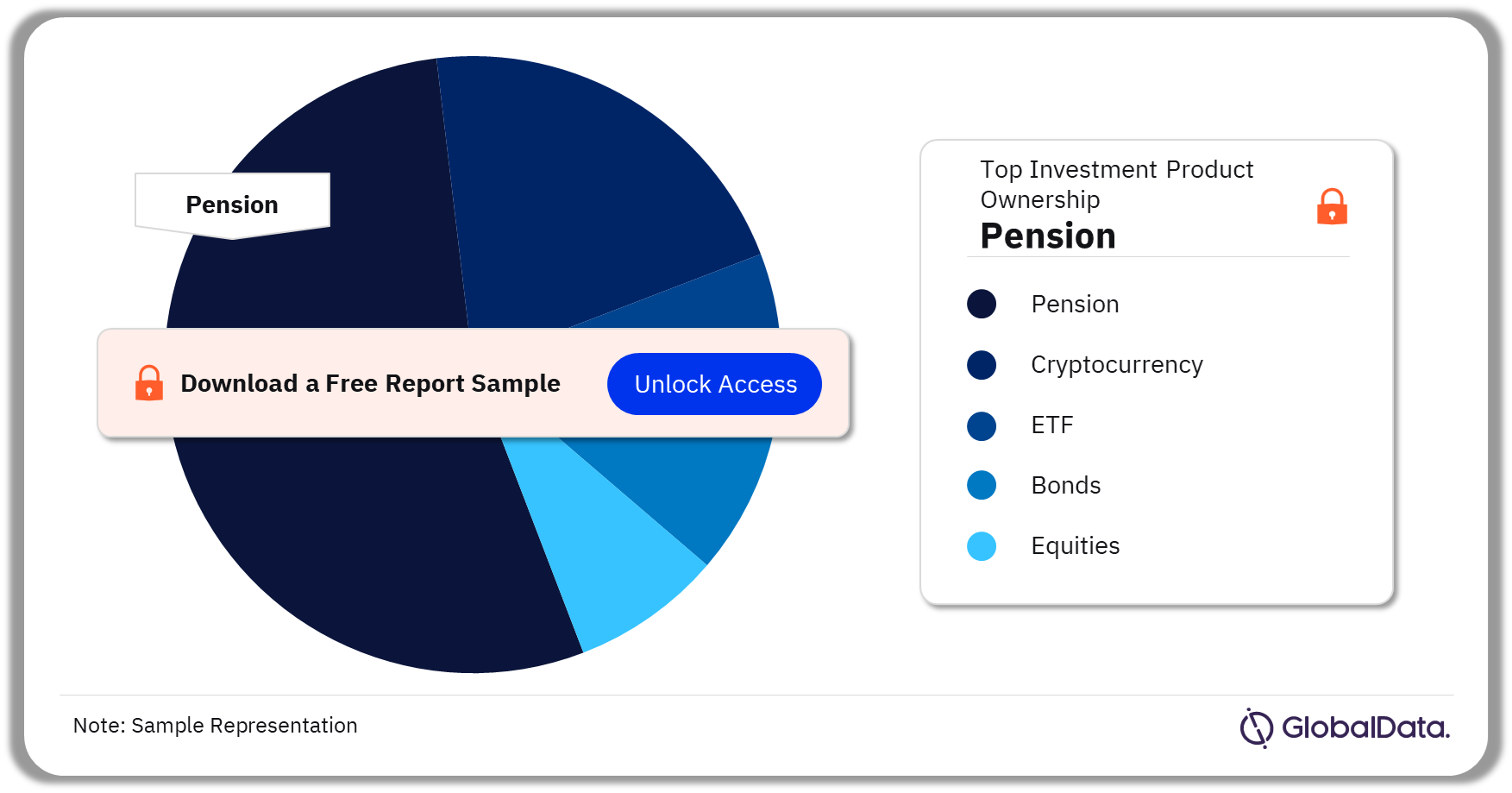

Investment Products Ownership: The key investment products are cryptocurrency, ETF, bonds, pensions, and equities. In 2022, private pension plans were distinctly more popular in majority of the European economies. In terms of popularity, cryptocurrencies have come to rival traditional forms of investment.

Current Account Products Ownership: Charge card or deferred debit cards, cash accounts, prepaid cards, and savings accounts are some of the leading banking products owned by consumers in the Europe regional retail banking. Prepaid cards are unpopular in Europe, with the notable exception of Italy. Prepaid cards tend to be adopted by the poor when there is a cost attached to holding a current account. This might well explain Italy’s high level of prepaid card usage considering banking fees are common and the country has a lower GDP per capita than most of the other countries considered in this report.

Credit Products Ownership: The key credit products owned by consumers in the European economies are credit cards, mortgages, personal loans, BNPL in-store, and BNPL online. Customers are much less likely to use credit cards in the Netherlands than anywhere else. This is primarily down to cultural attitudes: whereas in other markets, such as the US, the idea of being an indebted consumer is accepted, it is not in the Netherlands.

Insurance Products Ownership: Some of the main insurance products owned by the consumers in the Europe economies are travel, house/contents, life, mobile, motor, and private health. The lowest level of private health insurance holding is found in the UK, undoubtedly a result of the UK’s National Health Service. Home/contents and motor insurance are the most popular forms of insurance. Houses, their contents, and vehicles are of very high value, and as such, any customer who is mildly loss-averse is likely to want to get these insured, even if the actual risk of damage or loss of one of these is quite low.

Europe Regional Retail Banking Market Analysis by Products Ownerships, 2022(%)

For more product ownership insights on the Europe regional retail banking market, download a free sample report

Scope

• Sparkassen in Germany, Credit Agricole in France, and Lloyds Banking Group in the UK are the three largest banks in Europe in terms of retail deposits.

• On average, the European markets for retail deposits and for residential mortgages are as concentrated now as they were five years ago.

• The Netherlands has the highest levels of retail deposit market concentration in Europe, likely the result of the relatively long tenure of the average Dutch current account customer.

• Santander’s acquisition of Banco Popular has significantly increased the level of concentration in the Spanish retail deposit market. The combined retail deposit market share of the largest five banks in Spain increased from 67% to 78% between 2016 and 2021.

Key Highlights

- Sparkassen in Germany, Credit Agricole in France, and Lloyds Banking Group in the UK are the three largest banks in Europe in terms of retail deposits.

- On average, the European markets for retail deposits and for residential mortgages are as concentrated now as they were five years ago.

- The Netherlands has the highest levels of retail deposit market concentration in Europe, likely the result of the relatively long tenure of the average Dutch current account customer.

- Santander’s acquisition of Banco Popular has significantly increased the level of concentration in the Spanish retail deposit market. The combined retail deposit market share of the largest five banks in Spain increased from 67% to 78% between 2016 and 2021.

Reasons to Buy

• Keep up to date with the macroeconomic trends impacting the retail banking sector in Europe.

• Understand where the best opportunities lie by comparing countries based on factors ranging from average net interest margin to market concentration.

• Develop an understanding of the differences between consumers’ research methods, average tenure, and channel usage across different European countries.

PwC

J.P. Morgan

Sparkassen

Credit Agricole

Lloyds Banking Group

Caisse d’Epargne

La Caixa

Intesa Sanpaolo

Banque Populaire

La Banque Postale

BNP Paribas

Deutsche Bank

NatWest Group

Barclays

Nationwide

HSBC

Santander

BBVA

Rabobank

Credit Mutuel

ING

Table of Contents

Frequently asked questions

-

Which are the top consumer banks in the Europe regional retail banking market?

Sparkassen in Germany, Credit Agricole in France, and Lloyds Banking Group in the UK are the three largest banks by retail deposits in Europe.

-

Which country has the largest retail deposit in the Europe regional retail banking market?

Germany and France have the largest retail deposit in the Europe regional retail banking market.

-

Which country has the highest credit card debt in the Europe regional retail banking market?

The UK has the highest level of credit card debt in the Europe regional retail banking market.

-

Which investment product will be dominating the Europe regional retail banking market?

Pension is the dominating investment product in the Europe regional retail banking market.

Get in touch to find out about multi-purchase discounts

reportstore@globaldata.com

Tel +44 20 7947 2745

Every customer’s requirement is unique. With over 220,000 construction projects tracked, we can create a tailored dataset for you based on the types of projects you are looking for. Please get in touch with your specific requirements and we can send you a quote.

Sample Report

Europe Regional Retail Banking Analysis by Consumer Credit, Retail Deposits and Residential Mortgages was curated by the best experts in the industry and we are confident about its unique quality. However, we want you to make the most beneficial decision for your business, so we offer free sample pages to help you:

- Assess the relevance of the report

- Evaluate the quality of the report

- Justify the cost

Download your copy of the sample report and make an informed decision about whether the full report will provide you with the insights and information you need.

Related reports

View more Retail Banking and Lending reports