31 Mar, 2022 LIC continues to lose market share in highly concentrated Indian life insurance market, reveals GlobalData

Posted in InsuranceLife Insurance Corporation of India (LIC), which has recently received the approval of the Securities and Exchange Board of India (Sebi) for its initial public offering (IPO), continues to lose its market share to private insurers such as SBI Life, HDFC Life, ICICI Prudential, and Max Life, finds GlobalData, a leading data, and analytics company.

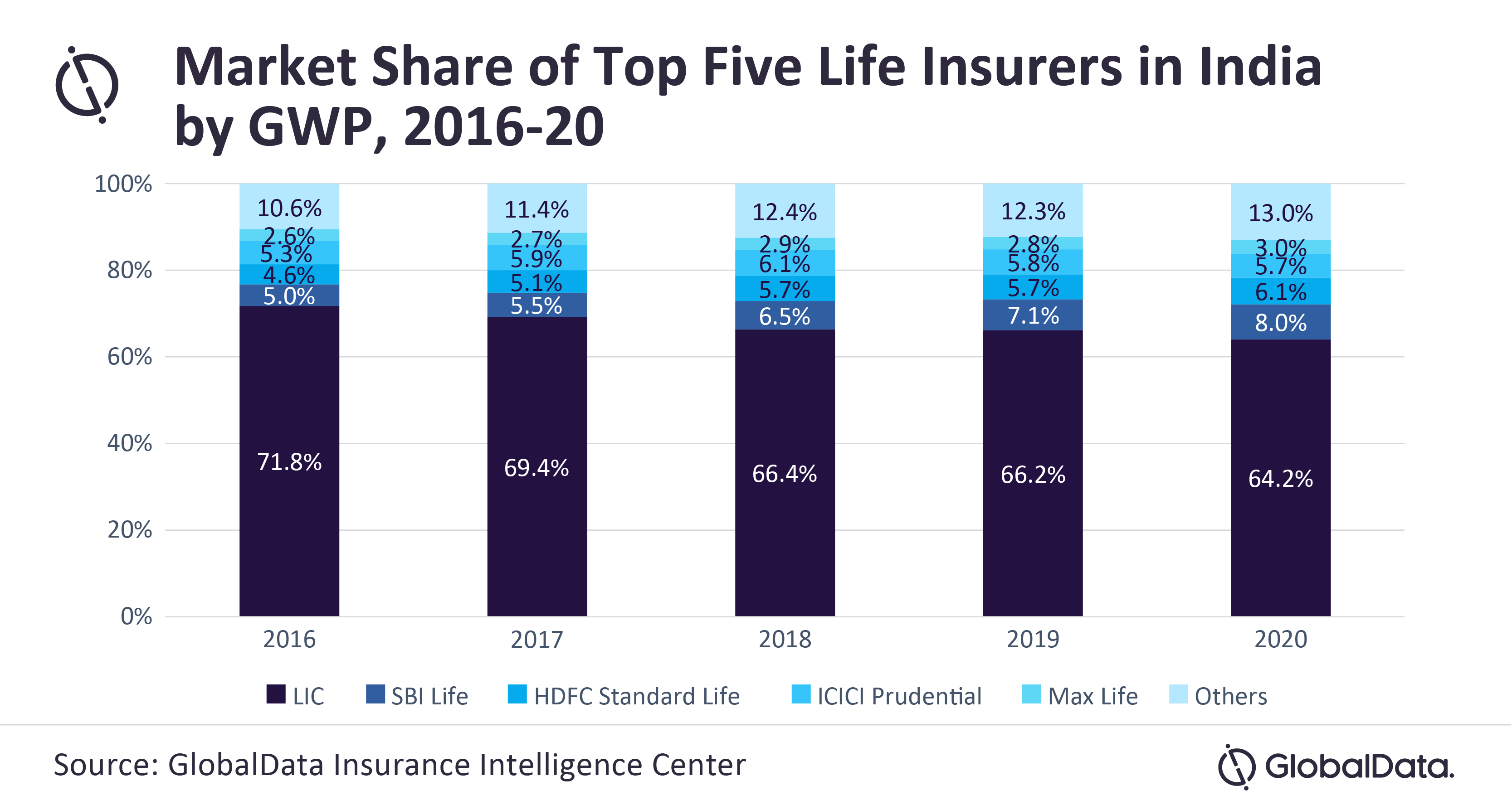

The life insurance market in India is highly concentrated with the top five insurers accounting for 87% share in 2020. Although LIC continues to be the leading insurer, its market share has declined from 71.8% in 2016 to 64.2% in 2020. SBI life moved up from being third largest insurer in 2016 to becoming second-largest insurer in 2020. Similarly, HDFC Life became the third largest insurer in 2020, moving up from fourth position in 2016.

GlobalData’s Insurance Intelligence Center reveals that except LIC, all the top four life insurers have registered double-digit growth during 2016-20. The gross written premium of LIC grew at a CAGR of 7.6% during 2016-20, whereas SBI Life registered a growth of 24.4% followed by HDFC Life with 18.7%.

Swarup Kumar Sahoo, Senior Insurance Analyst at GlobalData, comments: “LIC’s sales growth has slowed down during the last few years due to its high dependence on the traditional agency-led distribution model. Whereas private insurers have a more diversified distribution network.”

In 2020, over 94% of LIC’s first-year premiums were generated through agents and insurance advisors, with banking and alternative channels such as corporate agents, brokers and insurance marketing firms (IMF) accounting for 3.4% and direct marketing at 2.2% share.

However, private insurers that are mostly backed by banks have increasingly adopted the bancassurance channel, which has allowed them to increase sales by leveraging their existing customers.

For instance, SBI Life generated 56% of its new business from the bancassurance channel followed by agencies with 17% share and other channels at 27%. Similarly, HDFC Life generated 61% share of new business from bancassurance followed by 19% from direct marketing, 13% from agencies, and 7% from brokers and others.

Additionally, digital initiatives of private insurers to enhance customer service have also provided them an edge over LIC. This includes the ease of onboarding customers and agents through digital solutions, real-time tracking of claims as well as virtual meetings with customers to resolve their queries.

Sahoo concludes: “LIC’s market share is expected to continue to decline due to its high dependence on traditional distribution channels and low technology investments as compared to private insurers. As LIC prepares for its IPO in 2022, the continuous decline in its market share could negatively impact investor sentiment.”