The rise of alternative fuels: can biofuel feedstocks ever meet demand?

Supporting both decarbonisation strategies and supply security, biofuel demand is increasing, but feedstock availability threatens to cap growth.

The demand for biofuel is growing, with ramifications for feedstock availability and scaling. Both conventional and advanced feedstocks are experiencing surging demand, with the latter particularly sought-after by hard-to-abate industries under pressure to decarbonise.

While decarbonisation targets are driving biofuel demand, recent disruptions in the Middle East have reminded governments of the geopolitical sensitivity of oil supplies and the fragility of supply chains. Biofuels offer a reliable alternative to traditional petroleum products, supporting both decarbonisation strategies and supply security.

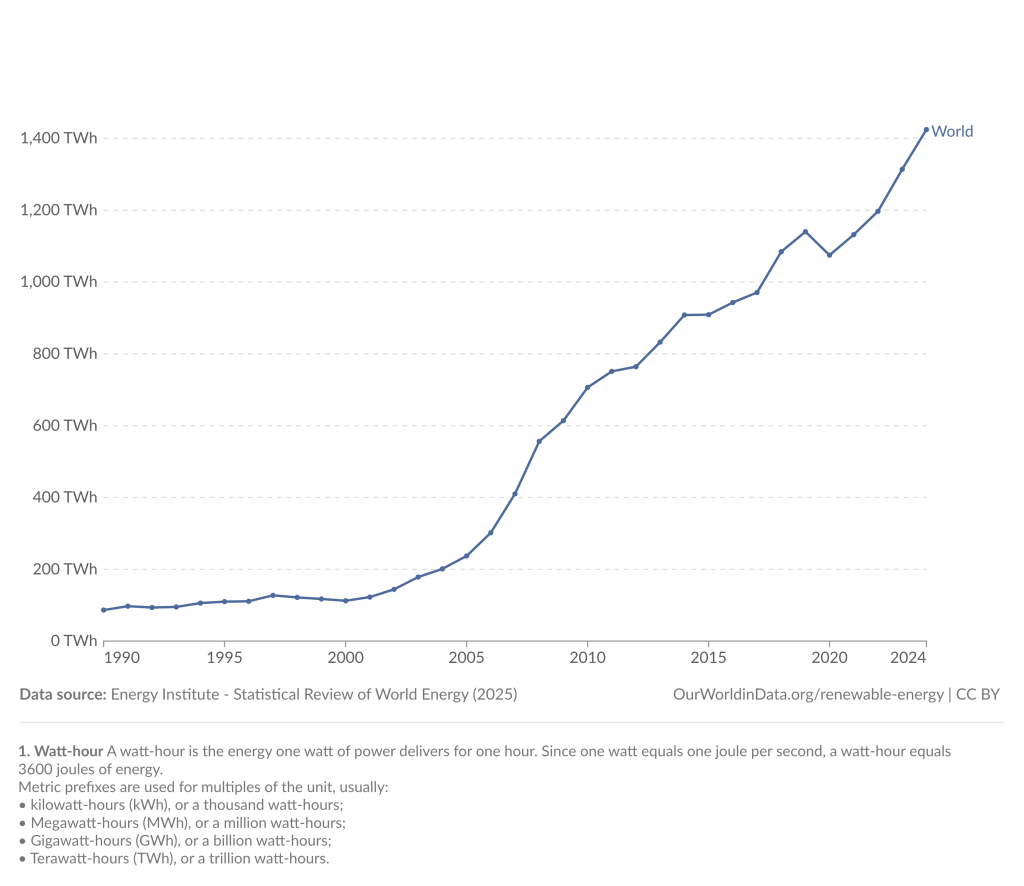

As a result, demand is on a firmly upward trajectory; production jumped from 1,074.66TW-hours (TWh) in 2020 to 1,424.52TWh in 2024, led by the US.

Global biofuel production has grown sevenfold in the past 20 years

However, biofuel production faces a fundamental constraint: feedstock availability. Production is inherently limited by the available quantity of biomass, and detractors argue that scaling up conventional feedstock production means compromising food security, while advanced feedstocks face complicated collection logistics and growing international supply competition.

As biofuel demand rises and feedstock limitations loom, the industry is approaching a structural crunch.

Clarice Brambilla, energy transition analyst at Offshore Technology’s parent company, GlobalData, notes the early signals of feedstock scarcity.

“Current biofuel production is heavily dependent on vegetable oils, used cooking oil [UCO] and animal fats, which have enabled the rapid scale-up of renewable diesel [RD] and sustainable aviation fuel [SAF] over the past decade. However, these resources are inherently limited, and increasing demand is already creating competition between fuel pathways,” she explains.

Demand and drivers: why and where are biofuels growing?

Although recent oil supply constraints have put biofuels in the spotlight, demand was already increasing prior to the current crisis.

Over the past decade, consumption growth has been relatively solid, with the Organisation for Economic Co-operation and Development (OECD) reporting an average growth of 3.3% per annum, driven primarily by blending mandates across major economies, particularly in hard-to-abate transport sectors. The EU's ReFuelEU Aviation directive, for instance, mandates increasing SAF blending ratios, while the ReFuelEU Maritime regulation imposes parallel requirements on shipping fuels.

According to GlobalData, global biodiesel production increased by 111% between 2015 and 2024, while the SAF market doubled its production between 2024 and 2025, reaching 2.3 million tonnes per annum (mtpa).

SAF alone is expected to climb from roughly 2% of the jet fuel market in 2025 to an estimated 70% by 2050, with regulatory pressure set to compound market-driven demand. Demand for SAF has shaped US biofuel exports, while announced project pipelines across North America, Europe and Asia indicate that future investment will be increasingly concentrated in SAF.

However, the expected scaling of biofuel production has ruffled feathers, and T&E energy and climate director Kädi Ristkok recently commented that “biofuels can never play more than a marginal role in our energy system without devastating consequences”, warning of “the unintended impacts on food prices”.

Currently, the majority of biomass supply comes from the agricultural sector, which includes food, collected residues and grazed biomass. Thus, agricultural feedstocks have been considered a threat to food security for local communities, particularly in emerging and middle-income economies, where much biofuel growth is centred.

Brazil is one such market. The country's biofuel demand is soaring following the introduction of a new policy in 2025 that increased the national ethanol blending mandate from 27% to 30% and the biodiesel blending mandate from 14% to 15%. Brambilla calls the country “one of the world's most ambitious biofuel markets” but points out that this growth is rooted firmly in conventional, agricultural feedstocks.

“Brazil combines abundant agricultural resources, strong government support and established infrastructure, while also benefitting from one of the world's most competitive sugarcane ethanol industries,” she says.

According to OECD figures, the US and Brazil are the main exporters of maize and sugarcane-based ethanol globally and are expected to remain so. Combined, the export share of both countries was 75% in 2025 and is expected to reach 79% in 2034.

Indonesia and India have also seen notable growth. Indonesia has expanded its biodiesel blending mandate to B35 (a mixture of 35% biodiesel and 65% diesel fuel), up from B30, while India has pursued an E20 (20% ethanol with 80% petrol) bioethanol blending target with unusual policy discipline. The country is now the world's third-largest producer and consumer of bioethanol, with production nearly tripling over five years.

The biofuel feedstock crunch

Despite significant growth across biofuel production, there is a looming bottleneck in scaling operations – not in refining capacity or blending infrastructure, but feedstock availability.

Tightening blending mandates and decarbonisation targets are widening the gap between feedstock availability and biofuel demand; this is exacerbated by the current pressure on global oil supplies, which has prompted export powerhouses like Brazil and Indonesia to limit exports of key biofuel crops.

Conventional agricultural feedstocks are not the only option, however. In fact, advanced feedstocks, such as UCO, animal fats and municipal solid waste are preferred by regulators and producers alike because they create a revenue from waste while reducing pressure on food security.

Policy incentives such as the EU’s Renewable Energy Directive (RED III) offer premium policy support for advanced feedstocks, helping to further boost profit margins. Head of biofuel commercial and sustainability at Certas Energy Oliver Bradshaw explains: “Crops tend to go into biodiesel fatty acid methyl esters, while waste oils tend to go into hydrotreated vegetable oil.

“From a commercial point of view, this is because you get more incentivisation from things like renewable transport fuel certificates in Europe. So more premium feed stocks – such as waste oils – tend to go into the more premium product because it generates larger margins.”

However, supply is necessarily structurally capped.

UCO supply is associated with foodservice, rather than biofuel demand. Collection can be small-scale and, therefore, logistically complex, with the International Energy Agency noting that UCO and animal fats could approach exhaustion by 2027. The OECD echoes this, forecasting little to no growth in waste oil and fat availability through 2030. Demand for these biofuel feedstocks has already outpaced supply, driving up premiums and compressing margins for producers.

Limited advanced feedstock availability puts pressure on conventional feedstocks, with around 8% of global cropland dedicated to biofuel feedstock production as of 2023, equating to approximately 32 million hectares. It is land and water-intensive, and biofuel production is estimated to require up to 20,000 litres of water per litre of fuel produced.

According to T&E, conventional feedstock cultivation consumes roughly 5% of the world's fertiliser supply to produce 4% of global transport fuels. Scaling conventional feedstocks could therefore risk food scarcity, putting pressure on freshwater systems and food production, often in remote, working communities.

However, producers are adamant that advanced feedstocks are not as doomed as critics might assert.

Gary Hubbard, senior vice-president of commercial and operations at the Biofuel Company, the only biofuel producer in Saudi Arabia, tells Offshore Technology that “bottlenecks are not generated within most countries who globally supply UCO”.

He explains that Europe and North America import significant volumes of UCO, creating “a false market price for what is essentially a waste item”. As a result, some governments like that of the United Arab Emirates are introducing taxes on the export of UCO to encourage local supply for biodiesel refining, while others like Indonesia’s are banning UCO and palm oil mill effluent (POME) exports entirely.

The likelihood of an impending bottleneck thus differs regionally. For some countries, it will represent a convergence of three constraints: the land and water-cost of expanding conventional sources, waste availability and inadequate collection infrastructure.

How to secure feedstock supply

A massive overhaul of collection infrastructure is one route to securing feedstock supply. However, aggregating dispersed waste streams or agricultural residues at industrial scale is difficult, even in wealthy, densely populated countries. The UK, for example, mandated household food waste collections to cover all councils by March 2026 but has failed to meet its deadline.

Yet Hubbard is confident that collection pains are surmountable: “All countries should focus on transparency and governance over local collection services, transporting to local biodiesel refineries for local consumption of biodiesel.” Localisation, he says, is “the way forward”.

However, even localised control cannot change the inherent finiteness of UCO and waste feedstock. To tackle this, the industry is looking beyond conventional and advanced feedstocks to next-generation pathways. These include algae and lignocellulosic biomass, which Bradshaw explains “includes wood waste; for example, from paper manufacturing (of which there is a lot), and other things like rice husks”.

Lignocellulosic feedstocks are largely considered to the surest ticket out of the feedstock crunch. The market was already valued at $8.2bn in 2024, with forecasts expecting it to reach $102bn by 2030. As a feedstock, cellulosic input avoids the resource strains presented by conventional feedstocks, while offering supply security and localisation beyond waste oils. However, commercialisation remains immature and there are significant, persistent pain points: lignocellulosic feedstocks require pretreatment processes that are costly at scale, and purpose-built biorefineries are capital-intensive.

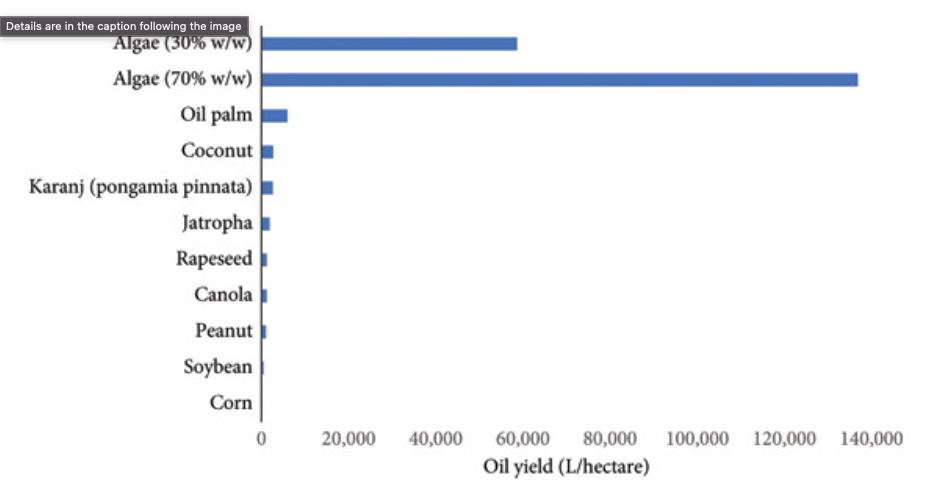

Algae-based feedstocks have also been touted as a potential solution to surging biofuel demand, with potential efficiency savings that are particularly attractive to investors. Algae offer much higher theoretical yields per unit of land area than other land-based crops, but the immaturity of algae in biofuel production has thus far hindered commercialisation.

Oil yields from algae versus first and second-generation biofuel crops

“The key question is not whether feedstocks can meet future demand but whether next-generation feedstocks can be commercialised quickly enough to keep pace with the growing demand for low-carbon biofuels,” Brambilla argues.

“The industry’s ability to scale beyond conventional feedstocks will ultimately determine the long-term growth potential of the biofuels market.”

The final defining factor of biofuel feedstock development is policy, as Bradshaw notes: “The biofuel market as a whole will be defined by policy and regulatory action.”

The EU’s RED III directive is heading in the right direction, aiming for the transport sector to achieve a 29% renewable energy mix and a 14.5% reduction in greenhouse gas intensity by 2030. RED III also caps conventional biofuels from food or feed crops at 7% of each member state’s transport energy, driving a structural shift towards advanced biofuels from waste and residues.

Boosting supplies will require significant financial support. A recent European Commission assessment found that between €3.8bn ($4.34bn) and €7.5bn would be needed annually by 2030 to underwrite industrial-scale biofuel production capacity, alongside an additional minimum of €700m annually in direct payments to farmers and feedstock aggregators.

Elsewhere, in Indonesia, the B35 mandate – requiring 35% palm oil blending in diesel – was maintained throughout 2024, contributing around 39% of the country’s national renewable energy security. Indonesia moved to B40 in 2025 and is now pushing towards B50.

However, the country’s soaring domestic demand is placing pressure on palm oil production and exacerbating global biofuel feedstock scarcity. Indonesia's crude palm oil production was projected at 48.26 million tonnes (mt) in 2024, a decrease of 1.81mt from 2023.

Outside of Indonesia, China's elimination of its 13% export tax rebate on UCO is incentivising domestic use rather than export, tightening the global advanced feedstock market further. Malaysia, too, is exploring UCO and POME export controls to secure feedstock for a production target of 1mtpa of SAF by 2028.

Brambilla concludes: “Yes, biofuel feedstock supply can continue to support market growth, but not if the industry relies solely on today’s dominant feedstocks.

“Resources are inherently limited, and increasing demand is already creating competition between fuel pathways, particularly between RD and SAF. As a result, the industry’s long-term growth will depend on expanding beyond conventional feedstocks and commercialising a broader range of waste and residue-based alternatives.”