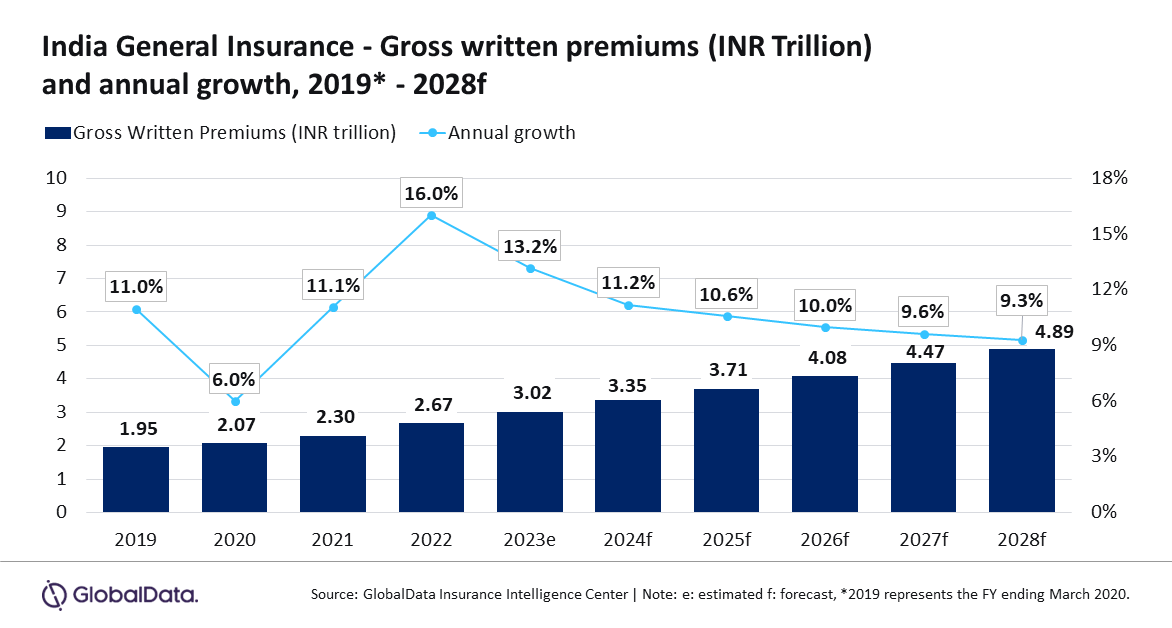

India’s general insurance industry is set to grow at a compound annual growth rate (CAGR) of 9.9% from INR3.35 trillion ($40.36 billion) in 2024 to INR4.89 trillion ($57.3 billion) in 2028, in terms of gross written premiums (GWP), forecasts GlobalData, a leading data and analytics company.

GlobalData’s Insurance Database reveals that the general insurance industry in India is expected to grow by 11.2% in 2024, driven by personal accident and health (PA&H), motor, and property insurance lines, which collectively accounted for 93% share of the total general insurance premiums in 2023.

Swetansha Chauhan, Insurance Analyst at GlobalData, comments: “The general insurance industry in India continued its high growth trend and grew by 13.2% in 2023, driven by economic growth and rising disposable income. Rising consumer awareness of health and other general insurance products and robust regulatory reforms also supported India’s general insurance industry growth. The trend is expected to continue in 2024 and 2025.”

PA&H insurance is the largest line of business, estimated to account for a 39.5% share of general insurance GWP in 2024. It is expected to grow by 14.5% in 2024, primarily driven by increased health awareness following the COVID-19 pandemic and rising medical inflation. PA&H insurance is expected to grow at a CAGR of 12.5% during 2024-28.

Positive regulatory developments will also support the growth of PA&H insurance. In December 2023, the government proposed to establish a healthcare regulator to organize, standardize, and regulate hospitals participating in health insurance. The regulator will be primarily responsible for increasing health insurance penetration, thereby moving the country towards achieving healthcare for all.

As part of the ‘Insurance for All by 2047’ initiative, the Insurance Regulatory and Development Authority of India (IRDAI) approved the launch of the insurance electronic marketplace ‘Bima Sugam’ in March 2024. It will serve as a one-stop solution for all insurance stakeholders like insurers, intermediaries, agents, and customers. It aims to facilitate the purchase, sale, and servicing of insurance policies, as well as the settlement of insurance claims, and grievance redressal, thereby promoting transparency, efficiency, and collaboration across the insurance value chain.

Motor insurance is the second largest line of business that is estimated to account for 31.1% share of general insurance GWP in 2024. The motor insurance industry is expected to register a growth of 10.4% in 2024, driven by rising vehicle sales. According to the Society of Indian Automobile Manufacturers (SIAM), vehicle sales grew by 12.5% in March 2024 as compared to March 2023. This growth is anticipated to continue, propelled by a rise in disposable income and an increasing rate of road accidents.

Chauhan adds: “The growth in vehicle sales was also fueled by the government’s vehicle scrapping policy, which came into effect on April 1, 2023. The policy requires private vehicles older than 20 years and commercial vehicles older than fifteen years to be scrapped. Motor insurance is expected to grow at a CAGR of 7.9% during 2024-28.”

Property insurance, the third largest line of business, is estimated to account for a 22.5% share of general insurance GWP in 2024. Property insurance is expected to grow by 10.4% in 2024, supported by investments in infrastructure projects. The government has increased its infrastructure allocation by 11.1% year-on-year to $134 billion in the 2024-2025 budget which will support the growth of property insurance to grow at a CAGR of 8.3% during 2024-28.

Liability, Marine, Aviation and Transit (MAT), and other general insurance products are estimated to account for the remaining 6.8% share of the general insurance GWP in 2024.

Chauhan concludes: “Recovery in the economy and rising disposable income will continue to support the growth of India’s general insurance industry during the next five years. Initiatives from the government and favorable regulatory reforms will help in increasing the insurance penetration rate in India (0.98%), which was lower as compared to other Asian markets such as Japan (1.75%), South Korea (1.46%), Hong Kong (1.65%) and China (1.26%) in 2023.”