23 Jun, 2021 Fabry disease market growth in US and Japan will be driven by entrance of several novel therapies

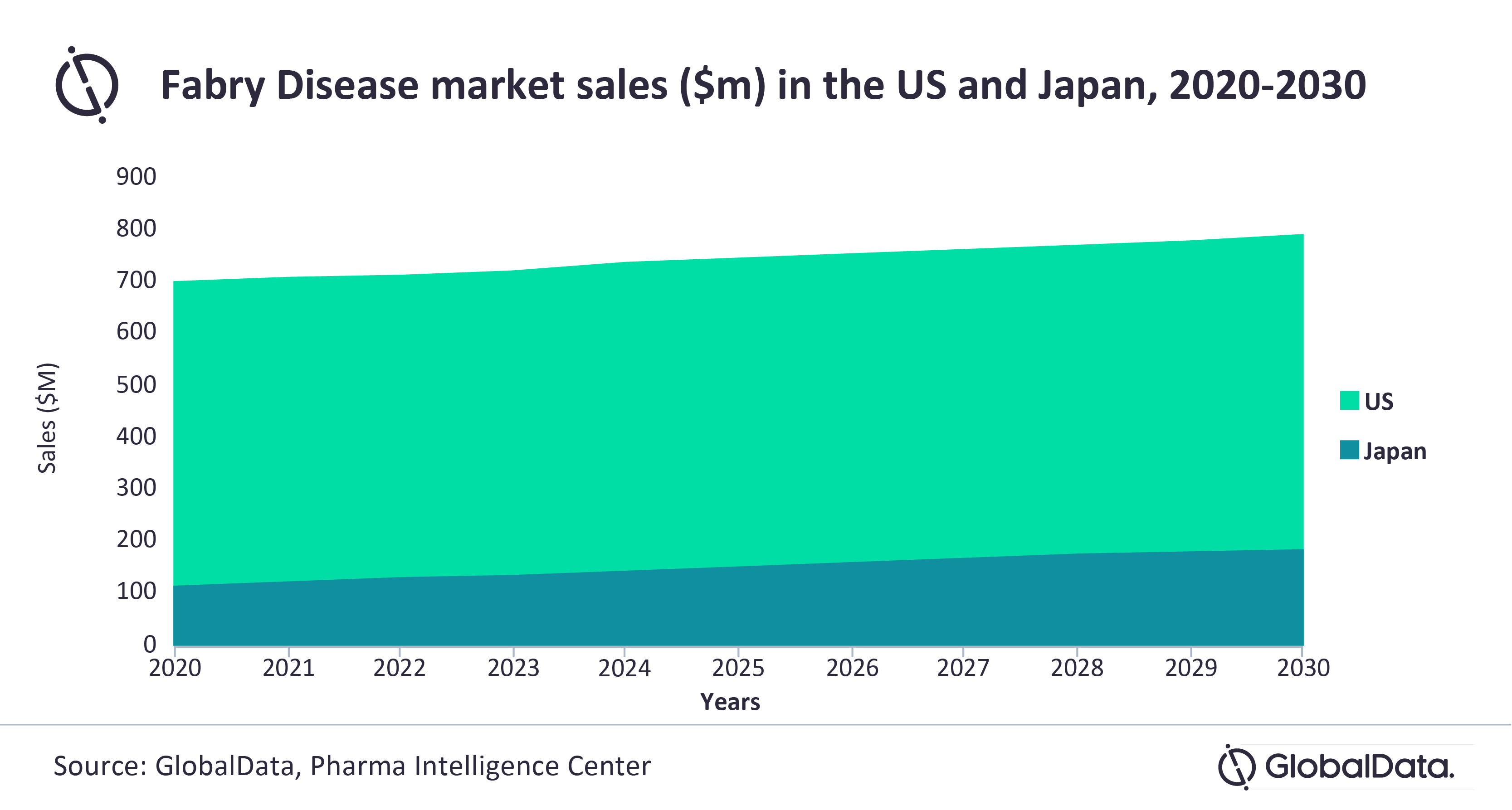

Posted in PharmaThe Fabry disease (FD) market in the US and Japan will see significant growth between 2020 and 2030, as total sales in these two major markets (2MM) are set to increase from $820.15m in 2020 to $985.81m in 2030, at a compound annual growth rate (CAGR) of 1.9%. This sales growth will be in line with a steadily increasing disease prevalence and the entrance of novel agents into the market, says GlobalData, a leading data and analytics company.

Several drugs in the pipeline have novel mechanisms of action (MoAs), including gene therapies that offer the promise of single-dose and potentially curative therapies.

The FD pipeline in the 2MM has two therapies in late-stage development: Chiesi Farmaceutici’s pegunigalsidase alfa, an ERT in pre-registration in the US, and Idorsia Pharmaceutical’s lucerastat, an oral glucosylceramide synthase (GCS) inhibitor in Phase III in the US and Japan. However, the overall clinical data from both of these therapies remain inconclusive.

Akash Patel, Pharma Analyst at GlobalData comments: “Key opinion leaders (KOL) interviewed by GlobalData reported that they remain unconvinced of the efficacy and primary endpoints of the trials for these therapies. In a direct head-to-head comparison with Fabrazyme, pegunigalsidase alfa has not demonstrated a very significant improvement in efficacy.

“However, pegunigalsidase alfa’s clinical data has demonstrated some significant benefits as it requires a decreased frequency of administration, once per month compared to bimonthly administration with existing ERTs, and shows improved drug clearance, as observed in the head-to-head trial with Fabrazyme.”

Oral therapies, such as lucerastat and marketed Galafold, offer novel MoAs that provide support to enzymes in the GLA-α metabolic pathway to prevent the accumulation of Gb3. Galafold, as a pharmacological chaperone, stabilizes the mutant α-GAL A, increases intralysosomal levels, and restores intralysosomal activity. Lucerastat inhibits the GCS enzyme, which is the first step of the glucosylceramide biosynthetic pathway and prevents the accumulation of Gb3.

Several gene therapies are currently in Phase I/II and are expected to enter the US FD market from 2026 onward. These therapies are designed to consist of a single dose and are potentially curative, with data from up to 22 months post-dose demonstrating sustained levels of α-GAL A or a sustained reduction in Gb3.

Patel adds: “In addition to late-stage pipeline agents, another driver of market growth for FD will be an increasing number of early diagnoses. Across the 2MM, regions are driving to increase screening rates for newborns, infants, and pediatric patients who demonstrate the early neuromuscular, cardiac, and digestive system complications that are associated with FD.

“This will increase the number of prescriptions for ERTs, and possibly also for gene therapies for pediatric patients. However, pediatric cases will only remain a small fraction of the patient share in the FD market, as not all regions are likely to adopt neonatal screenings and FD symptoms often do not present until adulthood.”