04 Dec, 2023 Non-stimulants face uphill battle to penetrate ADHD market despite lower abuse potential, observes GlobalData

Posted in PharmaStimulants, amphetamines, and methylphenidates continue to dominate the attention deficit hyperactivity disorder (ADHD) market across the seven major markets (7MM*), serving as the primary pharmacological treatment. Despite historical hesitancy towards their use in children, recent safety reassurances have increased acceptance. The late-stage pipeline introduces non-stimulant options with a focus on lower abuse potential. However, penetrating the stimulant-dominated market remains challenging without comparable efficacy, according to GlobalData, a leading data and analytics company.

The key opinion leaders (KOLs) in the treatment of ADHD noted that while there has historically been hesitancy among patients and parents in the use of stimulants for the treatment of ADHD in children and adolescents (6-17 years), this is now waning in line with positive long-term safety results, and the use of stimulants for ADHD treatment is increasing.

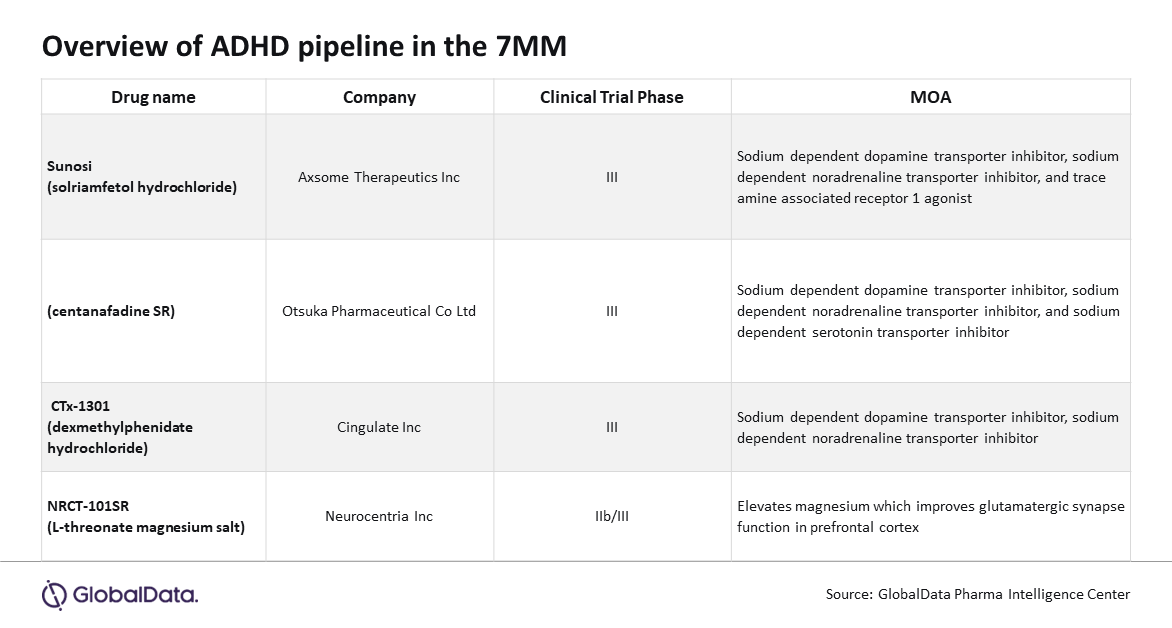

Despite this, three out of the four late-stage pipeline agents in Phase III development within the 7MM have non-stimulant properties: Axsome Therapeutics Inc’s solriamfetol, Otsuka Pharmaceutical Co Ltd’s centanafadine and Neurocentria Inc’s L-Threonate Magnesium Salt. The lower abuse potential of solriamfetol and centanafadine is emphasized by developers, but without displaying efficacy comparable to marketed stimulants they will struggle to penetrate the stimulant market share even if approved.

Lorraine Palmer, Pharma Analyst at GlobalData, comments: “Marketing emphasis on abuse potential is common in non-stimulates both marketed and pipeline, this is despite KOLs viewing the abuse potential of ADHD stimulants as overstated.”

A common cause for concern with stimulants is side-effects such as sleep disturbance and decreased appetite. Thus far non-stimulants have not proven to be the answer to these concerns. There are four non-stimulants presently marketed in at least one of the 7MM; guanfacine, clonidine, atomoxetine and viloxazine. Sleep-disturbance and decreased appetite have been reported as adverse events resulting from both clonidine and atomoxetine. In addition, all four display cripplingly lower efficacy in the treatment of ADHD than stimulants.

Palmer continues: “The KOLs interviewed by GlobalData were not concerned about whether a treatment is a stimulant or a non-stimulant, rather they are focused on the pharmaceuticals efficacy and side-effect profile.”

Marketed non-stimulants retain a place in the treatment algorithms only as second-line therapies, most frequently used for individuals who do not respond or cannot tolerate stimulants or for whom stimulants would be counter-indicated. KOLs noted that to penetrate this smaller section of the market, pipeline agents need to display a better side-effect profile than atomoxetine and guanfacine, the most widely approved non-stimulants in the 7MM.

Palmer concludes: “Rather than an emphasis on abuse potential, a better alternative strategy to penetrate the saturated ADHD market would be to target key unmet needs in ADHD treatment such as improving compliance or providing coverage into the evening without affecting sleep.”

Information – Countries included within the 7MM are France, Germany, Italy, Spain, the UK, the US, and Japan. GlobalData expects to release an ADHD opportunity assessment and market forecast report for the 7MM in 2024.